An employee stock purchase plan (ESPP) allows you to buy shares of stock in your employer. You can often buy shares with up to a 15% discount in a qualified ESPP. When you understand key terms, rules, and considerations, you can make more informed and tax-aware choices. Feel more confident and prepared during your next ESPP enrollment window.

Learning Points

Overview of Employee Stock Purchase Plans (ESPP)

If your employer’s stock is publicly traded in the United States, you may be eligible to participate in an employee stock purchase plan as part of your employee benefits package. You might know it as your company’s ESPP.

One of the key features of an ESPP is that it allows eligible employees to purchase company shares at a discounted price through after-tax payroll deductions.

The discount can be as high as 15% for a qualified employee stock purchase plan. Meaning, as an ESPP-eligible employee, you could elect to purchase company stock at a price significantly below its current fair market value.

The ESPP’s discount percentage is set by each company. Generally, you can expect to see this vary between 5%-15% for qualified ESPPs. Some ESPPs provide no discount. And so, if you find yourself discussing different ESPP offerings with a friend or member of your family, you could see some variation in this discount percentage from one company to another.

For this discussion, we’ll assume you are eligible to participate in a qualified employee stock purchase plan. Meaning, the ESPP fulfills the related regulatory requirements of Section 423 of the Internal Revenue Code. You’ll want to confirm with your employer whether your ESPP qualifies.

In the context of your family’s investment goals, holding a significant portion of your wealth in your company’s stock can increase the concentration risk of your investments. Doing so can decrease your investment portfolio’s diversification and could potentially take you away from achieving your financial goals. You’ll want to evaluate your employee stock purchase plan in the context of your personal situation.

Read on to explore key terms, examples, and tax planning considerations.

Employee Stock Purchase Plan (ESPP) Key Terms and Concepts

Eligible ESPP participants have the option to purchase discounted shares of employer stock by accumulating payroll deductions from eligible compensation. Your ESPP payroll deductions are after-tax dollars, meaning you’ve already paid taxes on that compensation when you contribute it to an ESPP.

The mechanics and timing of ESPP payroll deductions are like 401(k) plan contributions. Specifically, once you establish how much you want to contribute to your ESPP, the deductions can occur each payroll cycle.

Like so many other topics in personal finance, it’s helpful to familiarize yourself with the terms you are most likely to encounter when you’re reviewing materials relating to your specific employee stock purchase plan. Each ESPP is unique.

You’ll want to familiarize yourself with the specific terms and conditions governing your ESPP.

With that in mind, let’s explore the key terms and concepts, in chronological order, of your qualified employee stock purchase plan experience:

