Whether you’ve been investing for 1 year or 50+ years, you can set up simple ways to automate your savings. Explore practical considerations that align with your “why”. Feel more confident in completing the routine items on your financial “To-Do” list.

Learning Points

Automate Your Savings: Knowing Your Why

When you know who and what are truly important to you in life, you can create incredible clarity about your spending and saving.

Clarity to confidently spend on the things that matter, and confidently decline to spend on things that aren’t aligned with what you want in life.

Whether you are in your 20s, 30s, 40s, or 50s, you can implement simple ways to automate your savings. You’ll spend less time blocking and tackling these foundational elements of your financial life.

Start feeling more confident that routine items on your financial “To-Do” list are happening. Refocus your time on aligning the more involved elements of your financial life with your goals and values.

For instance, review your account beneficiaries or reaffirm that you’ve correctly titled your assets and accounts.

Aligning Your Savings Vehicle + Priority + Time Horizon

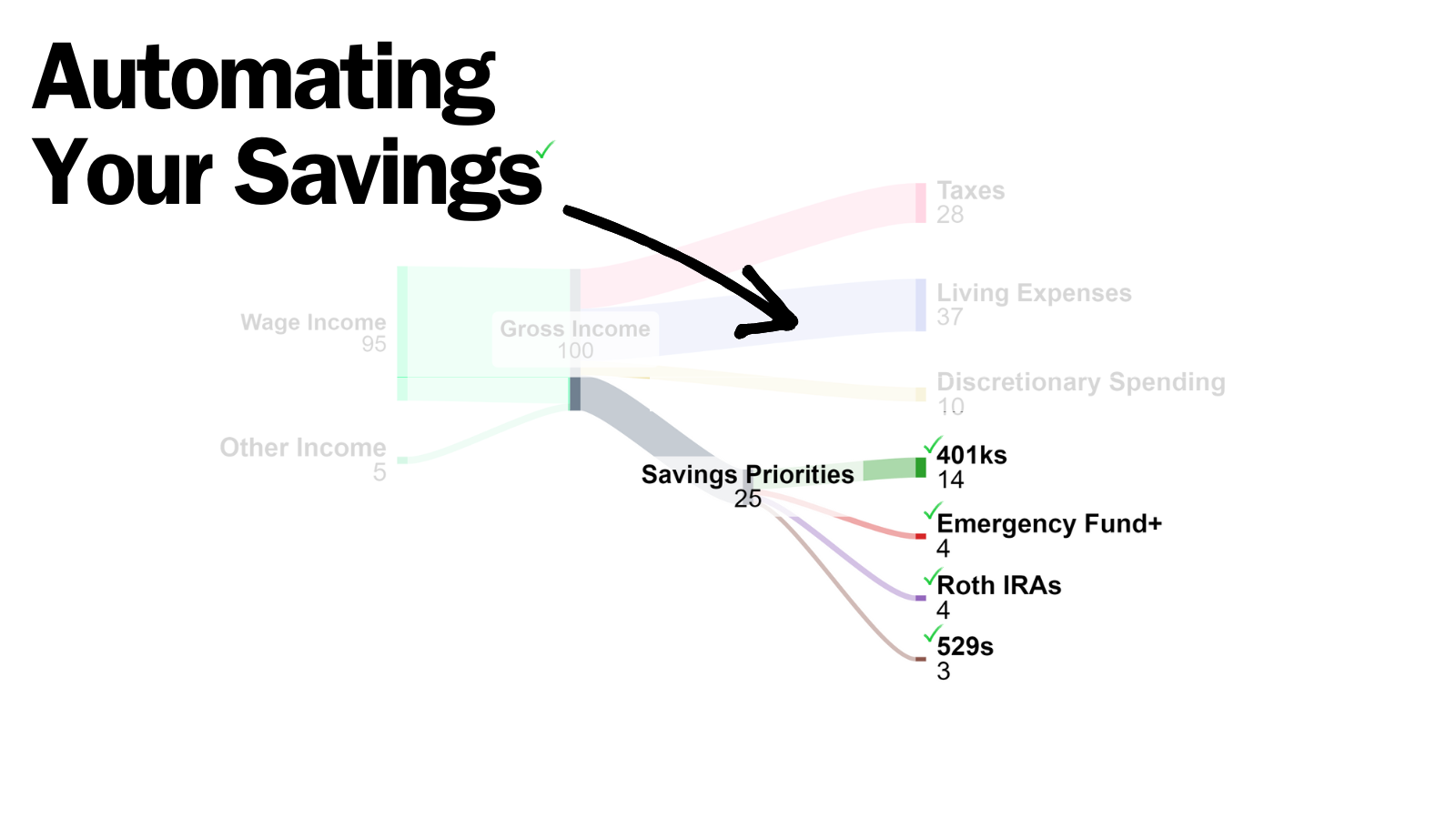

When you know your “why”, you can focus ways to achieve it. If you are looking to automate your savings, take the time to align your savings with your goals and values.

Thoughtful investors like you can align a handful of investment planning elements into a single, personalized solution:

- What you are saving for.

- How much you need to save.

- What account you use.

While there is no one-size-fits-all solution to investing and saving, consider these concepts in the context of your personal situation and goals:

- Time horizon: When do you plan to spend the money? For example, if your savings priority is your emergency fund, it’ll have a shorter time horizon than if your saving priority is your planned retirement in 20 years. Generally, you’ll want your shorter time horizon savings priorities to be invested in more cash, or cash-like investments.

- Liquidity: how quickly will you need to have your cash readily available, without having to sell the asset at a discount? Less liquid assets are often better paired with longer-term investment horizons.

- Risk-capacity and risk-tolerance: these concepts relate to how much you invest and how well you can sleep at night without undue anxiety around your investments. This is where you really start to feel and experience personalizing your savings and investing. Creating a solution that works for you and your family is what matters. Your risk capacity is your financial ability to absorb losses. Your risk tolerance is your emotional and psychological ability to take on, accept, and manage the uncertainty and volatility associated with risk-taking.

