Restricted stock units have the potential to create significant wealth for you and your family. Explore this educational post to better understand the key elements of your RSUs.

Learning Points

Overview of Restricted Stock Units (RSUs)

If you have, or plan to receive, equity compensation in the form of restricted stock units (RSUs), you want to understand how it affects your investment diversification and tax planning.

Restricted stock units, like other equity compensation programs, are intended to align the interests of award recipients with those of the company’s shareholders. RSUs can attract, motivate and retain key employees.

When circumstances line up well, equity compensation can act as a significant wealth building opportunity.

Plan participants might see a variation in the name of RSUs, like restricted share unit.

When you receive equity compensation in the form of restricted stock units, there are quite a few factors to consider. With thoughtful planning, you can avoid any surprises or unnecessary complexity with your restricted stock units.

One way to view your restricted stock units is to view them as a cash bonus when they are vested. Restricted stock units, like a cash bonus, are taxed as compensation when they vest. Specifically, RSUs are considered supplemental income and are subject to a minimum federally mandated withholding rate.

After your restricted stock units vest, the underlying stock becomes your property.

Whether you want to continue to hold the stock will depend on your goals and personal financial situation. You’ll want to understand how your RSU’s can support your overall financial goals. Whether that means you diversify your investments away from your employer’s stock to achieve your financial goals or hold a specific tranche of equity for a specific purpose.

When RSUs are one of the many pieces of your financial life, it’s important that you proactively and efficiently review, monitor, and take action on your RSUs.

Because topics like restricted stock units, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with a qualified tax professional.

Read on to explore key terms, illustrative examples, as well as tax planning considerations.

Key Terms and Concepts

Your restricted stock unit agreement will have defined terms that govern how and when your RSUs vest. As RSUs continue to gain in popularity, there are a variety of ways RSU agreements can be structured to align awardee and shareholder interests.

The following is an educational overview of the key terms you’re likely to encounter as an RSU recipient:

Restricted Stock Unit: Represents shares of the common stock of a company. This represents a right to receive stock, or cash payment of equal value, once you’ve met the conditions associated with their vesting. Typically, your RSU agreement will state that one RSU represents one share of common stock.

For example, your agreement might read something like, a “Restricted Stock Unit represents the right to receive one share of common stock in accordance with the terms and subject to the conditions (including the vesting conditions) set forth in this Agreement and the Plan.”

It’s important to remember stock-settled RSU represents a contractual right that is unfunded by the company.

Participant: This is the individual recipient of the Restricted Stock Unit Award on the specified Grant Date. If you are the Participant, you likely cannot assign or transfer it prior to vesting.

Grant Date: On the grant date, RSUs are awarded as equity compensation to employees who will receive the shares of company stock only after certain conditions, detailed in a vesting schedule, are met.

Vesting Date: The date when all your RSU plan’s vesting conditions are met. This is the date your restricted stock units (RSUs) become your property. As such, you will owe income taxes on the Fair Market Value (FMV) of the underlying stock.

Fair Market Value: From your perspective as a participant in the RSU agreement, this is generally measured as the vesting date price of the company’s underlying shares.

(Equity) Adjustments: While you’re holding restricted stock units, this type of provision can adjust the number of your RSUs proportionately for any increase or decrease in the number of issued shares of the underlying equity.

For example, this provision might apply to your RSUs if there is a split, combination, exchange, consolidation, spin-off or recapitalization of the underlying equity. It might also apply to any payment of a stock dividend.

The underlying concept is that you are to be made whole as a result any of covered corporate actions.

(Dividend) Equivalents: If you have this type of provision tied to your RSUs, your RSUs will earn dividend equivalents in the form of additional RSUs.

For example, as of each dividend payment date for your firm’s common stock, your RSU account will be credited proportionately with additional RSUs.

Dividend equivalents vest on the same schedule as the related RSU. If the dividend on the common stock is paid in cash, you will be paid in cash when you receive the share of common stock underlying the RSU.

Again, the underlying concept of this provision is to make you whole because of any covered corporate action.

Fractional Shares: In lieu of your RSU plan issuing you a fraction of a share, your company might choose to pay a cash amount equal to the fair market value of that fractional share.

Voting and Other Stockholder Related Rights: It’s important to recognize whether you have any voting, or other shareholder rights, associated with your RSUs.

