If you died, how would your assets transfer to your loved ones? Account titling is a key element of your estate plan. Account titling determines who can manage the specific asset during your lifetime. It also helps determine how your assets are distributed upon your death.

Learning Points

Aligning Your Account Titling and Your Estate Plan

Account titling refers to how you own an asset—individually, jointly, in a trust, or another entity. Asset or account titling affects who controls it, related tax consequences, accessibility to creditor claims, as well as inheritance, which makes it critical element of your estate plan.

Even the best plans can fail if you don’t align your account titling with the rest of your estate planning goals.

While a will or trust can instruct your family, or estate, about how your assets will be distributed, they are not the only components of an estate plan. If your estate plan involves a living trust, your estate plan depends on you correctly funding your trust.

To properly fund your trust, correctly transferring your intended trust assets into the trust can often involve updating the title of the assets. If you do not transfer your assets to your trust, those assets might not pass to your intended beneficiaries.

You can use this information to better understand how account titling fits into your personal situation. Or perhaps it inspires you to finish any outstanding account titling you need to complete to get your estate plan up to date.

Who Benefits When You Title Accounts and Designate Beneficiaries?

If you died, how would your assets transfer to your loved ones? While a will or trust can instruct your family, or estate, about how your assets will be distributed, they are not the only components of an estate plan. There are two concepts you should be aware of now that could simplify things for your loved ones later. Proper account titling and beneficiary designations can help determine how your assets will transfer.

Your approach to asset or account titling determines how you want to manage your assets during your lifetime. It also helps determine how your assets are distributed upon your death according to your will based on state law, agreement, or beneficiary designation.

A clear plan to take care of your loved ones after your death is a critical element of your financial plan.

If you do not have a trust or a will, then the laws of your state, also known as intestacy laws, will most likely govern the distribution of your estate.

When your money has meaning, it can be easier to intentionally save and spend your money in ways that are aligned with your values and goals. Your estate plan can specify how your assets, such as your home, investments, or life insurance, will be passed on to your loved ones after you are gone. How you title these assets and designate beneficiaries can significantly impact how smoothly things go for your family.

Asset titling is the ownership of an asset. Titling your assets can be done in your individual name, jointly with someone else, in a trust or entity, etc.

When you take the time to address essential estate planning elements, like account titling, you can make sure your loved ones are taken care of later.

Now that you understand what account titling is and who can benefit from your thoughtful estate planning, you can determine where asset titling can exist in your financial life.

Getting Organized: A Practical Perspective on Where to Start

If you have a trust and want to understand how to align your account titling with your estate plan, start by reviewing your trust’s instructions on funding and administration. Particularly the titling and transfer instructions. If you are unsure, first consult with your estate planning attorney.

As a starting point, review the following types of assets to confirm you’ve aligned the account titling with your estate plan:

- Bank Accounts: savings, checking, and money market accounts as well as safe deposit boxes.

- Life Insurance Policies: your term life, whole life, or universal life policies.

- Real Estate: your primary home, secondary homes (rental or vacation), land and commercial properties.

- Collector/High Value Vehicles: rare luxury automobiles and RVs, for example.

- Other Entities: i.e. limited liability company.

Remember, if you have a revocable living trust, chances are you trying to achieve some combination of the following:

- Avoiding the expenses, delays and publicity associated with the probate process.

- Creating a solution that manages your assets should you become disabled or incapacitated.

- Funding the trust in such a way that it maximizes your tax planning.

If You Have a Trust…

A revocable living trust can manage your assets while you are alive and make sure those assets go to the right people when you are gone. With this kind of trust, you retain control over your assets and can make changes if your circumstances change during your lifetime.

When you pass away, the trust becomes irrevocable, and your trust assets can be distributed to your heirs without having to go through the probate process.

Probate is the formal, court-supervised process of carrying out your last wishes. A probate court will validate your last will and testament (if it exists), resolve any outstanding debts or taxes, and distribute any remaining assets to rightful heirs.

