This post explores the essential details of 529 accounts. A 529 account can help you work toward your education funding goals.

Learning Points

529 Plan Types

A section 529 plan – also known as a “qualified tuition plan” – is a tax-advantaged investment program designed to help families save for higher education expenses. These plans are sponsored by states, state agencies, and educational institutions. In 2024, there are two kinds of 529 plans:

- Education Savings Plans: most education savings plans are available to everyone. A few have residency requirements for the account holder and/or the beneficiary.

- Prepaid Tuition Plans: While these typically have residency requirements, one notable exception is a prepaid tuition plan sponsored by a group of private colleges and universities.

529 accounts offer a flexible way for you to save and invest for a variety of educational goals, like:

- Kindergarten through 12th grade (K-12)

- Trade schools

- Undergraduate

- Qualifying graduate schools

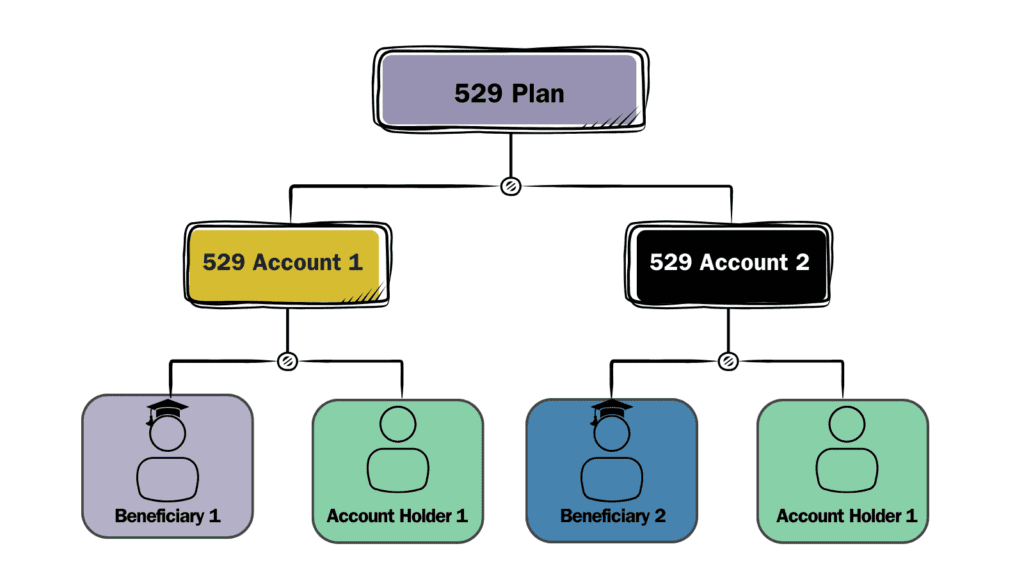

529 Account Structure and Illustrative Chart

The person who opens the 529 account through either of the two plan types is called the account holder, or the saver. The account holder opens the account for the beneficiary (i.e. the student). The account holder and the beneficiary can be the same person.

Below is an illustrative chart showing how these elements fit together:

An account holder can open multiple 529 accounts at the same 529 plan, and each account can be for a different beneficiary.

Personalize Your Education Funding Plans

Like most financial planning opportunities, education funding requires personalizing your plan and considering the interplay of all the details of your financial life. In many situations, parents will want to prioritize funding their own retirement goals over their children’s education funding goals.

Coordinating with a qualified tax advisor can be an important layer to successfully planning and executing on your 529 strategy, too, and should not be overlooked.

If contributing to a 529 account is a savings priority for you, read on, and familiarize yourself with the essential details of these investment accounts.

Key Considerations About 529 Accounts

There is no “one-size fits all” 529 strategy. The way you approach selecting, opening, and managing a 529 account depends on your personal facts and circumstances.

Here’s a simple framework to follow:

- What state do you live in?

- When does your 529 beneficiary need to use the money?

- What kind of educational need, or needs, will the 529 fund?

Start Here: What State Do You Live In?

As a starting point, it’s beneficial to frame 529 plan discussions around the account holder’s state of residency.

