If you’re saving for retirement, a Traditional IRA can provide additional flexibility to investors like you. Learn about the essentials of this type of IRA.

Learning Points

What is an IRA?

An Individual Retirement Account (IRA) is a tax-advantaged personal savings account generally used for setting money aside for retirement. Depending on the type of IRA and your personal circumstances, these tax advantages can include tax-deductible contributions for traditional IRAs and tax-free withdrawals for Roth IRAs. Make sure you understand the tax implications of investing in an IRA account and consider whether to consult a qualified tax professional.

IRAs can sometimes feel familiar from afar – it’s all right there in the name “Individual Retirement Account” – and then, after a closer review, it can seem entirely foreign.

You’re likely familiar your 401(k) account, how your paycheck is used to contribute to your 401(k), and regularly receive communications about your 401(k) from your employer/plan sponsor. It can sometimes feel like there is more structure and educational resources built around your 401(k) experience than the average IRA.

Consider this. For most investors, IRAs generally complement, but do not fully replace employer-sponsored plans, like a 401(k) or a 403(b), for your retirement savings goals.

Common Types of IRAs

Traditional IRAs offer unique benefits and considerations for investors like you.

Let’s break down how traditional IRAs work, provide some educational information, and make traditional IRAs more approachable.

IRA Fundamentals to Consider

If an IRA is a savings priority for you, here are some essential concepts to consider and review against your personal situation:

- Contribution and Income Limitations

- Taxability

- Tax Deductibility

- Earnings

- Withdrawals, Early Withdrawal Penalties, and Exceptions

- Required Minimum Distributions (RMDs)

- Beneficiaries

- Rollover Considerations

- Investment Options and Asset Location

- Creditor Protections

Traditional IRA

Traditional IRA: Contribution and Income Limitations

You can open and contribute to a traditional IRA if you – or, if you file a joint return, your spouse – received taxable compensation during the year.

In 2024, you can contribute up to the following amounts into a traditional IRA:

- $7,000 per person.

- Up to $8,000 per person if you are age 50 or older.

There are no age limits on making regular contributions to traditional IRAs or Roth IRAs (those rules ended after 2019).

These IRA contribution limits are per taxpayer, not per account. So, if you have both a Roth IRA and a traditional IRA, you must split your contributions across both accounts up to the limit.

IRA contributions can only be made with earned income. If only you or your spouse earned income in a particular tax year, you might still be able to contribute to your IRA. Be sure to read the Spousal IRA overview below for additional details.

Traditional IRA: Taxability

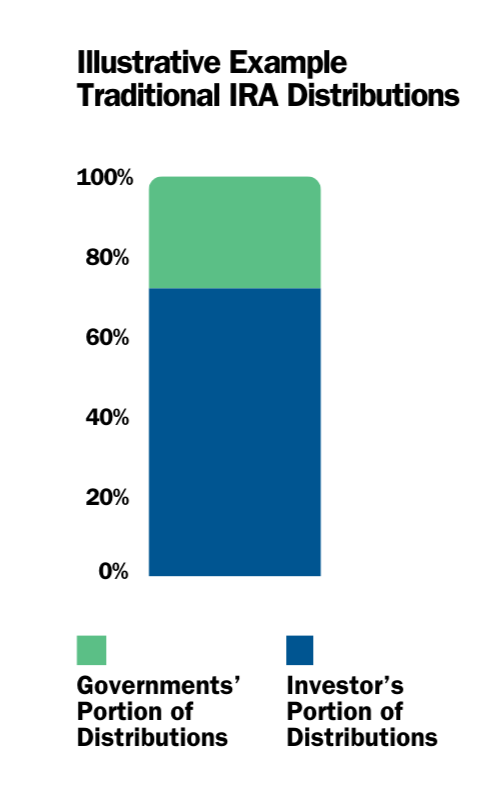

Traditional IRAs are tax-deferred accounts.

Contributions to a traditional IRA are made with pre-tax dollars.

Meaning, when you invest money in your traditional IRA, you won’t pay taxes until you start distributing money out of the account.

Any withdrawals/distributions are taxed at your ordinary income rates at the time of the distribution.

The chart on the left provides an illustrative example of how your traditional IRA distributions are allocated between government taxes and your income.