Setting up a trust can be relatively more expensive and time-consuming than some other estate planning options, but it can also provide more flexibility and control. It is a good idea to talk to a qualified estate planning attorney to see if a trust is right for you and your situation.

For married couples, there are several types of assets that may transfer by operation of law, either upon the death of one spouse or upon divorce. These types of assets are generally referred to as “non-probate assets.”

- Jointly owned assets: Assets that are owned jointly with rights of survivorship – sometimes abbreviated as JTWROS – like a joint bank account or jointly owned real estate. If you have assets with this ownership type, these assets will automatically pass to the surviving joint owner upon the death of the other joint owner. The owners can transfer or sell their interest during their life. However, a joint owner cannot leave or donate the interest at their death. It does not allow the deceased’s share of the property to pass into their estate.

- Assets with beneficiary designations: Assets that have a designated beneficiary, such as life insurance policies, retirement accounts, or payable-on-death (POD) bank accounts, will pass to the designated beneficiary upon the death of the owner.

Beneficiaries are the people who will receive your assets when you are gone. They don’t have any ownership rights while you are alive, and your assets are protected from creditors, bankruptcy, and divorce if you have properly designated beneficiaries. It’s a good idea to review your beneficiary designations periodically, as your life and circumstances change over time.

- Community property: In community property states, assets acquired during the marriage are owned equally by both spouses and will pass to the surviving spouse upon the death of the other spouse, unless there is a valid will or trust in place directing otherwise.

These types of non-probate assets are generally not subject to the probate process. Instead, they pass directly to the surviving joint owner or designated beneficiary.

A Practical Consideration: Estate Liquidity

Like many financial planning topics that intersect with the world of estate and tax planning, it’s important to create a balanced and personalized approach that works for you and your loved ones.

Managing your estate’s liquidity is another consideration to factor into your planning. Estate liquidity is your estate’s ability to pay all its final expenses on time and without the need to sell assets quickly (and/or less than market value).

And so if you, or a loved one, have a significant amount of wealth attributable to illiquid assets like a business, real estate, or collectors items, creating estate liquidity might be a higher priority in your financial planning.

If your estate does not have enough cash or readily marketable securities to pay for your burial expenses, final bills, or taxes you might owe, that could put undue stress of your loved ones. When you can estimate these final expenses, the better prepared you will be to avoid significant estate liquidity issues.

A Practical Consideration: FDIC and NCUA Coverage

As you review your account titling, and in particular your bank accounts, you should also consider how your account titling changes FDIC or NCUA coverage. Your account’s ownership type (individual, joint, trust, etc.) is factored into the FDIC and NUCA coverage. Each ownership category has separate limits.

For your bank accounts: review your FDIC insurance coverage with the FDIC’s calculator.

For your credit union accounts: review your NCUA Share Insurance with the NCUA’s estimator tool.