For example, if you don’t have a dividend/equivalents provision in your RSU agreement, you could potentially miss out on any dividends.

Section 409A Compliance: This matters if your RSU award violates Section 409A. If your RSU’s do not meet Section 409A, they may become immediately taxable to you, and you could incur an additional 20% penalty tax, as well as potential interest penalties.

In short, the RSU award could be deemed a form of “non-qualified deferred compensation” within the meaning of Section 409A of the IRS Code.

409A is a set of rules with a broad scope applicable to many compensation arrangements, including RSUs, that are not generally viewed as “deferred compensation”. The legal and tax ramifications of Section 409A are beyond the scope of this brief discussion.

There should be language in your RSU agreement that addresses this complex tax area.

Restricted stock units, like so many others in financial planning, intersect with the world of tax in a complex way, make sure you coordinate with a qualified tax professional.

Once you understand the terms and conditions of your restricted stock unit agreement, and how they apply to your personal situation, the more accurately you can plan for when your RSUs vest.

Common Types of Restricted Stock Unit Vesting Schedules

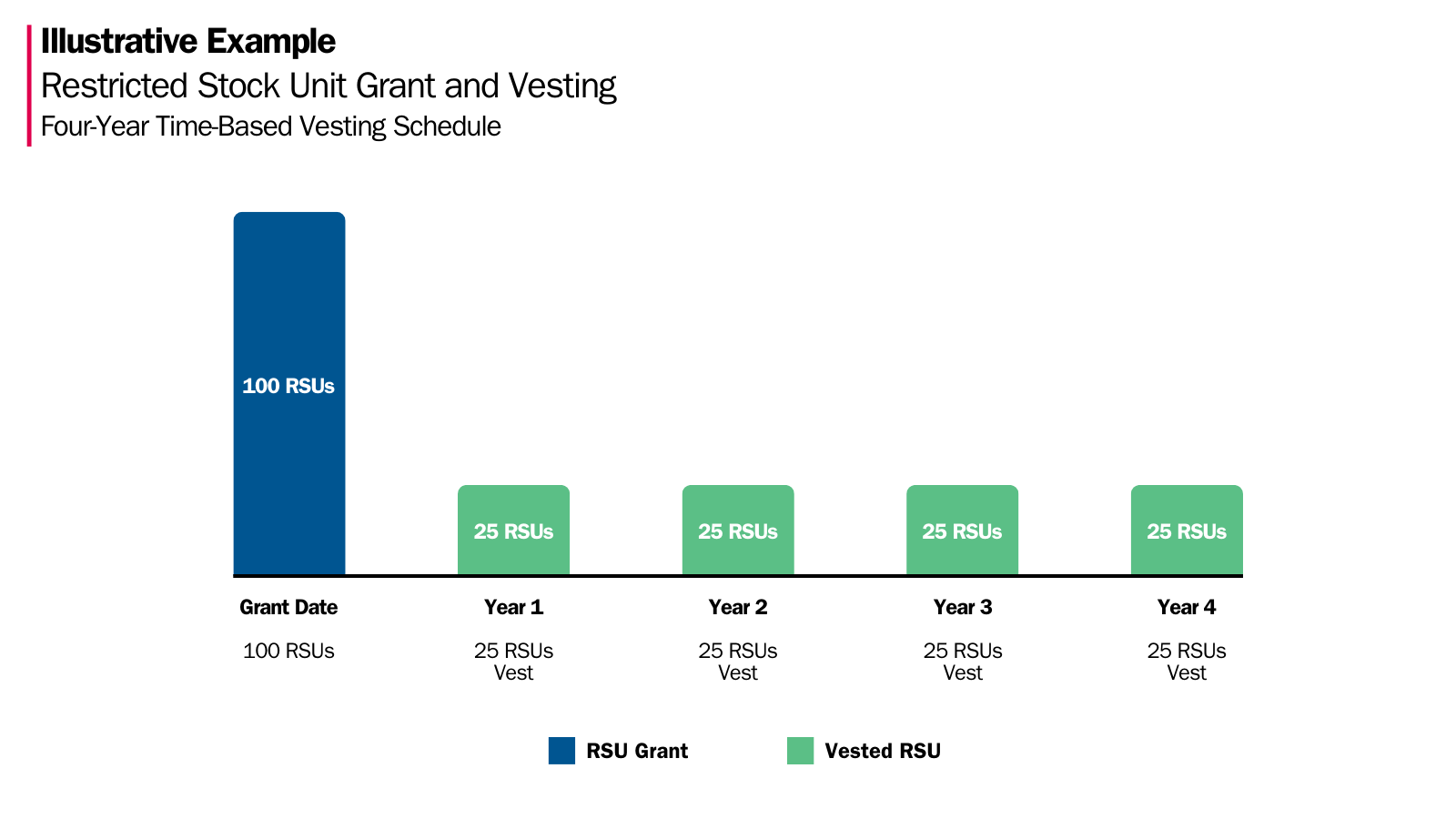

Graded/Time-based: Under this vesting schedule, you potentially receive a specific percentage of your RSUs each year on the anniversary of the grant date. Companies have some flexibility in how they choose to align management with shareholder’s interests.

For example, if you receive RSUs with a “three-year ratable vesting schedule”, those RSUs will vest 33 1/3% per year on each of the first, second, and third anniversaries of the grant date.

Or, if your RSUs “vest ratably over four years”, your annual RSUs will vest 25.0% per year on each of the first, second, third, and fourth anniversaries of the grant date. Below is an illustrative example of this vesting schedule.

