Explore how charitable bunching and donor advised funds work and the potential tax planning opportunities they create. This educational overview can help you to be more informed and prepared in your own philanthropy. Give your money more meaning using strategic charitable planning.

Learning Points

Giving Your Money Meaning

When you donate your time, your energy, or your money to charity, it can be a powerful experience.

There is a reciprocal nature to intentional philanthropy. One that goes beyond the immediate benefits your volunteerism or charitable donation provides to an organization.

At its core, there is an underlying message that you’re communicating to yourself and your family. That message is more of a feeling; that feeling of enough. Of abundance and fulfillment.

When you make the time to directly volunteer for a charity to support its mission, you can show your children how they can connect words and values to the real work of helping others. You lead by doing.

When you donate money or other assets to a charity, you signal to yourself that you’re going to be O.K. financially. That you have enough. It dials down the noise from the world around us. It pushes back on the notion that you need more. More stuff. More money.

The feeling of “enough” can be a calming force, especially in the context of your financial plan.

You can align your financial plan with directly supporting causes and organizations that matter to you and your family. When you take a strategic view of your philanthropy and combine it with thoughtful tax planning, you can efficiently share your resources with deserving public charities.

Read on to explore how donor advised funds work and the potential tax planning opportunity they create. Understand how different types of charitable donations compare to one another on an after-tax basis.

Because topics like charitable giving, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with a qualified tax professional.

Tax Planning: Charitable Contributions

If you’re considering donating money to charity and want to understand how it might influence your tax situation, evaluate whether you plan to itemize or take the standard deduction in a given tax year.

For taxpayers who itemize their deductions, charitable contributions, state and local taxes, and home mortgage interest are relatively common. This is especially true for taxpayers in high marginal tax brackets. If the sum of these itemized deductions is greater than your standard deduction, work with your qualified tax professional to determine the right deduction strategy for you and your family.

If you plan to take the standard deduction, remember that the temporary deduction for charitable cash contributions for taxpayers who do not itemize their tax returns has expired at the start of taxable year 2022.

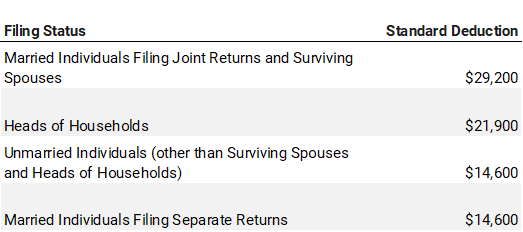

In general, for taxable years beginning in 2024, the standard deduction amounts are as follows:

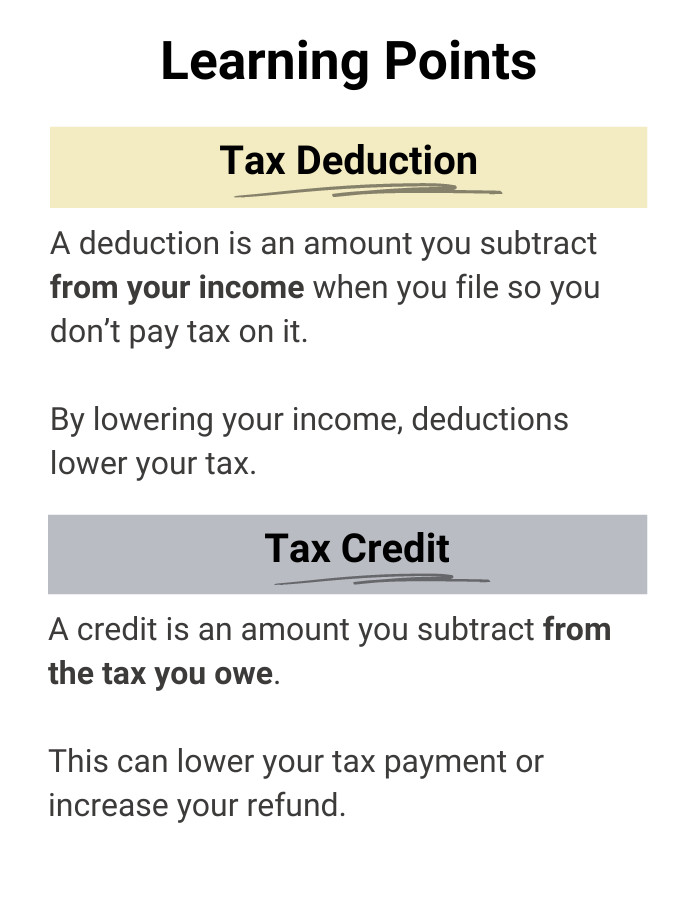

Tax Deductions vs. Tax Credits

As a quick refresher, remember the distinction between tax deductions and tax credits.