- Cost: investment costs erode your returns over time. Understand how much it costs to buy, own, manage, and sell your investments.

- After-tax results: Taxes matter. Preferential tax treatment in the form of long-term capital gains and qualified dividends provides an increasing benefit to investors with longer investment time horizons, than shorter ones. Holding your higher risk/return assets like equities, rather than lower risk/return assets like fixed income holdings, in taxable accounts, can create a more tax-efficient strategy.

Consider the hassle factor, too. Is it worth your time and energy to automate your saving if the expected result is immaterial to your financial life? Just because you can, doesn’t mean you should.

As you work toward your savings priorities, you can adjust your investment plan to support your “why”, even when your life changes.

Now, let’s explore simple and practical approaches to automating your saving.

Automating Your Regular Living Expenses

If one of your goals is to set aside enough money to pay your monthly living expenses, automating your finances can be relatively straightforward.

Ideally, you would need one recurring payment through a credit card or debit card to successfully pay each bill on time.

Chances are, you’ve already established recurring payments for your daily living expenses like your mortgage or rent, utilities, internet, cell phone, and credit cards. Similarly, you likely already use direct deposit with your paycheck, which is something you’ll want to do if you plan to automate any other areas of your financial life.

When you automate each of your regular, recurring payments, you can reduce some of your own mental load. You can shift your focus from “did I pay this bill?” to “do I need this service/thing/membership?”. You can also reduce the chances that you have to pay any late fees.

While you’re reviewing your household expenses, consider creating a short list of services you no longer want. This short list could include seldom used or redundant streaming services, or membership you no longer use.

Automate Your Savings: Practical Considerations

If your savings priority is for an emergency fund, an annual expense (e.g. your term life insurance premium), or a mid-range goal (e.g. a new vehicle), then you might then need to set up an external transfer to a high-yield cash account.