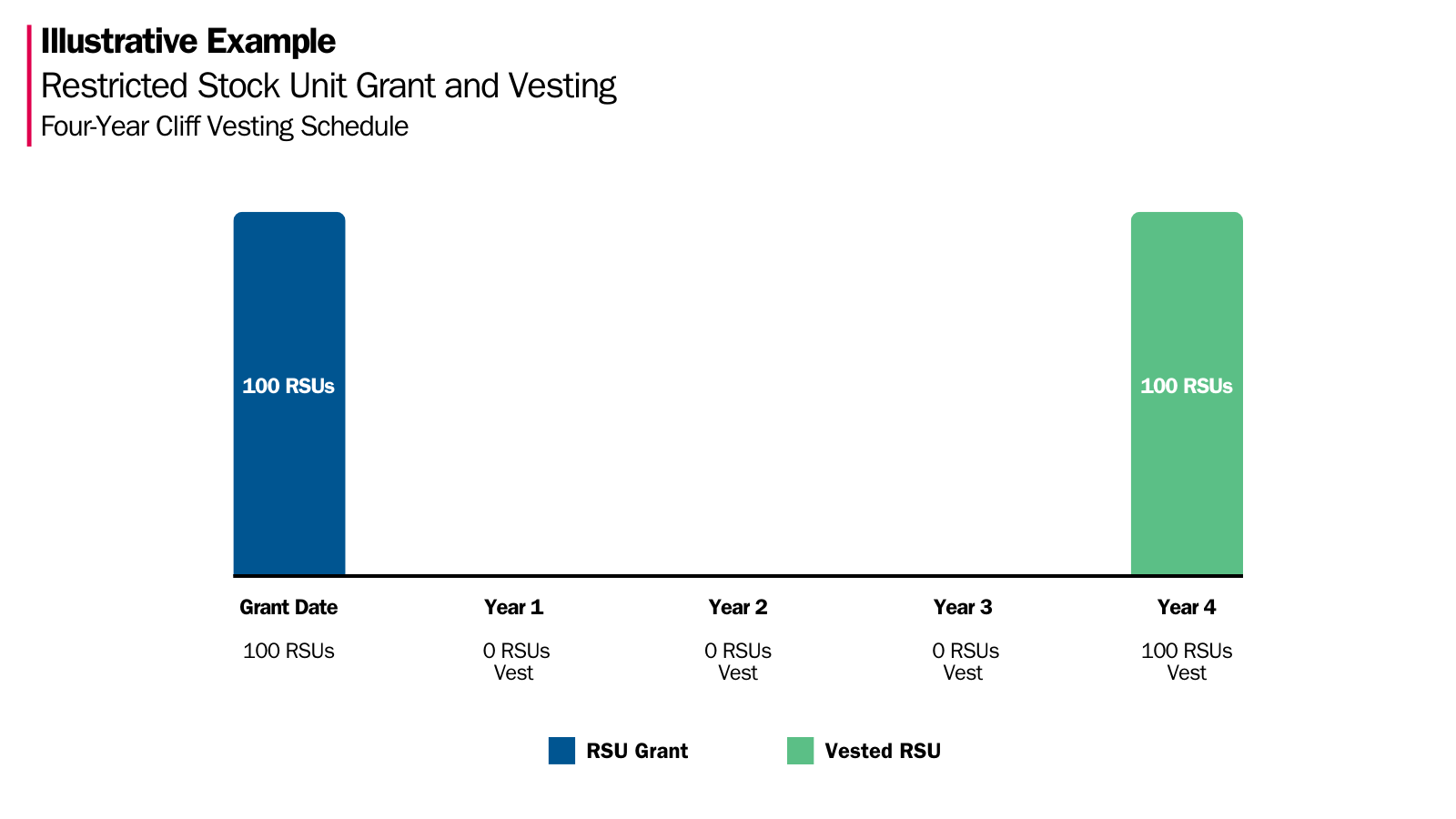

Cliff: Under this type of vesting schedule, all your restricted stock units vest at a specific time after their grant date. For example, your RSUs might vest on the 3- or 4-year anniversary of the grant date.

Your award agreement might state that your restricted stock/share unit “vests on the third anniversary date of the grant date and will be paid to the Participant in Shares on the vesting date or within 90 days thereafter.”

Performance-based: In some cases, RSU grants may vest if the company achieves specific performance-based goals over a pre-determined time-period. If this is the case, it’s likely this form of equity compensation is called a performance share unit, or PSU.

Companies have flexibility as to which performance metric(s) they want to use, if any.

For example, a mix of performance-based metrics could include:

- 50% vest based on earnings per share growth over a set time period.

- 50% vest based upon return on invested capital.

Other performance-based metrics could include profitability, revenue, or EBITDA for example.

A Central Question to Consider

Once your RSUs vest, generally they will be taxed as ordinary income based on the fair market value of the shares you receive.

For this reason, many RSU awardees like you tend to view RSUs as a bonus payment.

You should consider the following question before your RSUs vest:

“If you had received the after-tax value of your RSUs as a cash bonus, would investing that cash in your company’s stock align with your financial goals?”

If your answer to this question is “no”, then you should evaluate selling the vested shares. Your decision could be guided by how concentrated your wealth is in your employer’s stock, as well as your other financial goals and priorities.

As an investor, you should consider the amount and duration of your labor capital relative to your investable wealth. For example, if your labor capital is a relatively small part of your overall wealth, your labor capital should have less influence on your diversification and asset allocation.

