If you have a significant education funding goal and significant assets to contribute toward your goal, it’s worth learning how you can pair a 529 plan with a 5-year gifting approach.

Learning Points

529 Account Overview

A section 529 plan – also known as a “qualified tuition plan” – is a tax-advantaged investment program designed to help families save for higher education expenses. These plans are sponsored by states, state agencies, and educational institutions.

529 accounts offer a flexible way for you to save and invest for a variety of educational goals, like:

- Kindergarten through 12th grade (K-12)

- Trade schools

- Undergraduate

- Qualifying graduate schools

If you have not yet had a chance to read our foundational 529 account piece, “Elevate Your Understanding: Today’s 529 Account Essentials“, give it a read, it explores the essential details of 529 accounts.

529 Plan Contributions

529 plan contributions are one of two essential concepts to understand when you’re considering a 529 account superfunding strategy. While contributions to a 529 account are not tax-deductible at the federal level, they are subject to the annual gift tax exclusion limit. In 2024, an individual’s annual gift tax exclusion limit is $18,000 per recipient.

Many states offer a tax deduction, and a handful offer tax credits, for residents who contribute to a 529 plan.

Notably, Missouri residents may claim this benefit whether they invest in a Missouri 529 plan or another state’s 529 plan. For example, Missouri residents can contribute up to the following amounts in a 529 plan and reduce taxable income:

- $8,000 (filing single)

- $16,000 (married filing jointly)

Given this approach, for example, if a Missouri resident grandparent contributes to their grandchild’s out-of-state 529 account, they would still receive this tax benefit. The same holds true for a parent contributing to their child’s out-of-state 529 account.

Annual Gift Exclusion

The annual gift tax exclusion, sometimes called the gift tax exemption – is another essential concept to understand when you’re considering a 529 account superfunding strategy. The annual gift exclusion is a provision that allows you to give a certain amount of money or property to someone each year without incurring any gift tax.

For tax year 2024, this annual gift exclusion is set at $18,000 per recipient. Specifically, the first $18,000 of ‘gifts of present interest’ to each donee during the calendar year is subtracted from total gifts in determining the amount of taxable gifts.

This means that you could give $18,000 to your child, another $18,000 to a friend, and so forth, all without the burden of gift tax reporting and taxes.

All the gifts you make to a donee/recipient during the calendar year are fully excluded under the annual exclusion if:

- they are all gifts of present interest, and

- they total $18,000 or less.

One example of this, assuming you made no other gifts in 2024, is the following:

- When you make two $9,000 contributions to your child’s 529 account. You’ve used the entire $18,000 annual gift exclusion.

Now that you have a sense of how 529 account contributions and the annual gift exclusion work, let’s explore 529 account superfunding works.

What is 529 Account Superfunding?

Since it’s tax filing season, it’s only fitting to reference one of the more concise explanations of 529 account superfunding;

“If in 2023, you contributed more than $17,000 to a qualified tuition plan (QTP) on behalf of any one person, you may elect to treat up to $85,000 of the contribution for that person as if you had made it ratably over a 5-year period.”

Source: Internal Revenue Service: Instructions for Form 709 – United States Gift (and Generation-Skipping Transfer) Tax Return, 2023.

Keep in mind that in 2024, the annual gift tax exclusion allows individual taxpayers to give each recipient up to $18,000 per year without incurring a gift tax.

As such, if you embark on a 529 account superfunding strategy in 2024, you can contribute up to $90,000. That’s a lot of books.

Potential Benefits of 529 Superfunding

- Accelerated savings: By contributing a larger amount to your 529 account upfront, you can take advantage of potential investment growth over a longer time period.

- Tax Planning: Earnings in a 529 plan grow tax-free, and withdrawals for qualified education expenses are also tax-free. Coordinating with a qualified tax advisor can be an important layer to successfully planning and executing on your 529 strategy, too, and should not be overlooked.

- Estate planning coordination: Superfunding can be part of an estate planning strategy to reduce your taxable estate while supporting a loved one’s education. Coordinating with a qualified estate attorney can be another worthwhile element of successfully planning and executing on your 529 strategy, too.