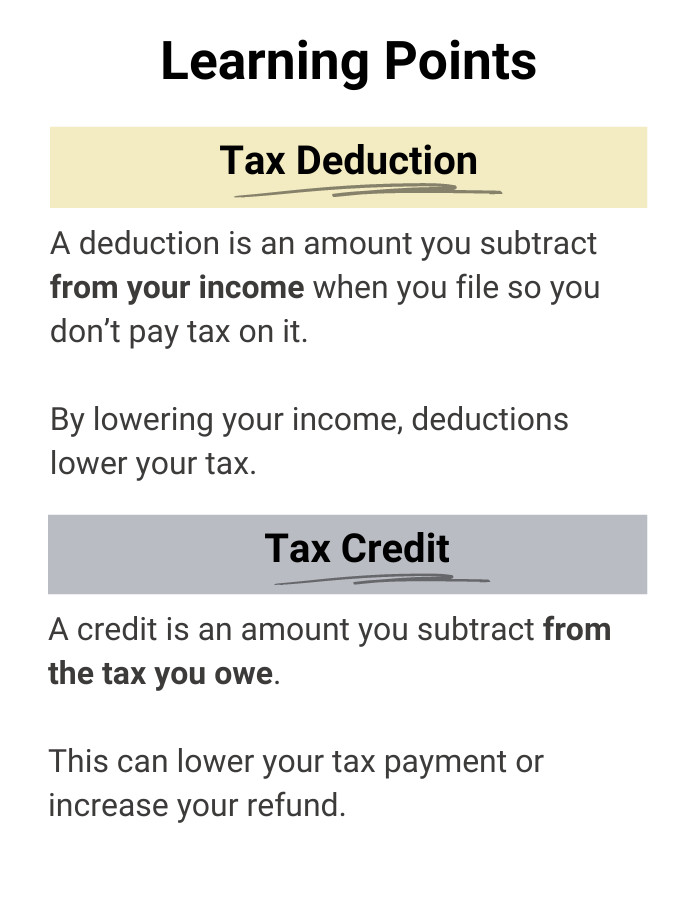

Traditional IRA: Tax Deductibility

If you meet specific eligibility criteria, you can deduct your contributions from your taxable income, which can lower your tax bill.

If you are covered by a workplace retirement plan, like a 401(k), your modified adjusted gross income (MAGI) affects the amount of your deduction.

Specifically, the deductibility of your traditional IRA contributions is limited by the following income phase-outs in 2024:

- For single and head of household taxpayers, the modified AGI phase out is between $77,000 and $87,000.

- For married couples filing jointly, the modified AGI phase-out range is between $123,000 and $143,000.

If you are not covered by a workplace retirement plan, like a 401(k), but your spouse is, the deductibility of your traditional IRA contributions is limited by the following income phase-out in 2024:

- For married couples filing jointly, the modified AGI phase-out range is between $230,000 and $240,000.

Traditional IRA: Withdrawals, Early Withdrawal Penalties, and Exceptions

Traditional IRA withdrawals during retirement are taxable.

The Internal Revenue Service (IRS) imposes a 10% early withdrawal penalty if you withdraw funds from your Individual Retirement Account (IRA) before the age of 59½.

However, there are exceptions to this rule.

If you believe one (or several) of these exceptions might be in your future, it’s good to be aware of them for your own planning.

It can highlight the need for further research and planning.

Traditional IRA: Summary of Exceptions to the Early Withdrawal Penalty (2024)

- Age: After the participant/IRA owner reaches age 59½.

- Disability: If you become permanently and totally disabled, you can withdraw funds penalty-free from both Traditional and Roth IRAs.

- Medical Expenses: You can withdraw amounts up to your unreimbursed medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI) in a calendar year.

- Homebuyers: Qualified first-time homebuyers, up to $10,000.

- Birth or Adoption: Distributions up to $5,000 per child for qualified birth or adoption expenses.

- Death: There is no penalty for the IRA beneficiaries to withdraw funds upon the original IRA owner’s death.

- Education: Qualified higher education expenses.

- Medical Health Insurance: Premiums paid while unemployed.

- Disaster Recovery: Distribution up to $22,000 to qualified individuals who sustain an economic loss due to a federally declared disaster where they live.

- Emergency Personal Expense: One distribution per calendar year for personal or family emergency expenses, up to the lesser of $1,000 or vested account balance over $1,000 (provided these distributions have been made after 12/31/2023).

- IRS Levy: If the IRS levies your IRA to satisfy a tax debt, the withdrawal is not subject to the penalty.

- Domestic Abuse Victim: Distribution to a victim of domestic abuse by a spouse or domestic partner, up to the lesser of $10,000 or 50% of account (provided these distributions have been made after 12/31/2023).

