Qualified Charitable Distributions (QCDs) provide a tax planning opportunity to investors who have charitable giving goals. Explore the details and practical considerations of QCDs in this educational overview. Read on to be more informed and prepared in your own philanthropy, or that of older family members.

Learning Points

Explore Qualified Charitable Distributions

A qualified charitable distribution (QCD) sent directly from your Individual Retirement Account (IRA) to a qualified charity can be a tax-effective way for you to give without affecting your taxable income later in life.

Traditional IRA distributions, ones that are made with pre-tax dollars, are taxed as ordinary income. Qualified charitable distributions potentially allow you to exclude the distribution from your income.

Below are key details about QCDs to help you consider whether this charitable giving strategy aligns with your personal situation and giving goals.

Because topics like charitable giving, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with a qualified tax professional.

Qualified Charitable Distribution: Eligibility and Mechanics

Age Eligibility: You can perform a qualified charitable distribution if you are 70½ or older when the QCD is made.

Required Minimum Distributions (RMDs): If you or a loved one must take RMDs, QCDs count toward an individual’s RMD.

For example, if your required minimum distribution for the year is $7,000, and you make a $4,000 qualified charitable distribution, you would only need an RMD of $3,000. The $4,000 QCD is excluded from your income, and the $3,000 RMD would be included in your taxable income.

Standard or Itemized Deductions: Unlike other some other charitable giving strategies, a qualified charitable distribution allows you to itemize your deductions or take the standard deduction.

Direct Transfer: The qualified charitable distribution must be a trustee-to-trustee transfer. Meaning, a QCD must be a direct transfer from the IRA to the qualified public charity. It isn’t a QCD if you deposit the distribution in your bank account and later donate it.

Practical Consideration: The qualified public charity you are directly distributing your QCD to must be eligible to receive tax-deductible charitable distributions.

Distribution Limit: In 2024, the annual maximum QCD is $105,000, across all IRAs. Like other IRA limits, this is a per taxpayer limit. This figure adjusts annually by a set inflation factor.

Since a QCD must come from an IRA, which is an inherently individual account, a couple that files a joint return could potentially coordinate their QCDs to maximize their charitable efforts. It’s important that your QCD does not conflict with your other financial goals, like retirement.

Distribution Source: For your IRA distribution to qualify as a QCD, it must come from deductible contributions and earnings. Meaning, if you took a regular IRA distribution, it would have been characterized as taxable income to you.

- If an IRA includes deductible and non-deductible contributions, the QCD comes from deductible funds first, and then from any non-deductible IRA contributions. This allows for a larger amount of your non-deductible (read: non-taxable) funds to remain in your IRA for later distributions.

Eligible IRA Types: Traditional IRAs, rollover IRAs, inherited IRAs as well as inactive SEP-IRAs and inactive SIMPLE-IRAs are potential candidates.

A Roth IRA, funded by after tax dollars, would not provide as much of a benefit for QCDs relative to a traditional IRA.

Ineligible IRA Types: QCDs cannot be made from ongoing / active employer-sponsored IRAs like:

- SEP-IRAs

- SIMPLE-IRAs

For clarity, QCDs cannot be made from defined contribution retirement plans, such as:

- 401(k) accounts

- 403(b) accounts

Timing/Deadlines: A QCD needs to be completed by December 31 of the taxable year in which you want it to apply.

Mixing IRA contributions and QCDs: In 2024, the amount of QCDs that you can exclude from income is reduced by the following:

- The excess of the aggregate amount of IRA contributions you deducted for the taxable year, and any prior year that you were age 70½ or older, over the amount of those IRA contributions that were used to reduce the excludable amount of QCDs in all earlier years.

- Practical perspective: consider whether making Roth IRA contributions in the years leading up to and including a QCD provides you with a more tax efficient approach to your charitable giving.

- Coordinating your income and tax planning around IRA contributions and distributions, including QCDs, with your spouse and their IRA(s) can provide you with thoughtful tax planning opportunities.

IRA Overview

If you are investing money in your traditional IRA or a Roth IRA, it’s important to remember are tax-advantaged accounts that certain individuals or married couples can establish to accumulate funds for retirement.

Contributions to traditional IRAs can be tax deductible, but withdrawals are included in taxable income.

Roth IRA contributions are not tax deductible, but withdrawals are generally tax free.

IRA Distributions Fully or Partly Taxable

Distributions from your traditional IRA may be fully or partly taxable, depending on whether your IRA includes any non-deductible contributions.

- Fully taxable: If you only made deductible contributions to your traditional IRA, then you have no basis in your IRA. Because you have no basis in your IRA, any distributions are fully taxable when received.

- Partly taxable: If you made non-deductible contributions, or you rolled over any after-tax amounts to any of your traditional IRAs, you have basis. That basis, also called cost basis, is equal to the amount of your contributions.

These non-deductible contributions aren’t taxed when they are distributed to you. They are a return of your investment in your IRA. Until all your basis has been distributed, each distribution is partly nontaxable and partly taxable.