The amount you save with a deduction depends on your tax bracket. For example, if you’re in the 37% tax bracket, a $1,000 tax deduction would save you $370 off your tax bill.

A tax credit reduces your total tax bill. For example, a $1,000 tax credit would save you $1,000 off your tax bill.

Charitable Bunching

If you regularly give set amounts of money to charity, but don’t have enough qualifying itemized deductions in a given tax year, evaluate whether a planned charitable bunching strategy aligns with your long-term goals and values.

Charitable bunching occurs when you aggregate your charitable contributions for multiple years into a single year so that you can itemize your tax deductions in that year. In subsequent years you could then re-evaluate whether the standard or itemized deduction decision is right for you.

If you are on the threshold between taking the standard deduction or itemizing to maximize your tax benefits, charitable bunching is worth evaluating in detail.

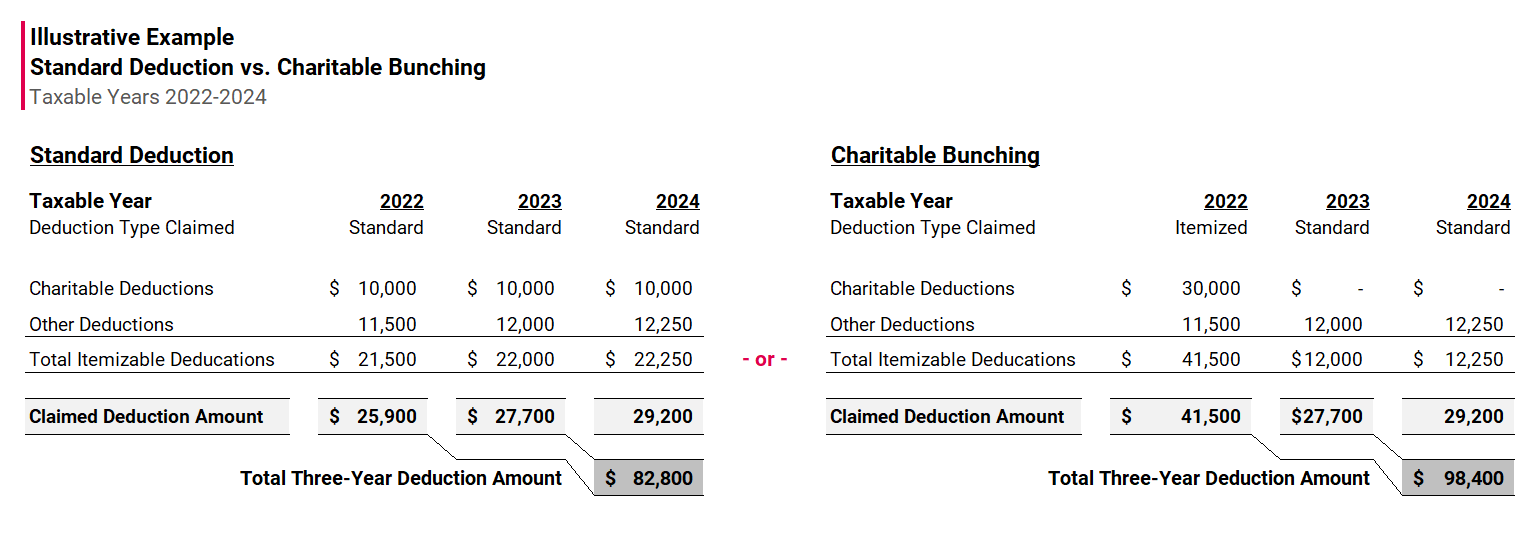

Illustrative Example: Standard Deduction vs. Charitable Bunching

To show how choosing the standard deduction compares to charitable bunching, consider the following illustrative example.

In the Standard Deduction hypothetical scenario, a couple who are married filing jointly contribute a fixed amount to charity in taxable years 2022, 2023, and 2024. They would claim the standard deduction in each of those taxable years. As such, they would have $82,800 in total claimed deductions.

In the Charitable Bunching hypothetical scenario, a couple who are married filing jointly contribute three years-worth of charitable donations in taxable year 2022. They would not claim any charitable deduction in taxable years 2023 and 2024. They itemize their deductions in taxable year 2022, and claim the standard deduction in 2023 and 2024. As such, they would have $98,400 in total claimed deductions.