Here’s one approach to consider…

Banking Institution: Internal Transfers

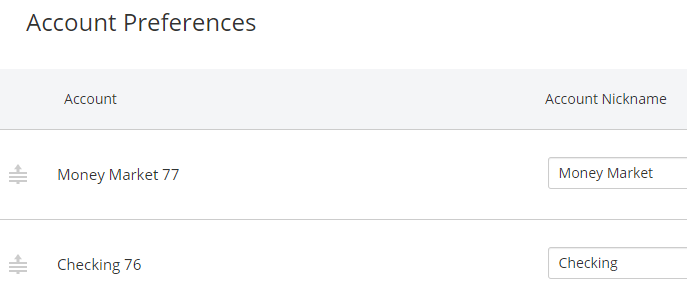

Step 1 | Establish and Rename Your Accounts: Once you create your account(s) at your bank or credit union, give that account a name that reminds you why you’re saving money in it.

Step 2 | Know when you get paid: Review your employee handbook or employment agreement to confirm your pay schedule. The goal is to ensure you have the income to transfer to your newly created accounts.

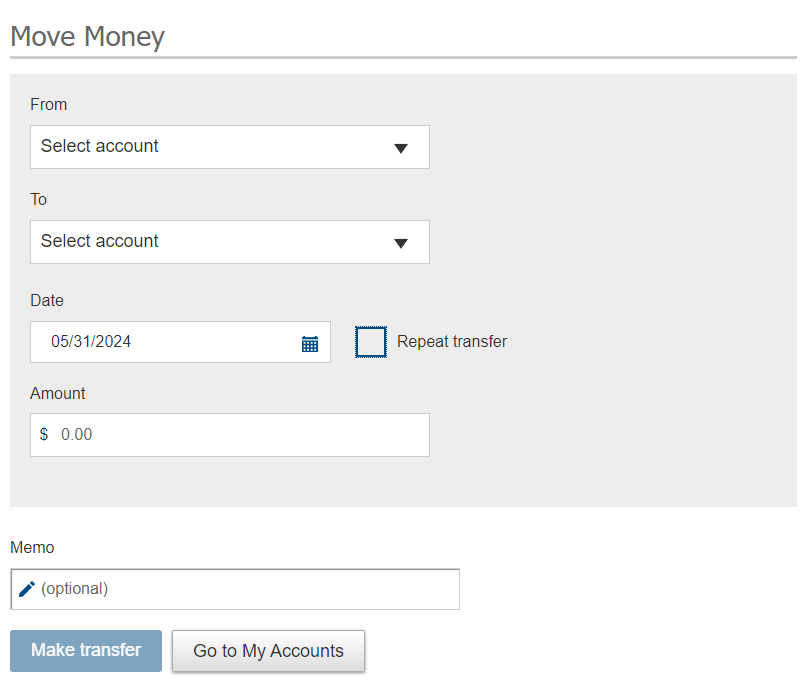

Step 3 | Create your scheduled transfer:

- From which account is your transfer going?

- Where do you want your transfer to go?

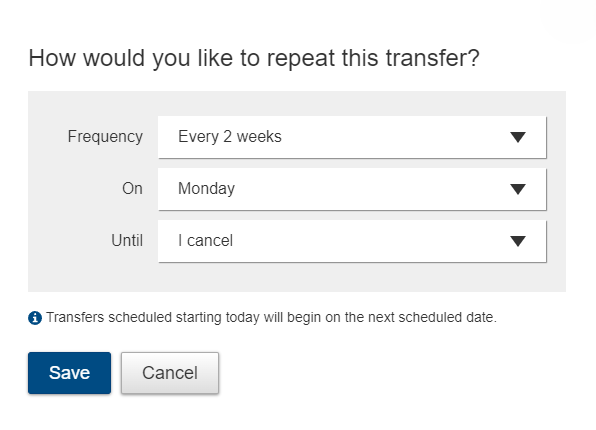

- When do you want the transfer to occur? If, for example, you get paid on the 2nd and 4th Friday of every month, you could establish a recuring transfer to occur on the following Mondays.

