If you died, how would your assets transfer to your loved ones? Beneficiary designations are a key element of your estate plan. Your beneficiary designations ensure your assets are passed along according to your wishes. It can be easy to overlook beneficiary designations on your accounts.

Learning Points

While a will or trust can instruct your family, or estate, about how your assets will be distributed, they are not the only components of an estate plan. Beneficiary designations are another important element of your complete estate plan. They can guide your family or estate on how you want your assets transferred after your death.

Read on to gain, or refresh, your working knowledge of beneficiary designations. Apply this knowledge to your own life and get organized. Reaffirm how you are using beneficiary designations in your own estate planning.

What is a beneficiary designation?

The beneficiary designation allows you to specify who receives your account’s assets after you are gone. A beneficiary can be an individual or entity. A beneficiary does not have any ownership rights, access, or control of an account while you are alive.

Your primary beneficiary is the person or entity you name in your last will and testament, or trust. Your primary beneficiary is who you want first scheduled to receive a distribution.

For instance, if you name your daughter as the beneficiary of your bank account, your daughter will not have access or control of your bank account simply because she is named as a beneficiary.

Additionally, you are not limited to just one beneficiary. You can have multiple beneficiaries. You do need a beneficiary on your account if you do not want your estate to have to go through probate court.

Prioritizing your beneficiary designations matters. When you choose someone, or your trust, to be your account’s beneficiary, in most cases, that designation overrides any language you have in your will about the matter.

You want to be confident in who you name as your beneficiary, so take your time and think through these choices using a long-term perspective.

Primary vs. Contingent

In the context of your estate plan that includes a trust, you can think of the contingent beneficiary designation as:

- The person or entity that you want to receive a trust (or estate) distribution, but only if the primary beneficiary has passed away, or is unable or unwilling to accept the distribution.

This role is sometimes referred to in the following terms:

- remainder

- remainderman

- secondary

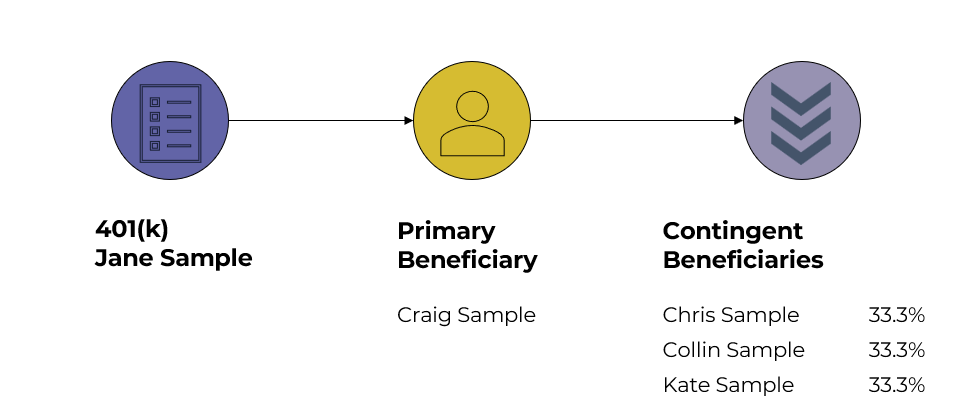

The diagram below shows the relationship between a 401(k) account for ‘Jane Sample’, her husband ‘Craig Sample’ as the primary beneficiary and their three children as contingent beneficiaries.

Where to start?

Now that you understand what a beneficiary is, you can determine where they can or should exist in your financial life.

As a starting point, review the following account types to confirm who you’ve designated as a beneficiary:

- Employer sponsored retirement plans: your 401(k), 403(b), 457s and other profit-sharing plans.

- Individual Retirement Accounts: your traditional IRA, Roth IRA, SEP IRA, and SIMPLE IRA.

- Life insurance policies: your term life, whole life, or universal life policies.

- Annuity products: if you have a fixed annuity or variable annuity, for example.

- Other employer-sponsored plans: company stock options, restricted stock units, deferred compensation, and defined benefit plans.

Additionally, you’ll want to review your bank accounts. Specifically for your bank accounts, a payable on death (POD) designation means your bank account automatically transfers to the named beneficiary upon the death of all account owners and co-owners.

What if I have young children?

If you have young children, especially kids under the age of majority in your home state, you should consider speaking with an estate planning attorney about creating a trust.

Your trust can help you detail who controls your assets, how and when you want your money distributed to your children, as well as other provisions.

An estate planning attorney can help you and your spouse think through and memorialize, how best to protect and thoughtfully distribute your assets according to your wishes.

Your Will and Trust

Like a lot of financial planning, it can help you to take a step back from a specific topic to see where it fits into the bigger picture. It can reinforce or clarify your understanding, as well as understand how the specific puzzle pieces fit together.

As a quick refresher, your will provides for the probate administration of any assets that:

- you own individually at the time of your death;

- are not held jointly with one or more people;

- and do not have a valid beneficiary designation.