The difference in these two charitable giving approaches creates a difference of $15,600 in total claimed deductions over the same hypothetical three-year period.

If you are on the threshold between taking the standard deduction or itemizing to maximize your tax benefits, charitable bunching is worth evaluating in detail.

This hypothetical example is only for illustrative purposes. Haven Wealth Planning does not provide tax or legal advice. Please consult your qualified legal or tax professional about your specific facts and circumstances.

Donor Advised Fund

A donor advised fund is a tax-advantaged account – like a 401(k) is for retirement savings – with a specific, intended purpose.

Tax-advantaged means the tax code provides a benefit to the investment or account holder by making the investment or account exempt from taxation, deferred from taxation, or bear a reduced tax to the taxpayer.

A donor advised fund, or DAF, is a charitable investment account you can establish to support public qualified charitable organization(s). A DAF also allows you to take an immediate charitable deduction in the year of your contribution.

At the technical level, a donor advised fund is a separately identified fund or account maintained and operated by a section 501(c)(3) organization and is considered a public qualified charity. In this context, the public qualified charity is called a sponsoring organization.

Each donor advised fund account is composed of contributions made by an individual donor or joint donors.

Donor Advised Fund: Contributions

Once you make a donor advised fund contribution, that contribution is irrevocable. The qualified charity has a high degree of legal control over those assets.

However, donor advised fund donor(s) retain advisory privileges with respect to the following:

- distribution of funds

- the investment of assets in the account.

Therefore, as a DAF donor you retain some rights to recommend which qualified charities receive grants and the specific grant amounts.

While this depends on your personal situation, if you have highly appreciated securities, donating them could provide you with a greater tax savings in a given year than donating cash directly to a charity.

Contributing Appreciated Assets

Donor advised fund donors can directly contribute publicly traded securities. This approach is particularly tax-efficient for securities that have been held for more than one year. This type of security can be donated at its fair market value and does not subject the donor to capital gains tax.

Adjusted Gross Income (AGI) Limits on Deductions

Your deduction for charitable contributions generally can’t be more than 60% of your AGI. In some cases, 20%, 30%, or 50% limits may apply. Two of the more relevant and applicable deduction limits to consider are the following:

- If you donate cash, via a check, wire transfer or credit card, you’re generally eligible for an income tax deduction up to 60% of your AGI.

- If you donate long-term appreciated assets directly to charity or to a donor advised fund, you generally won’t have to pay capital gains. As such, you generally can take an income tax deduction in the amount of the full fair-market value, up to 30% of your AGI.

Carryovers

If your charitable donations exceed your AGI-based deduction limits in a taxable year, generally you can carryover the excess deductions for up to five years. There are certain situations such as qualified conservation contributions that can be carried over longer than five years.

You could then apply the excess deductions against your AGI in a future tax year.

You’ll want to work with your qualified tax professional to understand your personal situation and how the carryover rules apply.

The goal of this particular article is to raise your awareness of these rules so you can be more informed.

Documentation Fundamentals

Since 2006, when you establish a donor advised fund, you want to receive a written, contemporaneous acknowledgment from the DAF. In this context, a contemporaneous acknowledgment needs to meet:

- received on or before the earlier of the date on you file a tax return for the tax year in which the contribution was made or

- the due date (including extensions) for the return.

The IRS requires the written “acknowledgment required to substantiate a charitable contribution of $250 or more must contain the following information:

- name of the organization;

- amount of cash contribution;

- description (but not value) of non-cash contribution;

- statement that no goods or services were provided by the organization, if that is the case;

- description and good faith estimate of the value of goods or services, if any, that organization provided in return for the contribution; and

- statement that goods or services, if any, that the organization provided in return for the contribution consisted entirely of intangible religious benefits, if that was the case.

When you contribute cash, securities, or other assets to a donor-advised fund at a public charity, like, you are generally eligible to take an immediate tax deduction. Then those funds can be invested for tax-free growth, and you can recommend grants to any eligible IRS-qualified public charity.”

