If you’re saving for retirement, a Roth IRA can provide investors like you with additional flexibility on your retirement path. Learn about the essentials of the Roth IRA in 2024.

Learning Points

What is an IRA?

An Individual Retirement Account (IRA) is a tax-advantaged personal savings account generally used for setting money aside for retirement. Depending on the type of IRA and your personal circumstances, these tax advantages can include tax-deductible contributions for traditional IRAs and tax-free withdrawals for Roth IRAs. Make sure you understand the tax implications of investing in an IRA account and consider whether to consult a qualified tax professional.

IRAs can sometimes feel familiar from afar – it’s all right there in the name “Individual Retirement Account” – and then, after a closer review, it can seem entirely foreign.

You’re likely familiar your 401(k) account, how your paycheck is used to contribute to your 401(k), and regularly receive communications about your 401(k) from your employer/plan sponsor. It can sometimes feel like there is more structure and educational resources built around your 401(k) experience than the average IRA.

Consider this. For most investors, IRAs generally complement, but do not fully replace employer-sponsored plans, like a 401(k) or a 403(b), for your retirement savings goals.

Common Types of IRAs

A Roth IRA offers unique benefits and considerations for investors like you.

Let’s break down how Roth IRAs work, provide some educational information, and make Roth IRAs more approachable.

Roth IRA

Roth IRA: Contribution and Income Limitations

You can open and contribute to a Roth IRA if you – or, if you file a joint return, your spouse – received taxable compensation during the year. Your Roth IRA contributions consist of after-tax dollars – money you’ve already paid income tax on.

In 2024, you can contribute up to the following amounts into a Roth IRA:

- $7,000 per person.

- Up to $8,000 per person if you are age 50 or older.

There are no age limits on making regular contributions to traditional IRAs or Roth IRAs (those rules ended after 2019).

These IRA contribution limits are per taxpayer, not per account. So, if you have both a Roth IRA and a traditional IRA, you aggregate your contributions across both accounts up to the applicable limit.

In 2024, there are adjusted gross income phase-out ranges for taxpayers making contributions to a Roth IRA.

- For single and head of household taxpayers, the income phase out is between $146,000 and $161,000.

- For married couples filing jointly, the income phase-out range is between $230,000 and $240,000.

IRA contributions can only be made with earned income. If only you or your spouse earned income in a particular tax year, you might still be able to contribute to your IRA. Be sure to read the Spousal IRA overview below for additional details.

The Potential for Tax-Free Growth

Unlike a traditional IRA, your Roth IRA contributions consist of after-tax dollars – money you’ve already paid income tax on. This allows your Roth IRA contributions to grow tax-free provided that you follow the IRS’ Roth IRA rules.

Roth IRA: Tax Deductibility

There is no tax deduction currently for Roth IRA contributions.

Roth IRA: Withdrawal Sequence and Qualified Distributions

Roth IRA withdrawal rules are relatively more flexible than those for traditional IRA or 401(k) plans.

When you need to access your Roth IRA funds, the order of withdrawals is as follows:

- Contributions (1st)

- Conversions (2nd)

- Earnings (3rd)

If you experience an unexpected expense that fully depletes your emergency fund, you can distribute some or all your principal contributions from your Roth IRA at any age for any reason without taxes or penalties.

There is a five-year holding period for qualified distributions. This period begins January 1 of the year a contribution is made to any Roth IRA.

Qualified Distributions

Specifically, a qualified distribution is any payment or distribution from your Roth IRA that meets the following requirements:

- It is made after the 5-year period beginning with the first tax year for which a contribution was made to a Roth IRA set up for your benefit.

- The payment or distribution is:

- Made on or after the date you reach age 59½,

- Made because you are disabled,

- Made to a beneficiary or to your estate after your death, or

- One that meets the requirements listed for first-time home buyers (up to a $10,000 lifetime limit).

So, if you’re over 59½ and have held your Roth IRA for at least five years, you can withdraw earnings with no tax or penalty. This is in addition to the contributions you can withdraw with no taxes or penalties.

If you’re under the age 59½ and take a Roth IRA distribution within five years of the conversion, you’ll pay a 10% penalty unless you qualify for an exception.

Roth IRA: Required Minimum Distributions (RMDs)

Required minimum distributions (RMDs) are the minimum amounts you must withdraw from your retirement accounts, which include traditional IRAs, SIMPLE IRAs, and SEP IRAs, each year.

There are no required minimum distributions (RMDs) for a Roth IRA while the original account holder is alive.

However, if you intend to leave your Roth IRA assets to heirs after your death, they should plan on required minimum distributions.

Roth IRA: Beneficiary Designation

We understand how hard it can be to think about what happens after you are gone.