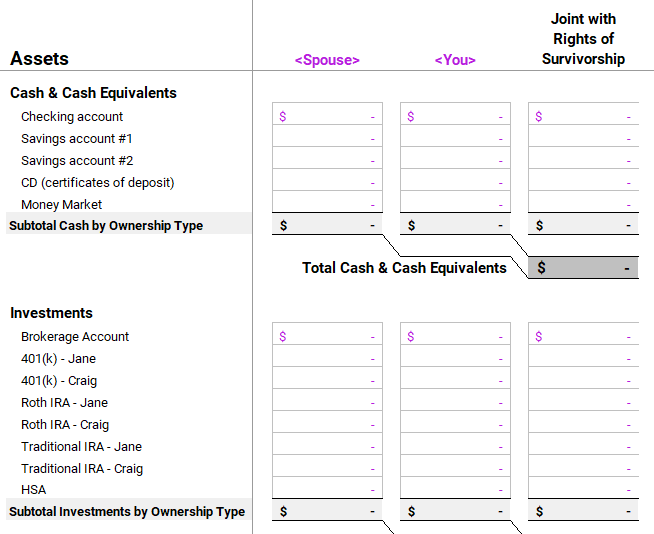

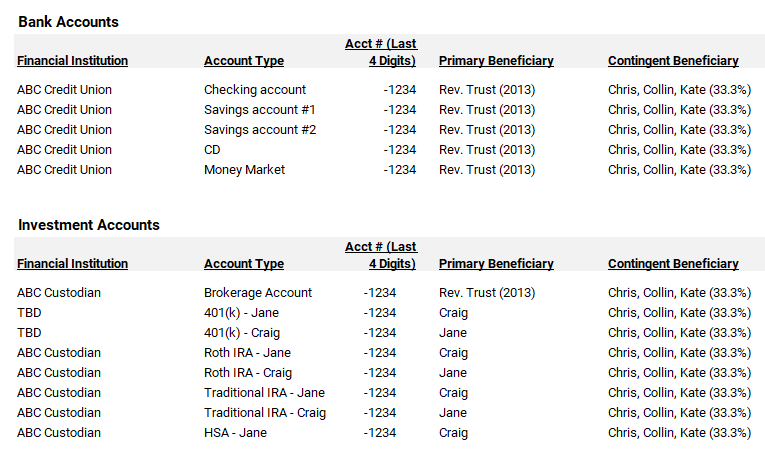

Use your Personal Net Worth Report to Stay Organized

Your account titling and beneficiary management can be administratively burdensome – at least initially.

One way you can create clarity and understanding for you and your spouse is to inventory your assets and accounts and their key details into a single document.

Start with all your accounts, insurance policies, and annuities listed on your personal net worth report.

If you don’t have a personal net worth statement, you can download your free, personal net worth and cash flow report template here.

You can choose to include details like those shown in the report template below:

You might also consider including contact details such as their phone number, email address, mailing and address. Once you’ve consolidated these details, you can quickly reconcile and update your account inventory as your life changes.

For most long-term investors like you, this becomes an easy to manage process. If you’re partnered alongside a financial planner, it should be even easier.

This document can serve as a valuable reference point when you are considering updates to your estate plan or when your family relationships evolve.

Your up-to-date account inventory can also guide your spouse if you are no longer around.

Store this document in a secure location. Strongly consider using multifactor protection and a unique password to protect this specific document. Consider storing a physical copy alongside your estate documents.

The Next Step

Proper account titling and designating beneficiaries are important parts of making sure your loved ones are taken care of after you are gone. Your estate planning efforts can help ensure how your preserve your wealth – and make sure your heirs use it for its intended purpose.

Poor planning can expose your family to legal proceedings, weak asset protection, unnecessary taxes, probate fees, and more.

There is no single solution to estate planning and the way someone wishes to distribute their estate depends on their personal and family situation, as well as their values, resources, and goals.

Keep in mind that account titling and beneficiary designations are just one part of a complete estate plan.

If you do not have an estate plan, consider consulting with a qualified estate planning attorney. One who understands your state’s laws and who can create a thoughtful solution for your personal situation. You should consult with your estate attorney before retitling accounts or adding beneficiary designations to accounts that aren’t aligned with your existing trust titling and transfer instructions.

It’s important to filter your decisions with the knowledge that your account titling and beneficiary designations won’t automatically change when your life does. How you title your accounts and assets will affects who controls the assets, how your assets are distributed, tax consequences, whether or not they need to go through probate, and whether the assets are subject to creditors’ claims.

Consider all the elements of your financial life when you are planning for what will happen to your assets after you are gone.

When you know who and what are truly important, you can create incredible clarity about your spending and saving.

Clarity to confidently spend on things that matter. Clarity to avoid spending your hard-earned resources on things that aren’t aligned with what you want in life.

As your financial planner in Saint Louis, we can help you plan for the future and enjoy the present moment.

Frequently, proactive and open collaboration with your tax and estate planning professionals can help you work towards your financial planning goals. Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.