- How much are you transferring? When you know how much you need to save to achieve your savings or investing goal, you can break that goal down into small amounts based on the frequency of your planned transfers. Determine how much you need to save every other week or every month, for example.

A Practical Consideration: FDIC and NCUA Coverage

Review your account(s) for FDIC or NCUA coverage: As you begin to automate your savings, review your bank account balances and consider how your account titling changes FDIC or NCUA coverage. Your account’s ownership type (individual, joint, trust, etc.) is factored into the FDIC and NUCA coverage. Each ownership category has separate limits.

For your bank accounts: review your FDIC insurance coverage with the FDIC’s calculator.

For your credit union accounts: review your NCUA Share Insurance with NCUA’s estimator tool.

External Transfer Considerations

What if you want to transfer money from a bank account to invest in your traditional IRA, Roth IRA, 529 account, or taxable brokerage account? You can automate your savings for these as well.

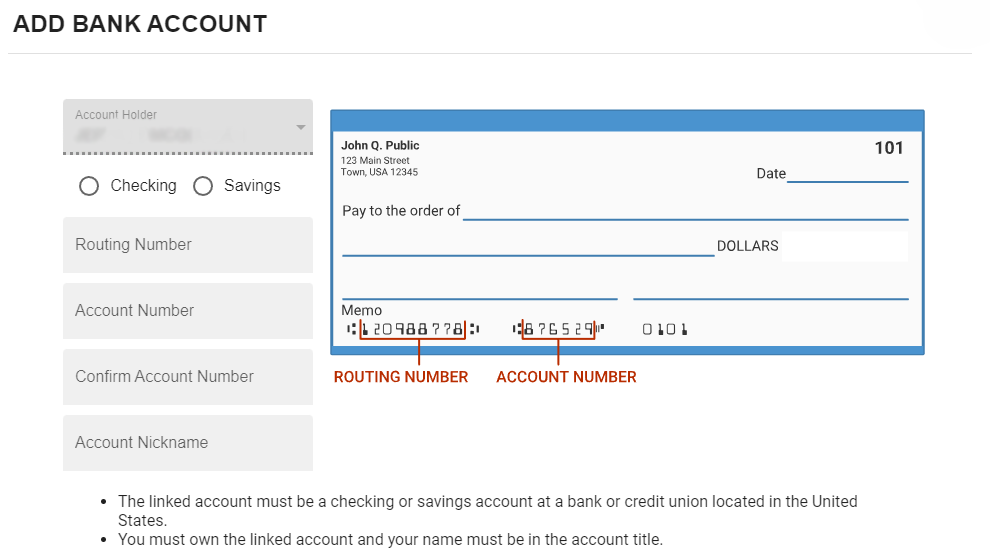

When you set up automations that pull money into your external investment account from your banking account, you’ll likely be asked to verify your ownership of the account.

The receiving investment institution will likely request that you verify your banking account ownership after you’ve provided them with the correct account and routing details.

Your investment institution might then send a couple of deposits (generally less than $0.50) to your bank account.

You’ll then need to tell the investment institution those specific deposit amounts. You’ll do this through the same account management page at your investment institution that you used to initiate the transfer.

Once you’ve established this connection, or any other automated funds transfer, you’ll want to verify it’s working as you intended.