- Emergency Personal Expense: One distribution per calendar year for personal or family emergency expenses, up to the lesser of $1,000 or vested account balance over $1,000 (provided these distributions have been made after 12/31/2023).

- Military: Certain distributions to qualified military reservists called to active duty.

This is a general list of exceptions, and the specifics of each exception vary.

The Next Step: It can be beneficial for you to consult with a qualified tax advisor if you believe these might apply to your specific situation.

Traditional IRA: Required Minimum Distributions (RMDs)

Required minimum distributions (RMDs) are the minimum amounts you must withdraw from your retirement accounts, which include traditional IRAs, SIMPLE IRAs, and SEP IRAs, each year.

In 2024, you generally must start taking withdrawals from your traditional IRA when you reach age 73 on or after January 1, 2023. This date is called the required beginning date.

Specifically for 2024, you can take your first RMD by December 31, 2024, or choose to take your first RMD until April 1, 2025. In the scenario where you wait until April 1, 2025, for your first RMD, then you will have to take a second RMD by December 31, 2025.

While a traditional IRA owner must calculate the RMD separately for each IRA they own, they can withdraw the total amount from one or more of the IRAs.

Traditional IRA: Beneficiary Designation

We understand how hard it can be to think about what happens after you are gone.

If you would like your loved ones to benefit from your IRA assets after your death, we’re here to help coordinate your wishes.

When you die, the assets you’ve carefully saved in your IRA go to those you’ve laid out in the IRA beneficiary designation form.

Most folks tend to choose individuals as beneficiaries. Maybe they leave everything to their spouse or divide it equally among their children (i.e. per stirpes). Some even choose to leave their assets to charities, making one last act of kindness.

Alternatively, you can also name a trust as your IRA beneficiary.

There are rules investors like you can use to determine required minimum distributions (RMDs) for beneficiaries. These rules are governed by whether:

- The beneficiary is the surviving spouse.

- The beneficiary is an eligible designated beneficiary other than the surviving spouse.

- The beneficiary is an individual, other than an eligible designated beneficiary.

- The beneficiary isn’t an individual (e.g. the owner’s estate or trust).

- The IRA owner died before the required beginning date, or died on or after the required beginning date.

The right IRA beneficiary can be different from one person to the next. You should carefully consider your choice in light of your of personal circumstances.

The Next Step: It’s important to review your account beneficiaries regularly, especially if key aspects of your personal or financial life have changed significantly.

Traditional IRA: Investment Options

Like a workplace retirement account, a traditional IRA can provide you with investment flexibility. IRA investment options are broader relative to a typical 401(k) plan. With a traditional IRA, you can select what you invest in, as well as how much and when you invest. Remember to stay within the contribution limits, though.

Mutual Funds, exchange traded funds (ETFs), and bonds are all potential investment options for IRA owners.

IRAs cannot invest in life insurance or collectibles, such as art, antiques, gems, coins, or alcoholic beverages. IRAs can invest in certain precious metals only if they meet specific requirements.

Traditional IRA: Asset Location

Your personal situation and investing goals can help shape your asset allocation. Generally speaking, this is the mixture of equity-like and bond-like investments you own. Once you establish the right asset allocation for you, it can then help guide your asset location. Meaning, the type of accounts you hold investments in.

Long-term investors can take a comprehensive view across all of their investment accounts, not just on an account-by-account basis. Your money should work together, and you can make sure your traditional IRA and taxable accounts are working together toward your goals.

Since Traditional IRAs are tax-deferred accounts, long-term investors like you can factor in the tax efficiency of a specific investment. After-tax returns matter. Investors can look to minimize the effects of taxes on investment returns by placing different types of investments in tax-advantaged accounts or taxable accounts based on the tax treatment of the account and their personal circumstances.

Generally speaking – and quite a bit of ink has been spilled on this topic – long-term investors will seek to hold taxable bonds and taxable bond funds in a traditional IRA. Asset location is a broader lens that you can apply to all your investment accounts. It’s something that needs to be personalized to fit your specific facts and circumstances.

Traditional IRA: Creditor Protection

While Individual Retirement Accounts (IRAs) offer benefits for your retirement savings, their vulnerability to creditor claims requires consideration and varies by state.

For IRAs, there are different statutes and specific case law in each state. While the details are beyond the scope of this article, the extent of an IRA’s creditor protection can depend on multiple factors, including: your state of residence, the type of IRA, the IRA’s origin (e.g. inherited IRA), and type of creditor claim.

The Next Step: If you need to understand how creditor protections apply to your specific situation, consulting with a qualified attorney who can effectively engage in asset protection planning is a good starting point.