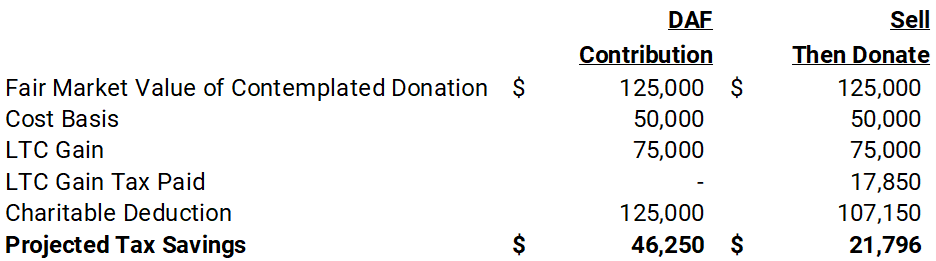

Hypothetical Illustrative Example: DAF Contribution vs. Post-Sale Cash Contribution

If a donor were to liquidate an asset and later donate the proceeds to their DAF, the amount would be reduced by capital gains tax, potentially leaving less money available to grant to a qualified charity.

Key Facts and Assumptions

- Contemplated Donation: is the fair market value of appreciated securities that have been owned more than one year.

- Cost basis: is the amount of money you have invested in an individual security.

- Realized Long-Term Capital Gain: The proceeds from the sale of a security less the cost basis.

Continuing this logic, if in 2024 you contributed to your donor advised fund the following:

- a security with a fair market value of $125,000

- with a cost basis of $50,000

- with long-term capital gain of $75,000

- your AGI is $675,000

- your Federal Marginal Tax Rate is 37%

- your LTC Gain Rate is 20% and Medicare Surtax is 3.8%

- you could potentially take a tax deduction for the full $125,000 in the tax year you contributed the security to your DAF; and

- you itemized your contributions.

Any calculations are intended to be illustrative and do not reflect all the potential complexities of individual tax returns.

The Projected Tax Savings reflects the federal income tax deduction less any long-term capital gains tax paid. The Projected Tax Savings does not account for any state and local taxes, alternative minimum tax (AMT), or limitations to itemized deductions.

Your Estate Plan and Donor Advised Funds

If you have philanthropic goals during or after your lifetime, a donor advised fund can support your vision and strategy for causes and organizations that matter to you, your family, and your community.

A donor advised fund also provides you with the choice of how your contributions are recorded and what personal information you want to share during the grant process.

If you’re considering gifting appreciated assets in a later season of life, you might want to reconsider transferring those assets via an inheritance instead. This could allow the recipient, or heir, of those assets to receive a step-up in basis to the fair market value at the time of your death, if you are the original holder.

A step-up in basis in this context is a tax rule that adjusts the value of inherited property to its fair market value at the time of the original owner’s death. This reduces the capital gains tax liability to the heir if they sell the property later. A step-up in basis applies to inherited assets such as stocks, real estate, and personal property.

And so, gifting an appreciated an asset during your lifetime does not allow this to happen.

Benefits/Considerations of Donor Advised Funds

- An immediate income tax deduction

- Avoidance of capital gains taxes if the gift is appreciated property

- The charitable assets have the potential for continued growth over time

- Reduction of the gross estate by the amount of the excluded asset

- Support multiple charitable goals through a single tax event

Drawbacks/Considerations of Donor Advised Funds

- Using assets or appreciated securities needed for your retirement or education funding goals

- Irrevocable contributions.

- Continued management of the DAF account and related portfolio

- Itemize deductions to capture

- DAF account management fees increase expenses (should be around ~1%/year or less)

In Practice: DAFs and Bunching Potentially Reduce Tax Burden in a Windfall Year

Depending on your specific facts and circumstances, DAFs and Bunching could potentially reduce your tax burden after you experience a financial windfall.

Windfalls from infrequent or one-time events such as receiving an inheritance, selling a business, or experiencing uncharacteristically strong market returns.

The windfall could allow you to effectively pre-fund years of planned giving with assets from a single high-income event.

The Next Step

When you set philanthropic goals, automate your saving for them, and create a plan designed for your specific situation you’ll be more likely to achieve your goals. Your philanthropy can foster a deeper connection with your family and loved ones. You can instill and reinforce important virtues with your charitable planning and actions.

As a thoughtful steward of your family’s resources, finding ways to maximize the positive impact of your charitable efforts is both diligent and practical. When you align your wealth with your thoughtful, generous spirit, you can give your money meaning.

The feeling of “enough” can be a calming force, especially in the context of your financial plan.

Use this educational overview of charitable bunching and donor advised funds to be more informed and prepared for your own philanthropy goals. Charitable giving, like so many other topics in financial planning, intersects with the world of tax, please make sure you coordinate with a qualified tax professional.

Frequently, proactive and open collaboration with your tax and estate planning professionals can help you work towards your financial planning goals. Working with a financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

Who is providing you with the right kind of accountability and collaboration in your personal financial life?

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.