If you would like your loved ones to benefit from your IRA assets after your death, we’re here to help coordinate your wishes.

When you die, the assets you’ve carefully saved in your IRA go to those you’ve laid out in the IRA beneficiary designation form.

Most folks tend to choose individuals as beneficiaries. Maybe they leave everything to their spouse or divide it equally among their children (i.e. per stirpes). Some even choose to leave their assets to charities, making one last act of kindness.

Alternatively, you can also name a trust as your IRA beneficiary.

With that in mind, the beneficiary of your Roth IRA can be anyone you designate.

The Next Step: It’s important to review your account beneficiaries regularly, especially if key aspects of your personal or financial life have changed significantly.

Roth IRA: Investment Options

Like a workplace retirement account, a Roth IRA can provide you with investment flexibility. IRA investment options are broader relative to a typical 401(k) plan. With a Roth IRA, you can select what you invest in, as well as how much and when you invest.

Remember to stay within the contribution limits, though.

Mutual Funds, exchange traded funds (ETFs), and bonds are all potential investment options for IRA owners.

IRAs cannot invest in life insurance or collectibles, such as art, antiques, gems, coins, or alcoholic beverages.

IRAs can invest in certain precious metals only if they meet specific requirements.

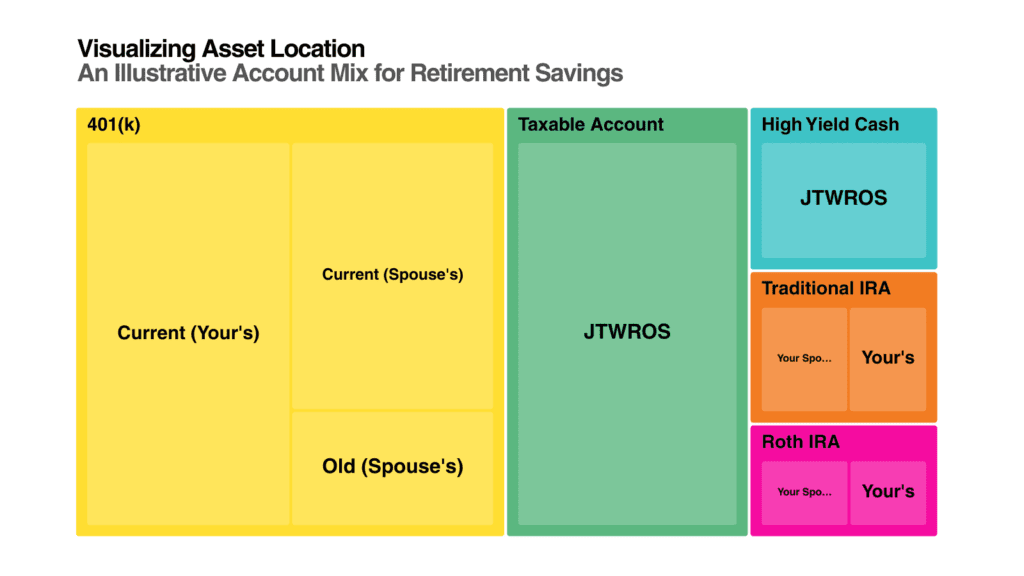

Roth IRA: Asset Location

Your personal situation and investing goals can help shape your asset allocation. Generally speaking, this is the mixture of equity-like and bond-like investments you own. Once you establish the right asset allocation for you, it can then help guide your asset location. Meaning, the type of accounts you hold investments in.

Long-term investors can take a comprehensive view across all of their investment accounts, not just on an account-by-account basis. Your money should work together, and you can make sure your Roth IRA and other investment accounts are working together toward your retirement goals.

Long-term investors like you can factor in the tax efficiency of a specific investment. After-tax returns matter. Investors can look to minimize the effects of taxes on investment returns by placing different types of investments in tax-advantaged accounts or taxable accounts based on the tax treatment of the account and their personal circumstances.

Roth IRAs are tax-free accounts, and long-term investors generally see better tax-efficiency by holding equities – like mutual funds and exchange traded funds (ETFs) – in these types of accounts. Asset location is a broader lens that you can apply to all your investment accounts. It’s something that needs to be personalized to fit your specific facts and circumstances.

Creditor Protection

While Individual Retirement Accounts (IRAs) offer benefits for your retirement savings, their vulnerability to creditor claims requires consideration and varies by state.

For IRAs, there are different statutes and specific case law in each state. While the details are beyond the scope of this article, the extent of an IRA’s creditor protection can depend on multiple factors, including: your state of residence, the type of IRA, the IRA’s origin (e.g. inherited IRA), and type of creditor claim.