Additional Charitable Giving Considerations with QCDs

While there is a $105,000 maximum QCD in 2024, the amount you contribute to charity via a QCD doesn’t apply to your overall charitable deduction limit.

Specifically, you cannot claim a charitable deduction for any QCDs since the distribution of income is excluded from your adjusted gross income. As such, your QCD is excluded from calculating your taxable Social Security income and Medicare IRMAA surcharges, among other things.

And so, if your charitable giving goals exceed the QCD limit, you could explore other tax-efficient ways to give, like charitable bunching cash or appreciated securities, or funding a donor advised fund.

Of note, you cannot make a QCD to a donor advised fund.

As an alternative to completing a QCD, evaluate whether taking your required minimum distribution (RMD) and gifting appreciated securities directly to charity in lieu of completing a QCD is more beneficial in any given taxable year. A key consideration in that scenario is determining your long-term capital gains in an appreciated security.

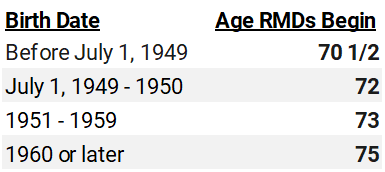

Depending on your date of birth, an IRA owner must begin taking annual withdrawals from traditional IRAs – called required minimum distributions (RMDs) – based on the following table:

Documentation Fundamentals

Even though qualified charitable distributions are not deductible as charitable contributions, you still need the correct documentation for your tax records.

Just like itemized deductible contributions, such as donor advised funds, if you complete a QCD, you need to receive a written acknowledgement of your contribution from the charitable organization before filing their return.

This requirement has been in place since the Pension Protection Act of 2006.

Specifically, you want to receive a written, contemporaneous acknowledgment from the charity. A contemporaneous acknowledgment needs to meet the following requirements:

- received on or before the earlier of the date on you file a tax return for the tax year in which the contribution was made or

- the due date (including extensions) for the return.

The written acknowledgment should include the following information:

- name of the organization

- amount of cash contribution

- description (but not value) of non-cash contribution

- statement that no goods or services were provided by the organization, if that is the case

- description and good faith estimate of the value of goods or services, if any, that organization provided in return for the contribution; and

- statement that goods or services, if any, that the organization provided in return for the contribution consisted entirely of intangible religious benefits, if that was the case.

Source: Internal Revenue Service https://www.irs.gov/charities-non-profits/charitable-organizations/charitable-contributions-written-acknowledgments

Tax Form Awareness

As you consider your charitable giving goals, and nuanced planning topics like QCDs that intersect with the world of tax, please make sure you coordinate with a qualified tax professional.

From a practical perspective, to connect the dots from charitable giving to the tax return itself, here are couple of quick educational takeaways:

- Generally, there are a few tax forms that you should be aware of in a year with a QCD; Form 1099-R, Form 1040, and Form 8606. Every tax situation is different.

- An IRA owner should have reported their Qualified Charitable Distribution(s) on their federal income tax return.

- In the early part of the year, after a completed QCD, the IRA owner will receive a Form 1099-R from the custodian, sometimes called the trustee, of their IRA.

- In Form 1099-R, Box 1 details the total IRA distributions made during that calendar year. That gross distribution figure would include both regular distributions and QCDs. To be clear, QCDs are not broken out here. You’ll need to track QCDs separately.

QCDs are included on Line 4a of Form 1040 or Form 1040-SR, and specifically:

- Total IRA Distributions = QCDs + regular distributions (line 4a)

- Total IRA Distributions less QCDs = Regular distributions (line 4b / taxable portion)

- Coordinate with your qualified tax professional and note “QCD” next to ‘taxable amount’ on line 4b.

You might also need to coordinate filing a Form 8606, Nondeductible IRAs, with your qualified tax professional if:

- you made the qualified charitable distribution from a traditional IRA in which you had basis and you received a distribution from the IRA during the same year (other than the qualified charitable distribution)

- the qualified charitable distribution was made from a Roth IRA.

- if you receive a distribution from a traditional IRA and have ever made non-deductible contributions or rolled over after-tax amounts to any of your traditional IRAs.

- This form helps you determine your nontaxable IRA distributions and your total IRA basis.

The Next Step

When you set philanthropic goals, automate your saving for them, and create a plan designed for your specific situation you’ll be more likely to achieve your goals. Your philanthropy can foster a deeper connection with your family and loved ones. You can instill and reinforce important virtues with your charitable planning and actions.

As you consider your charitable giving goals, and nuanced planning topics like QCDs, that intersect with the world of tax, please make sure you coordinate with a qualified tax professional.

Use this educational overview on qualified charitable distributions to be more informed about retirement and philanthropic planning. Whether it’s your own planning, or that of a close family member.

As a thoughtful steward of your family’s resources, finding ways to maximize the positive impact of your charitable efforts is both diligent and practical. When you align your wealth with your thoughtful, generous spirit, you can give your money meaning.

The feeling of “enough” can be a calming force, especially in the context of your financial plan.

Frequently, proactive and open collaboration with your tax and estate planning professionals can help you work towards your financial planning goals. Working with a financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.