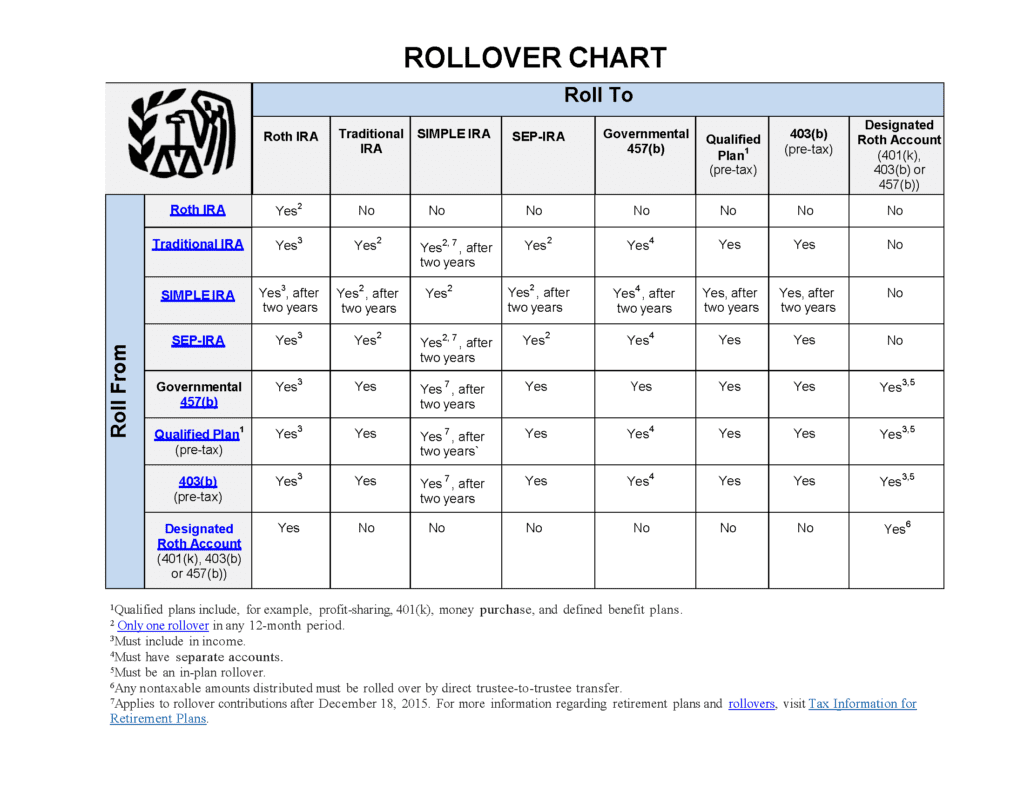

Traditional IRA: Rollover Considerations

If you are contemplating investing in a traditional IRA, then understanding the account rollover rules could help you plan ahead.

These rules govern how you can transfer assets held in these accounts to other types of accounts.

Below is a chart showing the different ways specific account types can, and cannot, transfer to other types of accounts.

Source: https://www.irs.gov/pub/irs-tege/rollover_chart.pdf

Spousal IRA: Overview

A spousal IRA is a special provision that allows a spouse to contribute to an individual retirement account (IRA) based on their working spouse’s income. The IRA can be either a traditional IRA or a Roth IRA. You’re a team, right?

For 2024, if you file a joint return and your taxable compensation is less than that of your spouse, the most that can be contributed for the year to your IRA is the smaller of the following two amounts:

- $7,000 ($8,000 if you are age 50 or older).

- The total compensation includible in the gross income of both you and your spouse for the year, reduced by the following two amounts.

- Your spouse’s IRA contribution for the year to a traditional IRA.

- Any contributions for the year to a Roth IRA on behalf of your spouse.

Given this, the total combined contributions you can make to your IRA and your spouse’s IRA in 2024 can be as much as:

- $14,000 if you are both under age 50.

- $15,000 if only one of you is age 50, or older.

- $16,000 if both of you are age 50, or older.

Summary

Hopefully you found this overview of the traditional IRA essentials helpful and educational.

What works well for one person might not be the perfect fit for another. When evaluating what type(s) of IRAs best align with your goals, you’ll want to fully incorporate all the moving parts of your financial life into your decision.

If you are interested in working with an advisor to make sure all these pieces fit together to support your goals and values, we’d be honored to learn more and explore how we might be able to help you.

Make sure you understand the tax implications of investing in a traditional IRA and consider whether to consult a qualified tax professional.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.