Now is a good time to create your home inventory; to review and catalogue your personal property. Explore how the loss settlement provisions of your homeowners insurance policy can play a significant role if you were to experience a disaster. This educational overview can help you to be more informed and prepared should you experience a loss of your personal property.

Learning Points

First, A Bit of Context

There have been multiple outbreaks of severe storms and tornados this year across the Midwest. In and around the Saint Louis, Missouri metropolitan area, there have been nearly a dozen confirmed tornadoes since the start of Missouri’s tornado season.[i],[ii]

These events, as well as a nearby house fire over the holidays, inspired and highlighted the relevancy of the following post about creating a home inventory.

Like clean water and modern electricity, it can be easy to take your everyday possessions for granted. While most of us assume our possessions will always be there from one day to the next, we guard against risk and disaster by insuring our possessions, like our homes, vehicles, and personal property.

The Importance of Your Home Inventory

When you pay for the right insurance coverage to mitigate significant risks in your life, you’re oftentimes protecting your loved ones and possessions. Disasters such as fires, floods, and tornados can ruin your possessions and leave you with the stressful task of trying to remember everything you used to own.

A comprehensive home inventory can save you time and alleviate stress in the aftermath of a disaster. Your home inventory can also help you and your family establish the fair and objectively correct value of any lost or destroyed possessions inside and outside your home.

To help you get started with your own home inventory, this educational post outlines what information to consider adding to your home inventory for insurance purposes. If you experience a significant loss of your personal property, your insurance company is likely to request that you provide them with an inventory of damaged or stolen property as part of the claims process.

But first, you’ll want to understand how a few key insurance concepts relate to your personal property and loss.

What is Personal Property

For most homeowners, the quickest way to think of your personal property is all the contents of your home (and beyond) that are not actually a part of the dwelling structure.

In the context of your insured personal property, there are three main categories:

- Fully covered items (up to your policy limit).

- Partially covered, specialty items (category-level limits).

- Excluded / non-covered items.

To determine what is and is not covered by your insurance – and for how much it is covered – review your homeowners insurance policy and related declarations.

Generally, fully covered personal property includes items like furniture, clothing, appliances, personal electronics, tools, home décor, and sporting goods for example.

Other valuables like jewelry, firearms, silverware, artwork, cash, and collectibles often have special and varying coverage sub-limits.

Your policy declarations detail how much loss is covered for one item, as well as the aggregate limit for each loss event. Your policy documents will also detail how much your deductible is for general personal property coverage.

Your personal property is often protected outside the home. Your homeowners insurance policy might even use the phrase “while it is anywhere in the world” to describe the type of coverage used for your personal property.

As an example, if you had some of your personal belongings inside your car that were stolen, chances are your personal property insurance covers it. However, if you rent a storage unit for your personal property, be sure to explore how much coverage your current policy provides.

For the third main type of personal property coverage, or lack thereof, these items are generally in that list:

- Pets (e.g. animals, birds, and fish).

- Motorized vehicles and watercraft (there are sometimes low, special limits of liability on certain types of these items).

- Business property (again, with certain lower limits depending on the nature of the property).

- Property owned by a tenant in your home not related to you.

Now that you understand the distinction between covered, partially covered, and excluded items, let’s dive a little deeper into personal property items with specialty limits, and address how to get your specialty items fully insured.

Scheduled Personal Property Coverage

If you have specialty personal property whose value, or collective value, exceeds your current policy’s sub-limits, then consider obtaining additional coverage by scheduling out your personal property on your homeowners policy.

To do this, your insurance company will request you to obtain an appraisal for each of the items you wish to schedule. The specific process will vary depending on where you live and your insurance company.

The benefit of this approach is that you’ll know exactly how much your item(s) are worth and insured for through your homeowner’s policy. This can be a cost-effective choice for a handful of items, like an engagement ring, a watch or heirloom jewelry.

Remember to revisit this topic if you get a new piece of jewelry that would exceed your base policy sub-limits. This highlights one downside to this approach; you have to vigilantly maintain your scheduled personal property list with your insurance company.

Alternatively, you could choose to cover your personal property items through a Personal Articles Floater. This is a separate policy for your personal property items, and you’ll want to research the related limits and provisions of this policy to determine whether it’s the right approach for you and your family.

This separate policy can allow you to avoid expensive claims on your homeowner’s insurance for personal property items. On the other, it’s a separate policy that you’ll need to maintain and pay for each year for the coverage. You’ll also need to consider whether the added hassle of coordinating reimbursement between two policies – a homeowners and separate personal articles floater – is beneficial to you and your family.