This is primarily driven by each state’s unique approach to taxes on 529 plan contributions and distributions. Framing it in this way helps put some initial guiderails to understand and compare against alternatives.

For example, some states, like Missouri, offer residents a tax deduction for their 529 plan contributions. Other states, like Kentucky, assess an income tax but do provide a tax deduction or credit for 529 plan contributions. The amounts of these tax deductions vary from state to state.

If you live in a state that has no state income tax, like Texas or Tennessee, there is no state income tax deduction or credit to consider.

Similarly, when it comes to K-12 tuition, the states have a mixed view. Some states, like New York, view paying for K-12 expenses as a non-qualified distribution. If you live in a state that follows this approach, this could influence the timing of when you plan to distribute funds from your 529. Other states allow you to use 529 assets to pay for qualified education expenses.

Familiarize yourself with your state’s specific 529 plan-related rules, tax benefits, and limits.

Some states provide additional flexibility for residents to use 529 plans from other states. This kind of reciprocity arrangement treats other state’s plans the same way as the in-state plan is treated. Review the details of the state’s agreement before enrolling in a 529 plan sponsored by a different state. Additionally, these agreements can change over time, so check with the plan’s administrator or your tax professional for the latest information.

529 Account Contributions

While contributions to a 529 account are not tax-deductible at the federal level, they are subject to the annual gift tax exclusion limit. In 2024, an individual’s annual gift tax exclusion limit is $18,000 per recipient.

Many states offer a tax deduction, and a handful offer tax credits, for residents who contribute to a 529 plan.

Notably, Missouri residents may claim this benefit whether they invest in a Missouri 529 plan or another state’s 529 plan. For example, Missouri residents can contribute up to the following amounts in a 529 plan and reduce taxable income:

- $8,000 (filing single)

- $16,000 (married filing jointly)

Given this approach, for example, if a Missouri resident grandparent contributes to their grandchild’s out-of-state 529 account, they would still receive this tax benefit. The same holds true for a parent contributing to their child’s out-of-state 529 account.

529 Account Earnings

529 account earnings grow tax-free while invested in the plan and are not treated as income for either the account holder or the beneficiary.

However, the earnings on non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, state and local income taxes and recapture of state tax deductions.

529 Account Distributions

529 account distributions used to pay for qualified education expenses are not taxable.

The timing of your 529 account distributions should match to the same year you paid qualified educational expenses. If the total distributions exceed the beneficiary’s qualified education expenses (including tuition at an elementary or secondary public, private, or religious school), the excess portion of the earnings is taxable.

Back to our hypothetical Missouri resident, qualified distributions are not taxable whether the Missouri resident has a Missouri 529 account or an out-of-state 529 account.

K-12 Education

Additionally, many, but not all, plans allow distributions up to $10,000 per year for tuition in connection with enrollment or attendance at a K-12 school. These include elementary or secondary public, private, or religious school. Trade schools can often be included in this definition.

Student Loan Payments

You can disburse 529 account assets to pay principal and/or interest on your designated beneficiary’s or their sibling’s student loan. 529 account distributions can be used for loan repayments. These are limited to $10,000 per borrower during their lifetime. Interest paid with these funds doesn’t qualify for the student loan interest deduction.

529 Plan Investment Options

529 plans traditionally offer investment options like mutual funds, exchange-traded funds (ETFs), CDs, and sometimes an account insured by the FDIC.

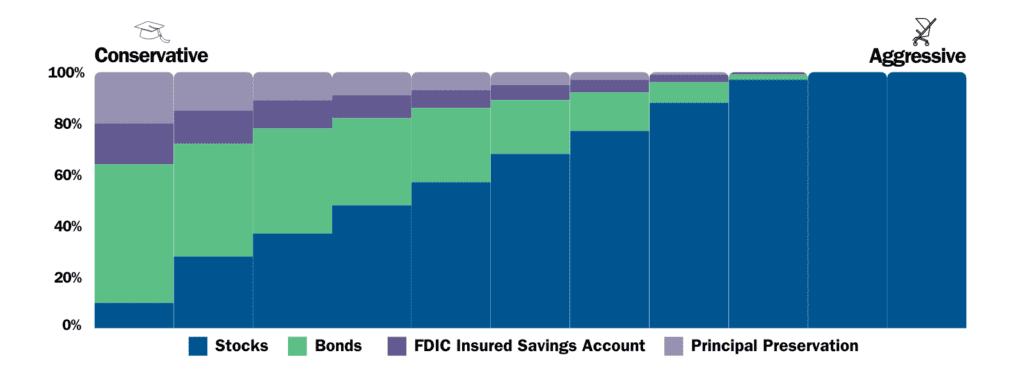

You can choose the investment options that best align with your personal risk tolerance, risk capacity and time horizon.