If your labor capital is a significant source of wealth creation for you and your family, that should have more influence on your asset allocation decisions.

You’ll also want to evaluate your restricted stock units in the context of your entire investment portfolio. Holding a significant portion of your wealth in your company’s stock increases the concentration risk of your investments. It decreases the amount of diversification and could take a long-term investor like you away from achieving your financial goals.

Tax Planning When Your RSUs Vest

If you have restricted stock units, you’ll want to understand how they are taxed, as well as how and when you pay these taxes.

While your specific facts and circumstances will affect how your RSU’s will be taxed, the following is an overview of the different taxes that could affect your restricted stock units when they vest:

- Federal Supplemental Tax1:

- If your total annual supplemental wages are greater than $1 million, your employer must withhold tax on the amount over $1 million at the highest rate of income tax allowed by federal law, which is currently 37.0%.

- If your supplemental wages are $1 million or less, the minimum withholding rate is currently 22.0% (and no other percentage is allowed)

- State Supplemental Tax: For example, this rate is currently 4.80%2 for Missouri taxpayers. As another example, Ohio taxpayers can pay as high as 3.5%3 depending on their adjusted gross income.

- Social Security Tax: 6.20% on your first $168,600 of wages.

- Additional Medicare Tax: If your total household annual income is greater than $200,000, the current rate is 0.90%.

- Medicare Tax: 1.45% on wages that exceed $250,000 for those married filing jointly. This will vary depending on your filing status.

This is where a stock-settled RSU’s taxation at vesting can deviate from a cash bonus. Specifically, the federal supplemental tax, with its fixed rates, could create a false belief that you’ve accurately paid all the taxes owed as of the RSU vesting. How so?

If your employer elects to use the 22% rate method on your vested RSUs, and the vested RSUs increase your marginal tax rate above 22%, you’ll want to have a plan for paying the remaining taxes you owe.