With this expanded understanding of personal property, let’s explore actual cash value and replacement cost value in the context of your personal property. If you experience a significant loss of personal property, these terms matter.

Loss Settlement: Actual Cash Value vs. Replacement Cost Value

As a homeowner, it’s important to familiarize yourself with two loss settlement methods used to describe how an insurance company will reimburse you for personal property losses: actual cash value and replacement cost value.

- Actual Cash Value (ACV) refers to the current value of your personal property, considering things like the item’s age, general wear and tear, and resulting depreciation. As such, this method will generally be a lower amount as compared to the cost of a brand-new item. This method does not consider qualitative factors such as how little used or well-kept your personal property was prior to the loss.

- Replacement Cost Value (RC) refers to how much it costs to repair or replace the lost personal property with an exact or functionally similar, but new, item.

A practical consideration: understand which loss settlement method applies to and for which category of personal property in your homeowners insurance policy.

In a scenario where you are reviewing your homeowners policy with a replacement cost provision, you might get to the section where the policy starts looking like an “if…then…” math problem.

That’s the heart of the matter on this topic.

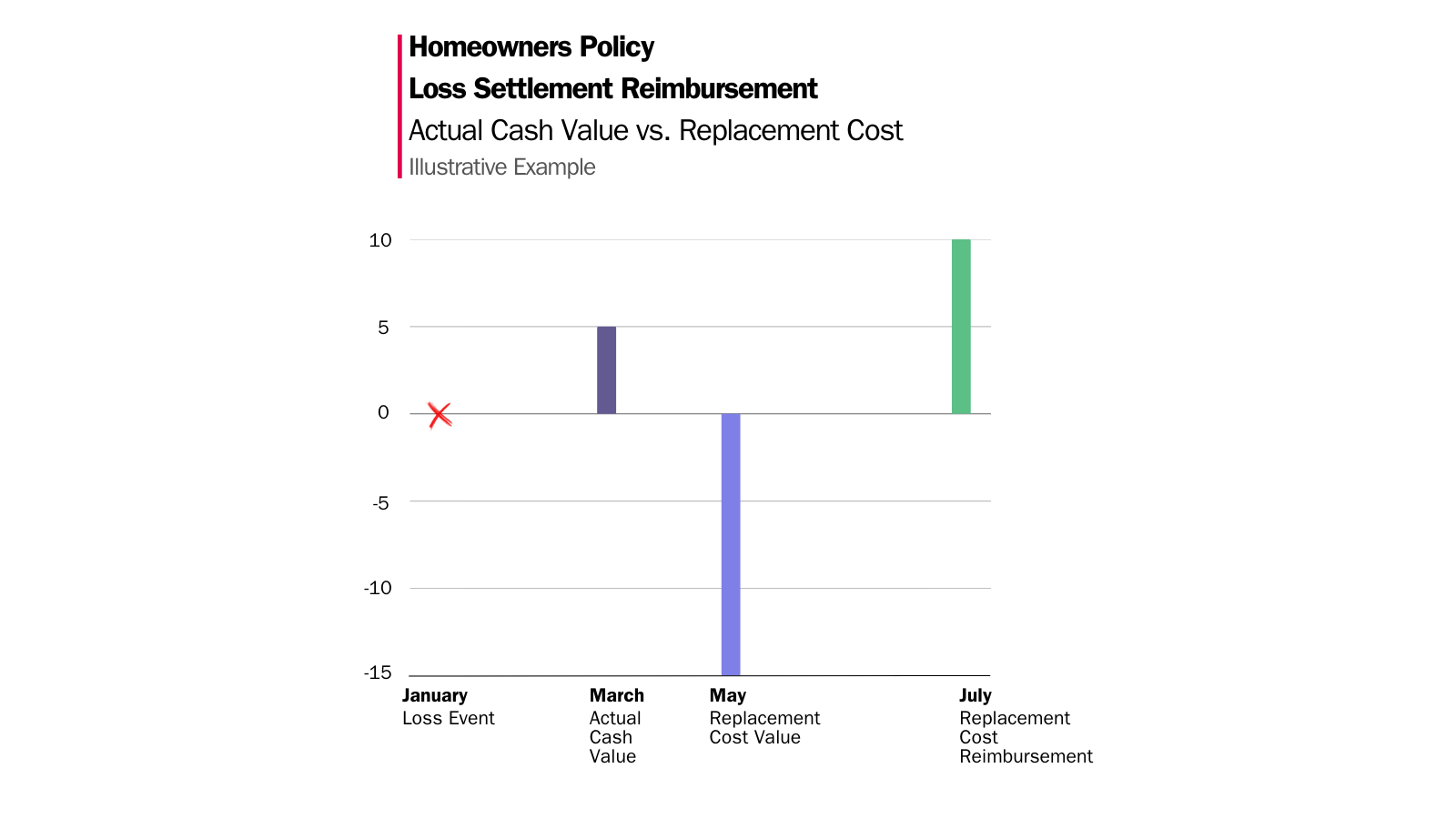

Specifically, your replacement cost loss settlement provision will likely reimburse you in a two-step process:

- First, you are reimbursed for the actual cash value of the lost or damaged personal property.