Trust, But Verify

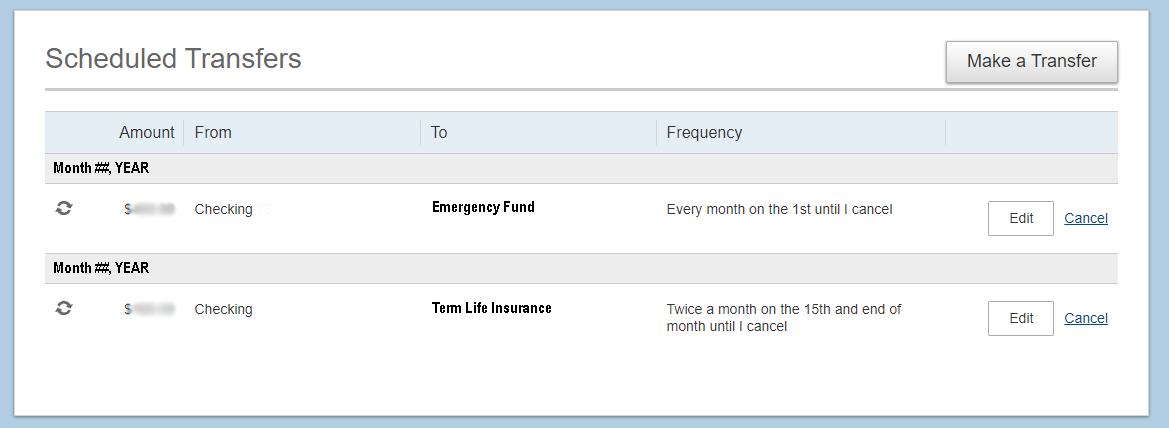

Once you’ve started to automate your savings, you’ll want to confirm that the transfers are happening.

Verify that you’re recurring/scheduled transfers are indeed established. Here’s an example of how it might look at your banking institution:

Next, set a reminder to review your transaction history so you can confirm that these scheduled transfers are occurring throughout the year.

Review and Harden Your Account Security

When you put your financial information onto the internet, even behind “secure” websites, it’s important to stay vigilant and take precautions. Today, many cybersecurity professionals have a view on security that it is not a question of “if”, but rather a question of “when” an online service gets compromised.

So, if you value your personal information remaining secure, you simply don’t want to put it on the internet.

While no service or approach is going to offer you total peace of mind, here are some approaches to consider:

Verify: Select reputable services for automating your savings, investing, and bill pay. Your financial institutions should be well equipped to provide this service directly. Before you link any of your accounts or share any personal information, verify that you’re interacting with the intended financial institution or business. What do their trust and security teams share with you to review? Spending just 5 minutes reviewing a firm’s website is better than trusting a webpage because it looks like the right company.

Enable Two-factor authentication: Creating a second check on your account access could lessen the chances of an account getting compromised. Using a third-party authentication app, with printed backup codes, can be a more efficient experience and secure than text-based two-factor authentication. Store those printed backup codes in a safe place.

Enable notifications/reporting: Set up transaction notifications or alerts for any changes or activities in financial accounts. This can help quickly identify unauthorized transactions or suspicious activities.

Regularly monitor transactions: Continuously monitor your bank and credit card statements for any unusual or unauthorized transactions.

Be on the lookout for phishing: Don’t let yourself become a victim of a phishing attempts via email, text messages, or phone calls. If somebody contacts you digitally with an urgent issue, you want to disengage immediately. Instead, contact the business or financial institution directly.

Other options to consider include only using a relatively low credit limit credit card to pay for online expenses.

The Next Step

When you know who and what are truly important, you can create incredible clarity about your spending and saving.

Clarity to confidently spend on things that matter. Clarity to avoid spending your hard-earned resources on things that aren’t aligned with what you want in life.

As your financial planner in Saint Louis, we can help you plan for the future and enjoy the present moment.

Whether you are in your 20s, 30s, 40s, or 50s, you can implement these simple ways to automate your savings. You’ll spend less time blocking and tackling foundational elements of your financial life.

Start feeling more confident that routine items on your financial “To-Do” list are happening. Refocus your time on aligning the more involved elements of your financial life with your goals and values.

When you thoughtfully execute on this approach, you can increase the likelihood of achieving your goals, setting new ones, and enjoying the present moment.

Frequently, proactive and open collaboration with your tax and estate planning professionals can help you work towards your financial planning goals. Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.