There’s never been a better time to check how you are making use of your employee benefits. While you’re in review mode, reaffirm that your 2024 savings priorities are on track.

Learning Points

The trees are finally leafed out around your home. Your first few mows of the season are in the books. You’ve spent some time in the sunshine getting ready for spring.

Or, you’ve completely neglected the yard and whatever is left of the garden. Instead, you supported your kids’ weekend activities and sports interests.

Now, consider a brief pause from your spring activities and, instead, check-in on your employee benefit utilization and savings priorities. Provide some accountability for yourself and confirm that your savings automations are working as you intended.

Working with a financial planner can provide you with the right mix of accountability, thoughtfulness, and long-term thinking. Your financial planner can help you prioritize your next steps and focus your energy toward measurable and actionable goals.

Who is providing you with the right kind of accountability in your personal financial life?

The following is a list of employee benefits and savings priorities to (re-)evaluate, and some practical questions to help you think through this area of your financial life.

Each of these topics might not apply to your current situation. It’s worth being aware of them, they could become opportunities for you to explore in the future.

Your Employee Benefits

Dependent Care Flexible Spending Account (DCFSA)

For this benefit, there are several elements to consider for your specific situation: your tax filing status, federal and state tax rates, and your previous year’s compensation.

In 2024, the maximum amount you can defer from your compensation to your DCFSA is:

- $5,000 for single taxpayers and married couples filing jointly.

- $2,500 for married couples filing separately.

If you are categorized as a highly compensated employee (HCE) by your employer, then your maximum dependent care benefit could be reduced. In the context of your DCFSA in 2024, you are generally considered a highly compensated employee (HCE) if you are:

- A more-than-5% owner of the employer at any time in the current or preceding plan year; or

- An employee who earned more than $150,000 in the prior plan year.

Source: IRS Publication 15-B – 2024

The next step: If you’ve chosen to contribute to your dependent care FSA in 2024, verify that you’re on track with your anticipated spending and reimbursements. Here are some practical questions and considerations to help guide your review of this account:

Do you have all the required receipts and related documentation you need to submit these expenses for reimbursement?

Verify that your dependent care provider provides the following documentation:

- Name of dependent receiving care

- Amount you paid for service

- Type of service (day care, day camp, after-school, elder care, etc.)

- Provider name and address

- Date(s) of service

How much – or how many more months – of eligible dependent care expenses do you need to incur to get fully reimbursed for this benefit?

Curious to project your own tax savings from this benefit? Aside from creating your own spreadsheet, consider reviewing your particular facts and circumstances with your financial planner. Keep in mind that you’ll want to compare the benefits of the DCFSA against the federal dependent child tax credit.

Looking Ahead

This summer, consider taking notes about the costs of eligible summer camps that you’d like your children to experience next year. Knowing these types of cost estimates can better inform your benefit elections for the next plan year.

The fall benefits enrollment season and January summer camp sign-ups will be here before we know it.

Do any of your children qualify for traditional daycare expenses? Or is your child moving to kindergarten?

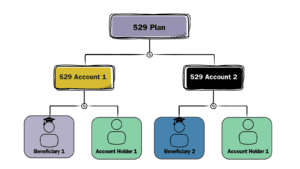

If your children attend private elementary school, consider whether using a 529 account to pay for tuition or save for future education costs is right for you.

Health Flexible Spending Arrangement (FSA)

Taxpayers like you can use your FSA funds for qualified medical expenses not covered by their health plan, such as:

- Co-pays

- Deductibles

- Medical products

- Services ranging from dental and vision care

- Eyeglasses and hearing aids

The maximum you can contribute to an FSA for tax year 2024 is $3,200.

If you and your spouse are each eligible to participate in your respective employer’s health FSA, you could each fully fund your FSA. And so, a married couple could make up to $6,400 in health FSA contributions in 2024.

FSAs are generally a “use-it-or-lose it” type of account. You do not want to overcontribute to your FSA for any given plan year.

The next step: Do you have eligible expenses you can submit for reimbursement? If not, consider reviewing your projected health care expenses for the remainder of the year.

Set a reminder to revisit your progress on FSA reimbursement later in 2024.

Looking Ahead

- Does your plan allow carryovers – or – a two-and-a-half-month grace period after the end of the plan year? Currently, plans can only provide one of these two features.

- Consider this, if you have the carryover feature, and your spouse has the grace period feature, map out how much and in which FSA(s) you should contribute.

- In 2024, the most you can carry over to a 2025 FSA is $640 of unused FSA contributions.

- If either you or your spouse feel your current employment situation is on shaky ground or you plan to change employers soon, you might need to evaluate how much FSA funding you want to elect during your next open enrollment period.