If you want to understand the specific tax planning opportunity around your RSUs, you’ll first want to understand your marginal income tax rate as well as whether you are subject to the alternative minimum tax (AMT).

As you evaluate your restricted stock units, keep in mind how their vesting influences your taxable income, and therefore your eligibility to contribute to certain accounts, like a Roth IRA.

It can also determine whether you qualify for other tax benefits.

Tax Planning: Capital Gains and Losses

If you decide to hold the underlying shares of your vested restricted stock units, your cost basis of those shares will be equal to the fair market value at vesting.

When you choose to sell shares, the capital gain or loss for those shares will be based on the difference between your cost basis and the sale price.

For a more detailed discussion on investment taxes generally, the following article provides some additional education and insights for RSU holders to consider.

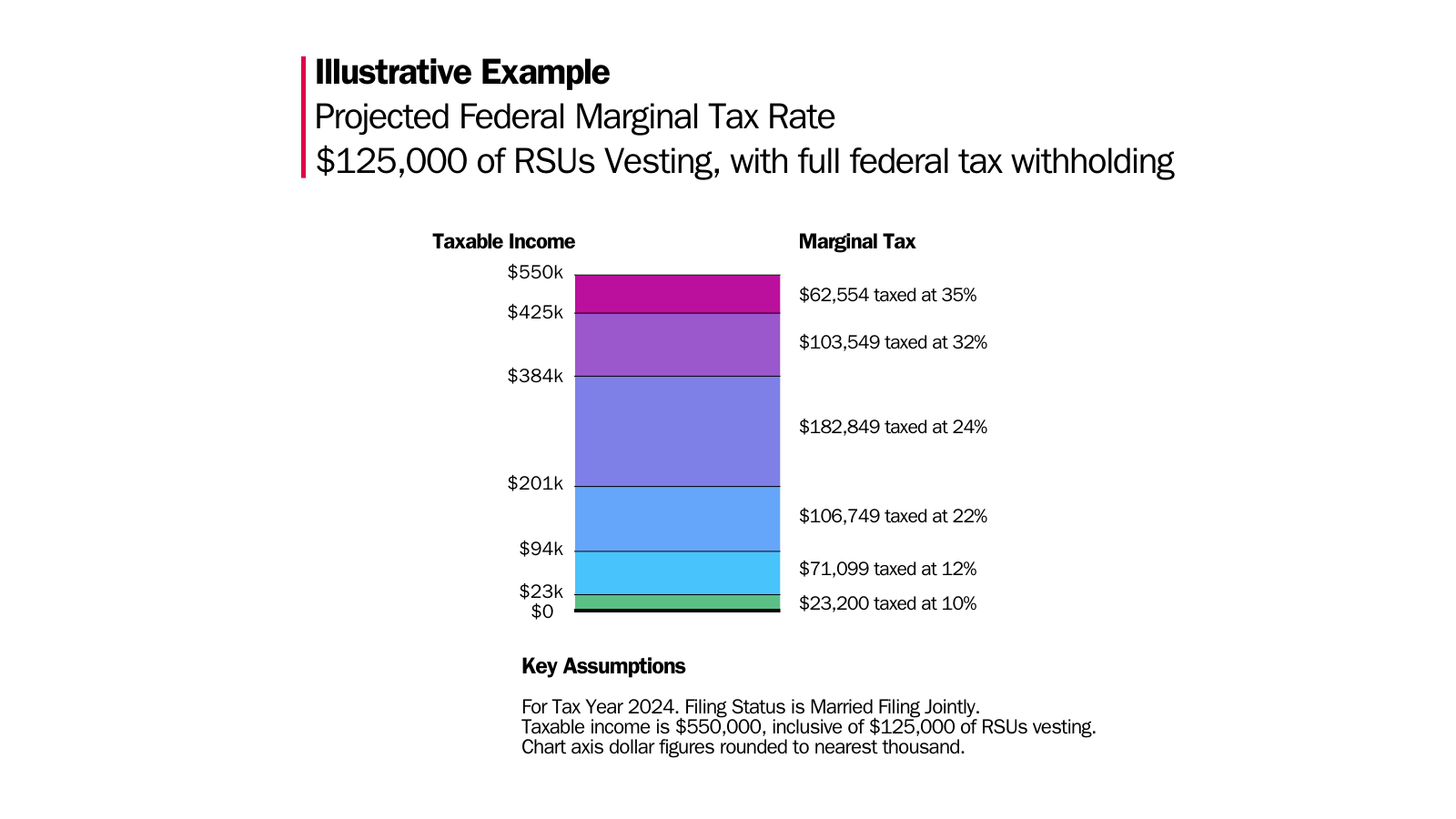

An Illustrative Example: Restricted Stock Unit Minimum Tax Withholding

The following 3-part illustrative example highlights this restricted stock unit projected federal tax gap. It is an oversimplification, and does not consider the full tax facts around a specific situation, including whether the taxpayer is subject to AMT.

With that additional context, let’s dive in:

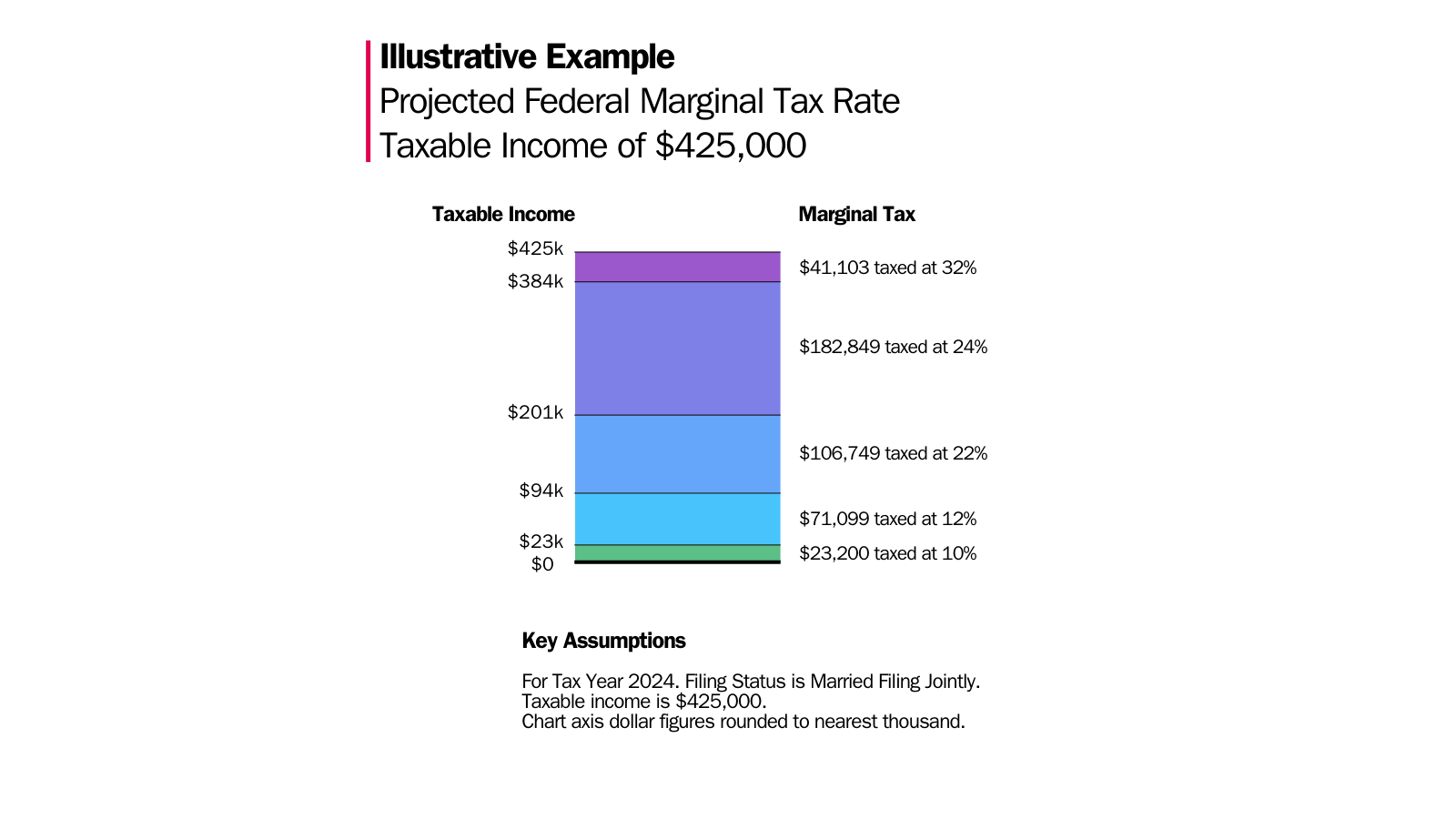

Part 1, Baseline. A household elects the Married Filing Jointly filing status and earns 425,000 of taxable income. This illustrative example project how their income is distributed across the relevant tax brackets.