The Next Step: If you need to understand how creditor protections apply to your specific situation, consulting with a qualified attorney who can effectively engage in asset protection planning is a good starting point.

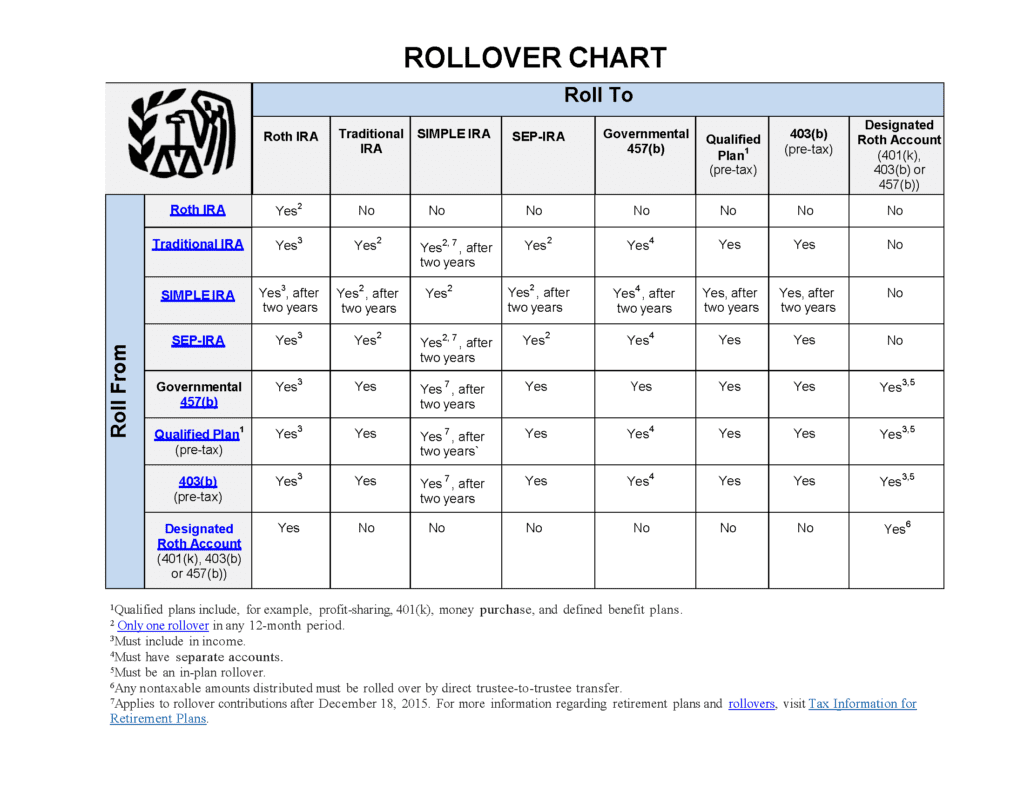

Rollover Considerations

If you are contemplating investing in a Roth IRA, then understanding the account rollover rules could help you plan ahead.

These rules govern how you can transfer assets held in these accounts to other types of accounts.

Below is a chart showing the different ways specific account types can, and cannot, transfer to other types of accounts.

Source: https://www.irs.gov/pub/irs-tege/rollover_chart.pdf

Spousal IRA: Overview

A spousal IRA is a special provision that allows a spouse to contribute to an individual retirement account (IRA) based on their working spouse’s income. The IRA can be either a traditional IRA or a Roth IRA. You’re a team, right?

For 2024, if you file a joint return and your taxable compensation is less than that of your spouse, the most that can be contributed for the year to your IRA is the smaller of the following two amounts:

- $7,000 ($8,000 if you are age 50 or older).

- The total compensation includible in the gross income of both you and your spouse for the year, reduced by the following two amounts.

- Your spouse’s IRA contribution for the year to a traditional IRA.

- Any contributions for the year to a Roth IRA on behalf of your spouse.

Given this, the total combined contributions you can make to your IRA and your spouse’s IRA in 2024 can be as much as:

- $14,000 if you are both under age 50.

- $15,000 if only one of you is age 50, or older.

- $16,000 if both of you are age 50, or older.

Summary

Hopefully you found this overview of the Roth IRA essentials helpful and educational.

What works well for one person might not be the perfect fit for another. When evaluating what type(s) of IRAs best align with your goals, you’ll want to fully incorporate all the moving parts of your financial life into your decision.

If you are interested in working with an advisor to make sure all these pieces fit together to support your goals and values, we’d be honored to learn more and explore how we might be able to help you.

Make sure you understand the tax implications of investing in a Roth IRA and consider whether to consult a qualified tax professional.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.