For example, the 529 investments for your high school freshman will likely look different than those of a parent whose child is in daycare.

In this example, your hypothetical high school freshman’s 529 investments will likely need to have less risk exposure to the equity markets than the 529 account of the toddler. Continuing with this sample, your high schooler’s education funding goal will have shifted from growing 529 assets to protecting 529 assets. This means your mix of stocks and bonds would adjust to a more conservative investment approach.

Similarly, if you are planning to use a portion of your 529 account to pay for K-12 education for a near-term need, you may not feel comfortable taking on riskier investments.

The chart below is an illustrative example of this risk continuum and how it could influence what a 529 account invests in over time.

Aligning Your 529 Account Investments with Your Education Goal

An Evergreen Perspective

There is no single, correct way to invest but there are suboptimal ways that can be avoided, and doing so can improve your long-term results.

- Market timing over your investment horizon is unlikely to deliver consistent, excess returns. Many 529 plans limit your ability to adjust your investments to only twice a year.

- Expenses and Taxes Matter. Frictions such as high costs and unnecessary taxes can erode returns over time. This can cause high performing investments to not look as stellar after you factor in expenses and taxes.

- Don’t Play the Losers Game. There is no evidence about the persistence of past performance as an indicator when selecting investments.

- Emotions, biases, and other psychological factors can cause the average investor, generally, to be wired to be poor investors of their own money. Be aware that these factors exist and take time to fully reevaluate your plan if you find yourself reacting, and not responding, to a particular situation.

Fees and Expenses

Expanding a little further on this topic, like many investment accounts, 529 plans may charge several types of fees, including:

- an enrollment/application fee

- an account maintenance fee

- program management fees

- underlying investment expense ratios.

Some savings accounts and CDs can also have early redemption penalties. Carefully review the fee structure of any plan you’re considering. High fees can erode your investment returns.

You do not need to work directly with a broker to open and fund a 529. More often than not, a direct-sold 529 plan, one that you can open and fund on your own, has lower fees and expenses. Be aware, broker-sold plans often mean higher fees.

Practical Considerations

If you have identified that a 529 account fits into your plan, consider opening and funding it as soon as you are able to do so. In addition to giving your investments more time to work for you, and benefiting from tax-free earnings growth, doing so starts the new 15-year, 529 to Roth IRA rollover clock.

529 to Roth IRA Rollover

Starting in 2024, 529 account holders will have the opportunity to transfer up to a lifetime limit of $35,000 from a 529 plan to a Roth IRA for a beneficiary.

This rollover allows Roth IRA owners to avoid triggering non-qualified withdrawal issues for an overfunded 529 account.

Eligibility Criteria

- The 529 account must be more than 15 years old to qualify for this rollover.

- Only amounts contributed to the 529 account more than five years ago can be rolled over.

- Note that this applies specifically to Roth IRAs, not traditional IRAs.

Separately, once you know how much you need to save, set up automatic contributions to your 529 account so you stay on track with your education funding goal.

Summary

Hopefully you found this helpful in understanding some essential details about 529 accounts.

What works well for one person might not be the perfect fit for you. Make sure you understand the tax implications of investing in a 529 account and consider whether to consult a tax adviser.

Fully incorporating all the moving parts of your financial life into your decision is a must.

Successfully building your wealth can feel energizing, and with that success can come new stresses and complexities.

If you’re unclear about your financial future, or uncertain about what your next steps might look like, let’s talk.

Stay tuned for more Insights on ways to build an enjoyable now and many bright tomorrows.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.