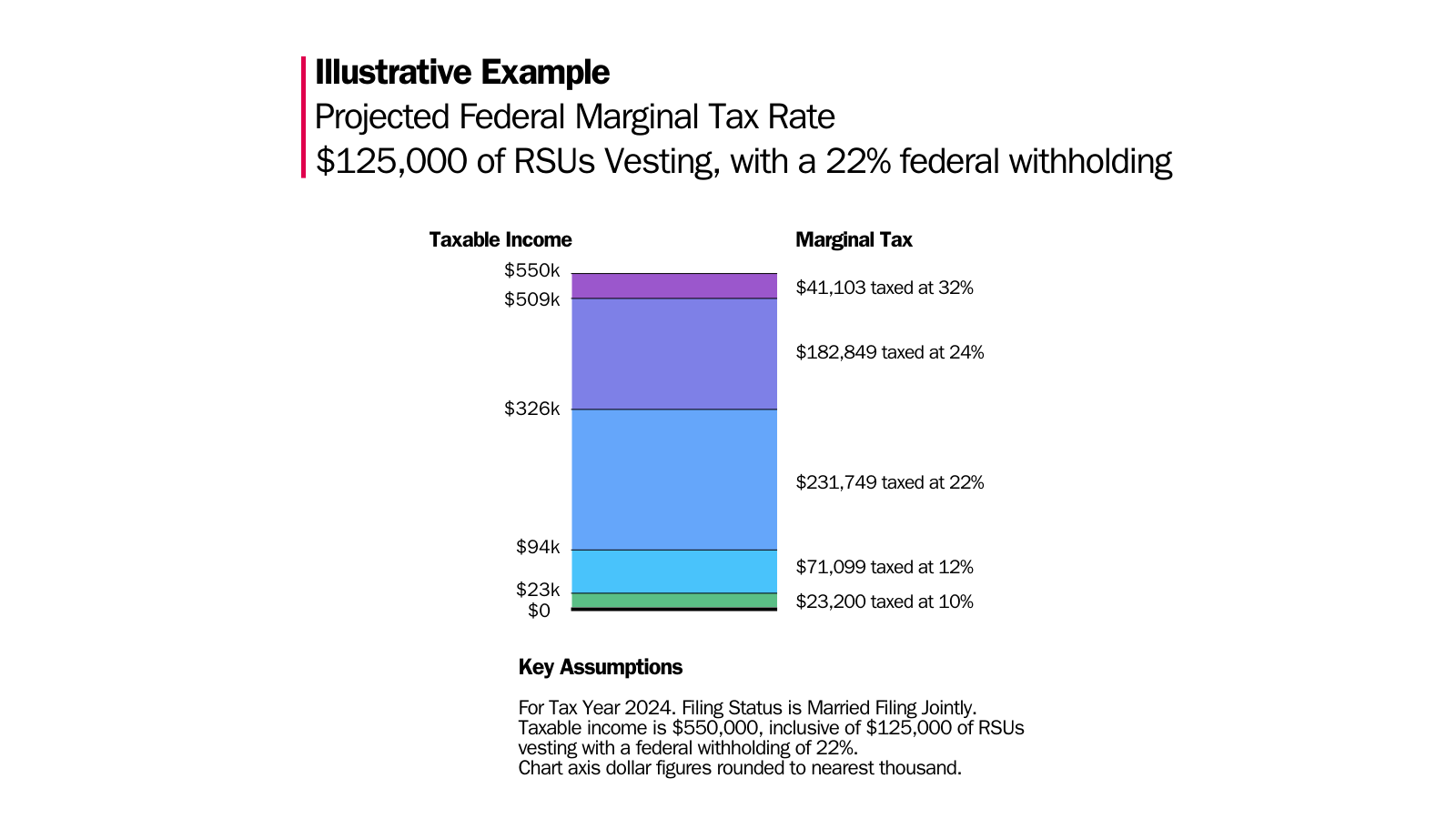

Part 2, RSUs Vest and 22% Minimum Withholding Applied. A household elects the Married Filing Jointly filing status and earns $550,000 of taxable income. Of which, $125,000 is attributable to vested restricted stock units. The vested RSUs have the minimum federal supplemental tax withheld at 22%. This illustrative example shows the projected distribution of taxable income across the relevant tax brackets.