FSAs are employer accounts. As such, health FSAs are not portable should you find yourself unemployed or changing employers. Your FSA contributions could potentially be lost if you lose your job or leave your current company.

Health Savings Account (HSA)

HSAs and health flexible spending accounts (FSAs) both enable you to contribute your earned compensation before it’s been taxed, to pay for health care costs.

If you have an HSA you likely already understand how these accounts work and why they can be powerful retirement savings vehicles.

Your HSA is a personal savings account that individuals can use to pay for qualifying medical expenses. Health Savings Accounts are paired with high-deductible health plans (HDHPs). HDHPs generally have lower monthly premiums compared to traditional health insurance plans but require individuals to pay a higher deductible before their insurance coverage begins.

If you want a brief refresher on HSAs, you can start by exploring these highlights.

Here are some questions below to guide your review of your HSA account(s):

- Are your contributions accumulating in your HSA?

- How are you investing your HSA contributions to support your savings priorities?

- Are your investments low-cost, low-turnover funds, or are there other options you need to consider?

Tax Withholdings and Estimated Payments

The amount of taxes withheld from your paycheck will depend on how much you earn each pay period. Your paycheck tax withholdings also depend on the information you provided to your employer on your most recent Form W-4. Ideally, you should review this information once a year.

How much you earn and your W-4, as well as information like your filing status, can affect the tax rate used to calculate your tax withholding.

Consider these additional sources of income you might have overlooked:

- Do you have any self-employment income?

- Have you received any traditional IRA or certain Roth IRA distributions?

- Do you have any new investments with taxable income that is not subject to withholding?

- Interest income

- Dividends

- Capital gains

- Perhaps you’ve moved into a new role and now receive periodic bonuses. Have you confirmed with your HR team how you wish the bonuses to be treated for withholdings and retirement plan contributions?

Looking ahead: Do you have reminders set so you can make the estimated payments that your qualified tax professional has recommended for you?

Revisiting Your 2024 Savings Priorities

Now that you’ve reviewed some key employee benefits, check your progress on your top savings priorities. These savings priorities are designed to build a strong foundation for your personal finances.

- Your emergency fund: It’s important to prioritize liquidity. Emergencies rarely announce themselves in advance. If you have 3 months saved to your emergency fund, consider contributing more to your emergency fund.

- Optimizing your 401(k) contributions for a company match: This is a benefit that many companies offer their employees and one that you should try to maximize each year.

- Eliminating high-interest credit card debt: High interest rates can make it challenging to build wealth in the long term, so it is important to prioritize paying off all your credit card debt.

- Adequate insurance coverage: If you have a family or significant assets to you and you don’t have the right amount of home, auto, life, umbrella, and/or disability insurance. Seek out unbiased, objective perspectives from someone whose interests are aligned with your own.

- Estate planning essentials: Estate planning is the process of organizing and expressing your wishes for the management and distribution of your assets after your death. The planning you do in this area of your life can help ensure that your children are taken care of, and your assets are distributed according to your wishes.

- Education Funding (529s): A 529 account can help you work toward your education funding goals. A tax-advantaged investment program designed to help families save for higher education expenses.

- Roth IRAs: If you’re saving for retirement, a Roth IRA can provide investors like you additional flexibility on your retirement path. Learn about the essentials of the Roth IRA in 2024.

- Maximizing your retirement plan contributions: Maximizing your contributions to a 401(k), 403(b), Roth 401(k), or 457(b) account can help you save for retirement.

- Paying off lower-interest debt: It may be beneficial to pay off lower-interest debts, such as a car loan, a personal loan with a low interest rate, before tackling other debts.

- Taxable investment accounts: By opening a taxable investment account, you can set aside money for mid-term needs and wants such as an anniversary trip, a wedding, a home addition, a vacation home, a rental property, or a new business venture.

Your savings priority strategy sequences contributions to your specific financial needs and their related investment accounts.

While this strategy can be effective and transformative to your personal finances, like all things personal to your finances, you’ll want to customize it to your specific situation.

Align these investments with the time horizon of your specific goals.

Because these topics, like so many others in financial planning, can intersect with the world of tax and estate, make sure you coordinate with a qualified tax professional and estate planning attorney.

The Next Step

Ideally, when you use this savings priority strategy, you fully fund each priority before turning your attention to the next priority.

When you’re comfortable that you’re minimizing your taxes, your living expenses are dialed in and aligned with your values, it becomes easier to save the right amounts toward your future goals/savings priorities.

When you know where you’re going financially and know who and what are truly important to you in life, you can create incredible clarity about your spending and saving.

You can confidently spend on the things that matter, and confidently decline to spend on things that aren’t aligned with what you want in life.

The sooner you are able to thoughtfully execute on this approach, you’ll increase the likelihood of achieving your goals, setting new ones, and enjoying the present moment.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.