- Second, after you repair or replace the damaged item, you’ll be reimbursed for the difference between the actual cash value and the cost you actually and necessarily spent to repair or replace the item.

- If you don’t repair or replace the property within two years after the date of the loss, you’ll only recover the actual cash value of the property.

The illustrative example below shows a hypothetical loss reimbursement process using the two-step process above.

Specifically, if the personal property’s replacement cost value is worth 15, and the actual cash value of the item is 5 (See Step 1 above), the replacement cost reimbursement would be equal to 10 (See Step 2 above). 5 + 10 = 15. Of note, this example does not contemplate how a deductible would reduce your recovery.

Illustrative Example of Loss Settlement Reimbursement

Three key learning points:

- If you choose not to repair or replace the damaged item, you do not get to proceed to step 2 above with the insurance company.

- If you repair or replace the damaged item within two years, you will need to have the cash on hand or credit available to pay for the full amount of the item outright and seek reimbursement for the difference between the ACV and the actual replacement cost from your insurance company.

- If you repair or replace the damaged item, or seek reimbursement, after more than two years (the timing may differ for your specific policy – you will not be reimbursed.

And so, if you experience a significant loss of covered personal property, and you don’t have strong documentation for expensive-to-replace items, you are at risk of not recovering the full value of the lost property.

The next step: Review your policy in detail and consult with the insurance company or broker for specific coverage details and any limitations or exclusions to your loss settlement options.

Creating Your Home Inventory

Now that you have a foundational knowledge about how your insurance company views personal property, it’s time to create your home inventory.

To start, decide where you’re going to store your home inventory. If you’re going to maintain a physical home inventory, the biggest question is where you’re going to physically store (and backup) all of that information.

If you’re going to store your home inventory digitally, consider whether you want this information accessible to the internet or if you want it on an encrypted drive/device.

Now that you’ve decided where you’re storing your home inventory, it’s time to get organized.

Home Inventory Data Points

Consider gathering the following data points in your home inventory:

- Item Name

- Serial Number

- Make/Model Number

- Date of purchase

- Bills/Receipts/Related documentation

- Appraisals or estimated value

- Photos

- Video

From a risk perspective, you could start by inventorying your home’s highest value items. Items like furniture, appliances, electronics/devices, clothing/shoes (e.g. your designer jean collection), jewelry, specialty tools, and other valuables. The key is keeping it organized in a way that works for you.

Keep your inventory up-to-date by adding or removing items as necessary.

Photographs and Videos

Photograph your personal property individually, rather than in groups or as it’s stored in a closet, drawer, or safe. You’ll want your photos and videos to show the detail and quantity of your property.

Even if you’re not the next Ansel Adams, be sure to have photos of key items from multiple angles.

However, if you have custom storage solutions for specific items, showing the manner in which they are stored could also help during your claims process. It can demonstrate the care in which the item(s) were stored and maintained.

Video your personal property, especially items with unique or expensive qualities. This can help you later during the claims process.

All of this is designed to create a visual record of the condition and value of your possessions.

Consider taking new photos or videos of your possessions to document their condition and any improvements or upgrades.

The Next Step

Start by covering the basics: snap photos and videos, save receipts and appraisals, and remember items beyond your home. You don’t have to do it all at once. Break up the project into mini tasks. Once you’ve documented your most expensive/important items, consider going room by room over the course of a year.

Keep your inventory secure and relatively up to date. This ensures you have a detailed record of your belongings, easing the claims process later should you get to that point.

Your thorough preparation can help protect your family from the risks of high impact events, even if they are relatively rare. A complete home inventory is one, albeit simple, way to stay prepared.

When you spend the time creating your home inventory, you can give yourself and your spouse peace of mind.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

References

[i] Source: https://www.ksdk.com/article/weather/severe-weather/st-louis-tornadoes-confirmed-touchdown-thursday-storms-missouri/63-398d00cf-63a8-4d20-a25e-a58018127270