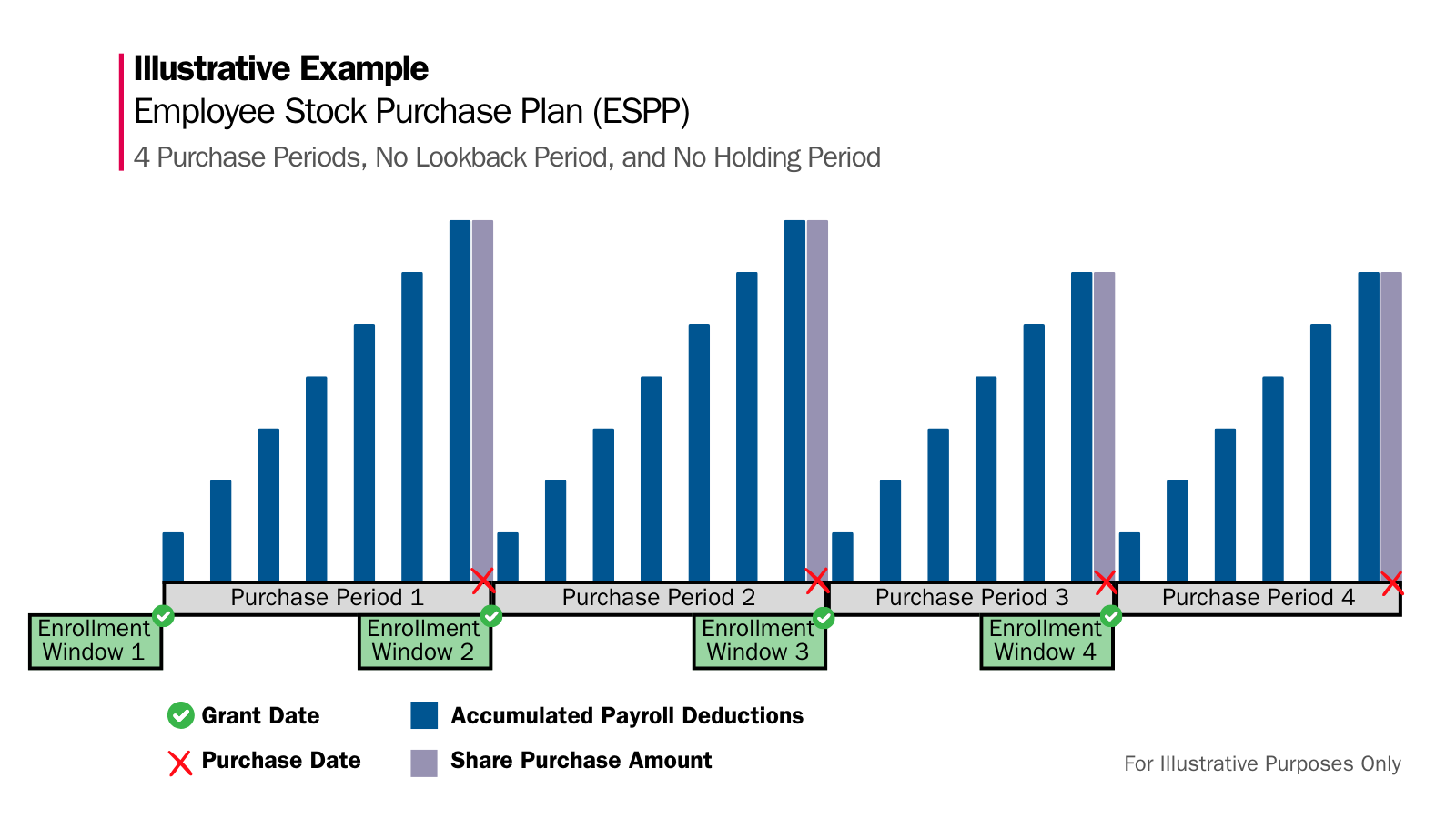

Enrollment Window / Date(s)

The period you can enroll to be eligible to participate in your ESPP’s next offering/purchase period.

Keep in mind that some companies have specific eligibility requirements governing if, or when, you can enroll in the ESPP.

For example, a firm might exclude highly compensated employees or part-time employees who work 20 hours or less per week. Others might require you to complete a specific length of tenure before you are eligible.

Review your ESPP materials, and if you intend to participate in the plan, enroll in the plan by the deadline. If you miss the enrollment deadline, you’ll have to wait until the next enrollment window, which could be a year later.

Grant Date

This is the first day of the offering/purchase period. This date is important because it helps establish the following elements:

- determines the stock price to be used for calculating the $25,000 contribution limit.

- serves as the point for calculating any lookback price, if this is a feature of your ESPP.

- starts the clock when determining whether the future sale of shares is a qualifying or disqualifying disposition.

- is used in calculating the amount of compensation income during a qualifying disposition.

Eligible Compensation

Your ESPP will define whether this includes your salary, commissions, bonuses or current cash awards, for example.

Contribution Amount/Percentage

Your ESPP will ask you to elect a specific percentage of your after-tax payroll to contribute to your ESPP each pay period.

Employee Stock Purchase Plans can require participants to select a specific whole number percentage for this election. An ESPP can also set specific maximum and minimum amounts that eligible participants can elect, too.

If your ESPP has a different method or allows you to specify a whole dollar amount, for example, review your options, including the plan literature, and do what works best for your specific situation.

Contribution Limit: Calendar Year Method

An Employee Stock Purchase Plan’s contribution limit is a central concept for qualified ESPPs.

Specifically, a qualified Employee Stock Purchase Plan limits participants from purchasing more than $25,000 worth of shares each calendar year, which is based on the fair market value of the underlying stock on the grant date.

If your ESPP provides a discounted purchase price, you can determine your maximum ESPP contribution amount by multiplying the $25,000 limit by the discount percentage. Here are a few maximum contribution calculations using common discount percentages:

- ESPP with a 5% discount on Purchase Price: $25,000 x (1 – .05) = $25,000 x .95 = $23,750

- ESPP with a 10% discount on Purchase Price: $25,000 x (1 – .10) = $25,000 x .90 = $22,500

- ESPP with a 15% discount on Purchase Price: $25,000 x (1 – .15) = $25,000 x .85 = $21,250

And so, the higher your ESPP’s discount percentage, the less payroll contributions you’ll need to reach the maximum $25,000 fair market value limit.

While it’s an intuitive algebraic formula, highlighting the difference between the $25,000 fair market value and the actual annual payroll contribution limit can help with your personal cash flow planning.

Anticipating that you had $3,750 less to fund your other savings priorities, only to be surprised toward the end of the year, isn’t ideal.

Your employee stock purchase plan literature should clearly state your maximum annual payroll contribution amounts.

The above examples highlight a common, calendar year basis method for calculating maximum employee contributions.

If your ESPP provides a multi-year offering period, eligible employees could accrue the right to purchase more than $25,000 worth of stock in the later years of the offering period if no purchases occurred in the first year.