The projected tax gap is most noticeable in the 22% marginal bracket, where all $125,000 of the vested RSU’s taxable income has been incorrectly allocated.

Part 3, RSUs Vest and Federal Taxes Reasonably Projected. A household elects the Married Filing Jointly filing status and earns $550,000 of taxable income. Of which, $125,000 is attributable to vested restricted stock units. This illustrative example shows the projected distribution of taxable income across the relevant tax brackets.

The tax gap has been corrected. Of note, the household’s additional taxable income from the vested RSUs is projected to flow into the 32% and 35% brackets.

Takeaway: Your Projected Federal Marginal Tax Rate

A key takeaway from these illustrative examples is that only relying on a 22% minimum withholding could create an unanticipated underpayment of your federal taxes. These projected federal marginal taxes illustrate a potential $14,377 federal tax gap that you’ll need to pay. This tax gap does not include any of the other

Another takeaway that is not shown in the illustrative example is that you’ll also need to factor in all the other taxes mentioned earlier. This will further increase the projected tax gap when your RSUs vest.

Your qualified tax professional and financial advisor can coordinate with you to determine how much additional tax you’ll owe, and the actions needed to close this gap.

If these are stock-settled RSUs, remember you’re not receiving cash. You’re receiving shares of stock. If you’re unable to adjust your withholdings prior to receiving the underlying shares, you can still close a projected tax gap.

Specifically, you can complete quarterly estimated tax payments or increase your withholdings from your paycheck by updating your Form W-4. If you are unaware or do not plan appropriately, a projected tax gap could create unanticipated cashflow and tax issues for you and your family.

Luckily, if you know this situation could occur, you have time to identify when you need to navigate these planning opportunities or engage with qualified professionals to help you get it right.

Federal Quarterly Estimated Payments

If you’re considering the quarterly estimated payments approach, you’ll want to set reminders for when those federal payments are due.

| Payment Period | General Due Date | Tax Year 2024 Due Date |

|---|---|---|

| January 1 – March 31 | April 15 | April 15, 2024 |

| April 1 – May 31 | June 15 | June 17, 2024 |

| June 1 – August 31 | September 15 | September 16, 2024 |

| September 1 – December 31 | January 15* of the following year. *Refer to Publication 505 for additional details. | January 15, 2025 |

A Practical Consideration: How You Pay Taxes on Your RSUs

First, you’ll want to review the agreement governing your restricted stock units and understand how taxes will be deducted from your RSU distribution at vesting. Your award agreement could state that a portion of your vested RSUs will be withheld and sold to pay for any taxes owed.

From the second illustrative example, in which $125,000 restricted stock units vest and 22% is withheld for taxes ($27,500), you’ll then receive $97,500 worth of the underlying stock.

You’ll also want to explore whether your RSU agreement contains additional language allowing you to proactively request your company to withhold more than the minimum required tax withholding.

If not, you’ll either need to have the cash on hand to pay the taxes when they are due or sell the correct amount of shares to raise the appropriate amount of cash for the taxes you owe.

The latter approach could have additional downstream tax effects like short-term capital gains or losses.

The Next Step

When you know who and what are truly important, you can create incredible clarity about your spending and saving.

Clarity to confidently spend on things that matter. Clarity to avoid spending your hard-earned resources on things that aren’t aligned with what you want in life.

As your financial planner in Saint Louis, we can help you plan for the future and enjoy the present moment.

Start feeling more confident that you are making progress toward your savings priorities and know what you need to do with your hard-earned restricted stock units.

Proactive and open collaboration with your financial, tax, and estate planning professionals can help you work towards your financial goals. Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

References

1 Internal Revenue Service, (Circular E), Employer’s Tax Guide (2024) § 7.

2 Missouri Department of Revenue, State of Missouri Employer’s Tax Guide (2024), § 7. A.