If you have a living trust, the purpose of your trust is generally to:

- provide for the continued management of your assets during your lifetime in the event of your disability,

- avoid the expense and delay of probate at the time of your death, and

- provide for the disposition of your assets after your death in accordance with your wishes.

If you have a trust and want to understand how a beneficiary fits into your estate plan, start by reviewing your trust’s instructions for funding. Particularly the titling and transfer instructions.

A Common Experience

You might not have thought about this topic since you initially opened your account. It might have been a while since you last reviewed your beneficiaries. It’s a helpful habit to review these designations periodically, as your finances, relationships or circumstances change.

You would not want an outdated family relationship or deceased loved one to remain the beneficiary of your account.

It can be challenging to keep track of all your designated beneficiaries. There is no national reporting mechanism, no centralized clearinghouse for accounts and designated beneficiaries.

Unlike the 1099-related documents you receive in the early part of each year, your financial institution is unlikely to ask you to review and update your designated beneficiaries.

And so, each time you update your estate planning documents, you’ll want to review a complete list of your accounts, policies, etc. where you should have a designated beneficiary.

Here’s one approach to consider.

Use your Personal Net Worth Report to Stay Organized

Whether you have a potpourri or a plethora of accounts, beneficiary management can be administratively burdensome – at least initially.

One way you can create clarity and understanding for you and your spouse is to inventory your accounts and their key details into a single document.

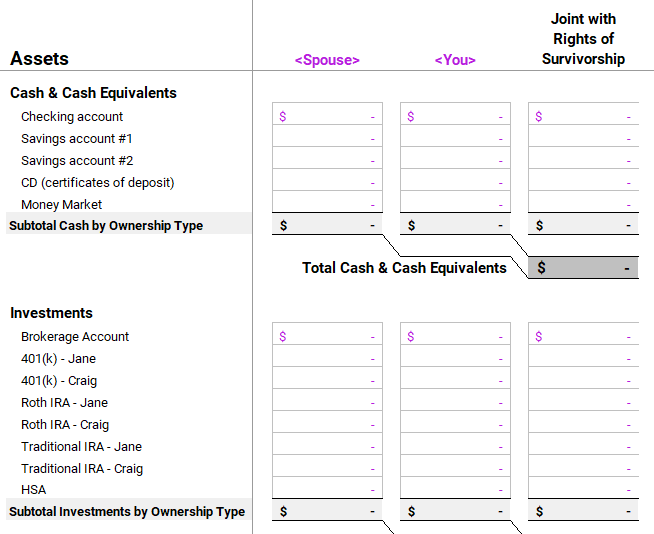

Start with all your accounts, insurance policies, and annuities listed on your personal net worth report.

If you don’t have a personal net worth statement, you can download your free, personal net worth and cash flow report template here.

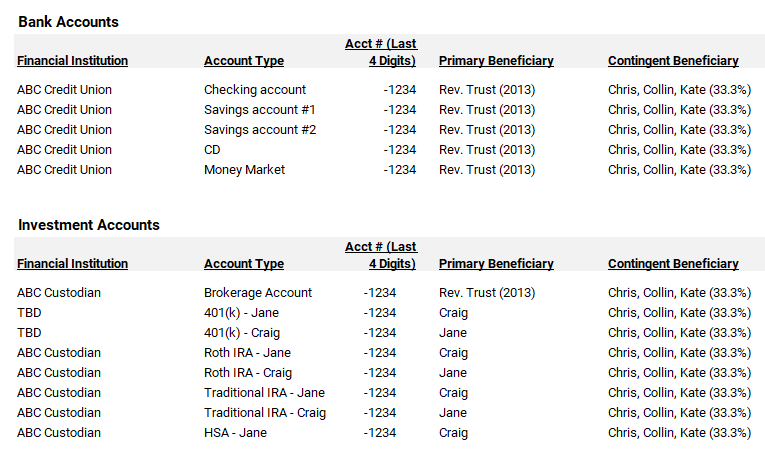

You can choose to include details like those shown in the report template below:

You might also consider including contact details such as their phone number, email address, mailing and address. Once you’ve consolidated these details, you can quickly reconcile and update your account inventory as your life changes.

For most long-term investors like you, this becomes an easy to manage process. If you’re partnered alongside a financial planner, it should be even easier.

This document can serve as a valuable reference point when you are considering updates to your estate plan or when your family relationships evolve.

Your up-to-date account inventory can guide your spouse if you are no longer around.

Store this document in a secure location. Strongly consider using multifactor protection and a unique password to protect this specific document. Consider storing a physical copy alongside your estate documents.

The Next Step

Review your personal net worth report and confirm whether each of your accounts has the proper beneficiary designation.

If you come across an account and you’re unsure who the beneficiary should be, consider reviewing your instructions for funding and titling your trust.

Working with a financial planner can provide you with the right mix of accountability, thoughtfulness, and long-term thinking. Your financial planner can help you get un-stuck by simplifying what you need to do into manageable goals.

Who is providing you with the right kind of accountability in your personal financial life?

Because this topic, like so many others in financial planning, intersects with the world of estate planning, make sure you coordinate with a qualified estate planning attorney.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.