While multi-year offering periods are more rare than common, this topic is worth exploring in greater detail in a later, separate post.

Offering/Purchase Period

The period of time when your payroll deductions are taken from your base salary paycheck on an after-tax basis. These are the predetermined intervals/dates at the end of which your accumulated payroll deductions are used to buy company stock.

Some ESPPs have a purchase period equal to the length of the offering period. Other plans have multiple purchase periods within a single offering period.

Purchase Date

The final day of the purchase period, during which your accumulated payroll deductions buy company stock.

Fair Market Value

This is primarily determined by reference to the closing price of the stock on a national securities exchange. For example, the closing price of the stock on the purchase date.

The final day of the purchase period, during which your accumulated payroll deductions buy company stock.

Purchase Price

The fair market value price of the stock, less your ESPP’s discount (if any).

Review your plan to determine whether you will pay brokerage fees, commissions, or other costs on the purchase. Frequently these fees are waived on the purchase of ESPP shares.

Note that you could incur brokerage fees, commissions, and other costs on any subsequent sales of shares.

Purchase Limit

Your ESPP might stipulate a maximum number of shares you can purchase during each offering period, subject to the annual contribution limit.

Example Calculation: ESPP Purchase Price with a Fixed Discount

An Employee Stock Purchase Plan that discounts its share price by a fixed percentage has the following facts:

- ESPP discount percentage = 15%

- Purchase Price is equal to 85% of the fair market value price on the last day of the purchase period.

- Fair Market Value: $100.00/share

Here’s an example of how to calculate the discounted price per share:

- (1 – .15) x $100.00 = 85% x $100.00 = $85.00 purchase price per share

Lookback Period

A company can choose whether to include this feature in its ESPP. If it is available in your ESPP, the purchase price is based on the lower of the two fair market values.

For example, an ESPP could choose to measure the discounted purchase price on the first or last date of the purchase period and select the lesser of the two values.

It’s important to understand that a lookback feature does not necessarily allow you to purchase stock at the minimum fair market value price the stock exhibited throughout the offering period. An ESPP could choose to use both a discount and lookback period:

An ESPP with a lookback period could determine the purchase price as the lesser of either:

- 85% of the Fair Market Value on the first day of the Purchase Period; or

- 85% of the Fair Market Value of the last day of the Purchase Period.

To better understand how the lookback works, let’s construct an example with hypothetical values.

Example Calculation: ESPP with a Lookback period vs. Without a Lookback Period

An Employee Stock Purchase Plan that discounts its share price by a fixed percentage has the following facts:

- Price on Grant Date/First Day of Purchase Period: $25.00

- Price on Last Day of Purchase Period: $35.00

- ESPP Discount: 15.0%

Lookback ESPP: Purchase Price: $25.00 x (1 – .15%) = $21.25 / share

No Lookback ESPP: Purchase Price: $35.00 x (1 – .15%) = $29.75 / share

In this example, the lookback feature allows the hypothetical ESPP participant to purchase shares for $8.50 less per share ($29.75 – $21.25 = $8.50) than if the lookback feature was not included.

Now, compared to non-ESPP participants who purchased shares for $35.00/share on the last day of the purchase period, the ESPP participant was able to purchase shares for $13.75 less per share.

Again, these are hypothetical examples intended to show how the lookback and discount features work within an employee stock purchase plan.

All else equal, together these two features can make an Employee Stock Purchase Plan more compelling to participant in.

After your share purchase is complete, the stock becomes your property.

Whether you want to continue to hold the stock will depend on your goals and personal financial situation. You’ll want to understand how an ESPP can support your overall financial goals. Whether that means you diversify your investments away from your employer’s stock to achieve your financial goals or continue to hold the shares for a specific purpose.

When an ESPP is one of the many pieces of your financial life, it’s important that you proactively and efficiently review, monitor, and take action on your ESPP-related holdings.

Because topics like employee stock purchase plans, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with a qualified tax professional.

Once you understand the terms and conditions of your employee stock purchase plan, and how they apply to your personal situation, the more accurately you can plan for when you are eligible to participate in your company’s ESPP.

So far, we’ve covered some details relating to purchasing and maintaining your Employee Stock Purchase Plan shares.

In our next post, we’ll explore what happens when you sell your ESPP shares.

The Next Step

When you know who and what are truly important, you can create incredible clarity about your spending and saving.

Clarity to confidently spend on things that matter. Clarity to avoid spending your hard-earned resources on things that aren’t aligned with what you want in life.

As your financial planner in Saint Louis, we can help you plan for the future and enjoy the present moment.

Start feeling more confident that you are making progress toward your savings priorities and know whether participating in your employee stock purchase plan aligns with your goals.

Proactive and open collaboration with your financial, tax, and estate planning professionals can help you work towards your financial goals. Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

If you’re unsure about your next step, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.