Origin Story: Treatment of Excess Contributions

Section 529 (c)(2)(B) of the Internal Revenue Code, provides the basis for a 529 account superfunding strategy, by stating the following:

“If the aggregate amount of contributions described in subparagraph (A) during the calendar year by a donor exceeds the limitation for such year under section 2503(b), such aggregate amount shall, at the election of the donor, be taken into account for purposes of such section ratably over the 5-year period beginning with such calendar year.”

Source: Internal Revenue Code, Section 529(c)(2)(B)

Plain English: Treatment of Excess Contributions

If you want to gift more than the annual gift tax exclusion during a calendar year to a 529 account, there is an option to do the following:

- Elect to divide the total amount of the gift by 5.

- Treat the resulting quotient as the same, consistent annual gift for the next 5 years.

- Year 1 starts in the year you made the gift.

- Assumes no additional gifts are made during the 5-year period.

Plain English: Short Example 1

Applying this framework in 2024, a parent could:

- Elect to gift up to $90,000 to their child’s 529 account.

- Treat this $90,000 gift as if it had made it ratably over a 5-year period.

- The resulting quotient is $18,000 each year for five years.

- Year 1 of the 5-year period is 2024.

You can make this election for as many separate people as you made 529 account contributions.

Plain English: Short Example 2

Extending this logic to a married couple with 3 children in 2024, each parent could:

- Elect to gift $90,000 to the 529 account for each of their children.

- The resulting quotient is $18,000 each year for five years.

- That’s $180,000 per 529 account in Year 1.

- The couple’s total gifts would be $540,000.

In both these examples, after this election is made, you cannot make additional gifts to the same beneficiary for the next four years without exceeding the annual exclusion. If you do make additional gifts during those four years, they will be subject to gift tax rules.

Keep in mind that 529 account superfunding is not limited to one-time event, as long as you adhere to the rules and start early enough before your education funding need.

These are just two examples. There are additional planning opportunities to consider for families with sizeable education funding goals or estate planning complexities.

For instance, the year before you elect to superfund a 529 account, you could contribute up to the annual gift tax exclusion; timing is critical.

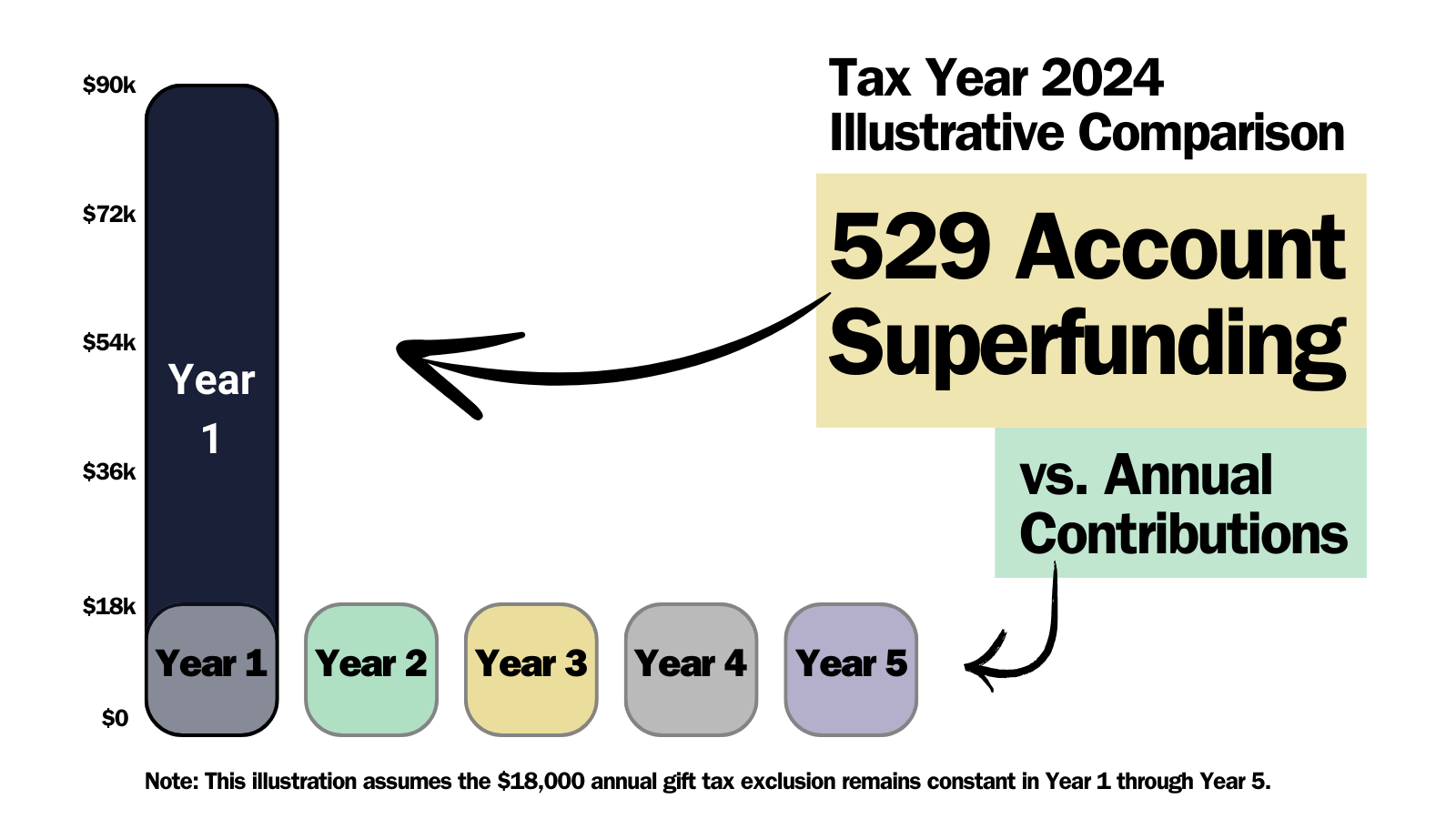

Illustrative Comparison

Here’s an illustrative comparison of 529 account superfunding versus a traditional, annual gifting approach:

Potential Downsides of 529 Account Superfunding

If you want to fund a 529 plan, there are downsides and limitations to consider around 529 account superfunding.

- You need to be certain the money is most needed for the beneficiary’s education, and not another savings priority. If you’re funding a 529 at the expense of your retirement, you might need to reevaluate your education funding solutions.

- Potentially miss out on the state tax credit or deduction, depending on your state of residence.

- A minor point in this context, but you might miss out on subsequent increases to the annual gift tax exclusion tied to inflation.

- 529 plans will accept contributions to account(s) until all account balances for the same beneficiary total a specific dollar threshold. This threshold usually represents the estimated cost of four years of undergraduate studies and two years of graduate school in the state of the 529 plan.

If you elect to superfund a 529 and then die during the 5-year period, the entire gift does not stay outside your gross estate.

This unique situation is contemplated in Section 529 (c)(4)(C) of the Internal Revenue Code, which states the following:

Amounts includible in estate of donor making excess contributions.

“In the case of a donor who makes the election described in paragraph (2)(B) and who dies before the close of the 5-year period referred to in such paragraph, notwithstanding subparagraph (A), the gross estate of the donor shall include the portion of such contributions properly allocable to periods after the date of death of the donor.”

Source: Internal Revenue Code, Section 529(c)(4)(C)

Summary

Hopefully you found this 529 account superfunding overview helpful and informative.

What works well for one person might not be the perfect fit for another. When evaluating an education funding decision, you’ll want to fully incorporate all the moving parts of your financial life into your decision.

Make sure you understand the tax implications of investing in a 529 account – especially if you are considering a 529 account superfunding strategy. Consider whether to consult a qualified tax professional.

The Next Step

When you know who and what are truly important, you can create incredible clarity about your spending and saving.

Clarity to confidently spend on things that matter. Clarity to avoid spending your hard-earned resources on things that aren’t aligned with what you want in life.

As your financial planner in Saint Louis, we can help you plan for the future and enjoy the present moment.

Start feeling more confident that you are making progress toward your education funding priorities.

When you thoughtfully execute on this approach, you can increase the likelihood of achieving your goals, setting new ones, and enjoying the present moment.

Frequently, proactive and open collaboration with your tax and estate planning professionals can help you work towards your financial planning goals. Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.