For working parents, whether you want to save and invest for your retirement, your children’s education, or you’re wondering what to do with your year-end bonus, now is a great time to revisit your savings priorities and evaluate your progress. Navigating the unknowns of life can be easier when you know you’re on track financially and feel better prepared.

Learning Points

Evaluating Your Progress on Key Savings Priorities

Whether your next couple of months are punctuated with travel to be with family or gatherings with dear friends, there has never been a better time to evaluate your progress on your savings priorities.

Perhaps you’ve been saving in your 401(k) and you’re ready to increase how much you contribute in 2025.

Or you’re balancing creating memories with your family this year and keeping your retirement plan on track.

Perhaps you completed your benefits open enrollment and elected to open a Health Savings Account in 2025.

Or you’re anticipating a significant year-end bonus or restricted stock unit award. Aside from the payroll taxes, do you have a plan for the money?

Evaluating your progress on your savings priorities can help you identify potential adjustments to keep you on track. Making steady progress on your savings priorities can create additional financial flexibility for you and your family when your life changes.

While each of these savings priorities might not be your current priority, they could become future savings priorities for you to explore in the future.

Expand your emergency fund to 6-, 12-, or 18-months

If it’s comforting to know you have 6-, 12-, or 18-months’ worth of cash to cover your family’s expenses, consider adding to your emergency fund. Increasing your emergency fund savings can be beneficial if your income is tied heavily to variable compensation, a volatile industry, or if you are self-employed.

One drawback to saving more in your emergency fund is the opportunity cost of not investing in other priorities, like funding your retirement. Understanding the cost of choosing one path instead of another can help you quantify which approach best aligns with your specific situation.

For some people, choosing to save more in an emergency fund allows them to feel more in control of their future. To feel like they have a stronger ability to absorb negative financial events in the future.

Contribute to Your 401(k) to Obtain a Full Company Match

Your employer’s 401(k) plan matching program is a benefit you should evaluate each year. If your employer offers this benefit, your employer is incentivizing your retirement savings.

How? By matching a percentage of your salary that you contribute to the company retirement plan up to a specific dollar amount.

Here are two common 401(k) company match methods you might be familiar with:

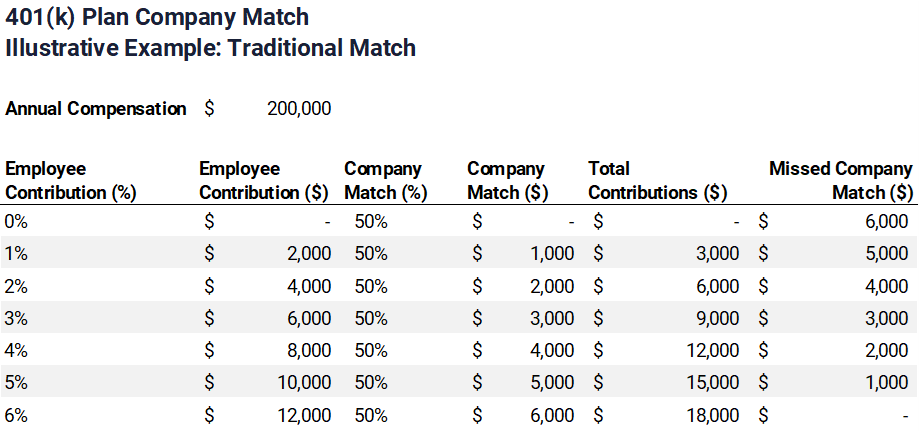

- Traditional matching contribution: Under this design, the employer matches a certain percentage of the employee’s contribution, up to a certain limit. For example, an employer might offer a 50% match on the first 6% of an employee’s salary that the employee contributes to their retirement plan.

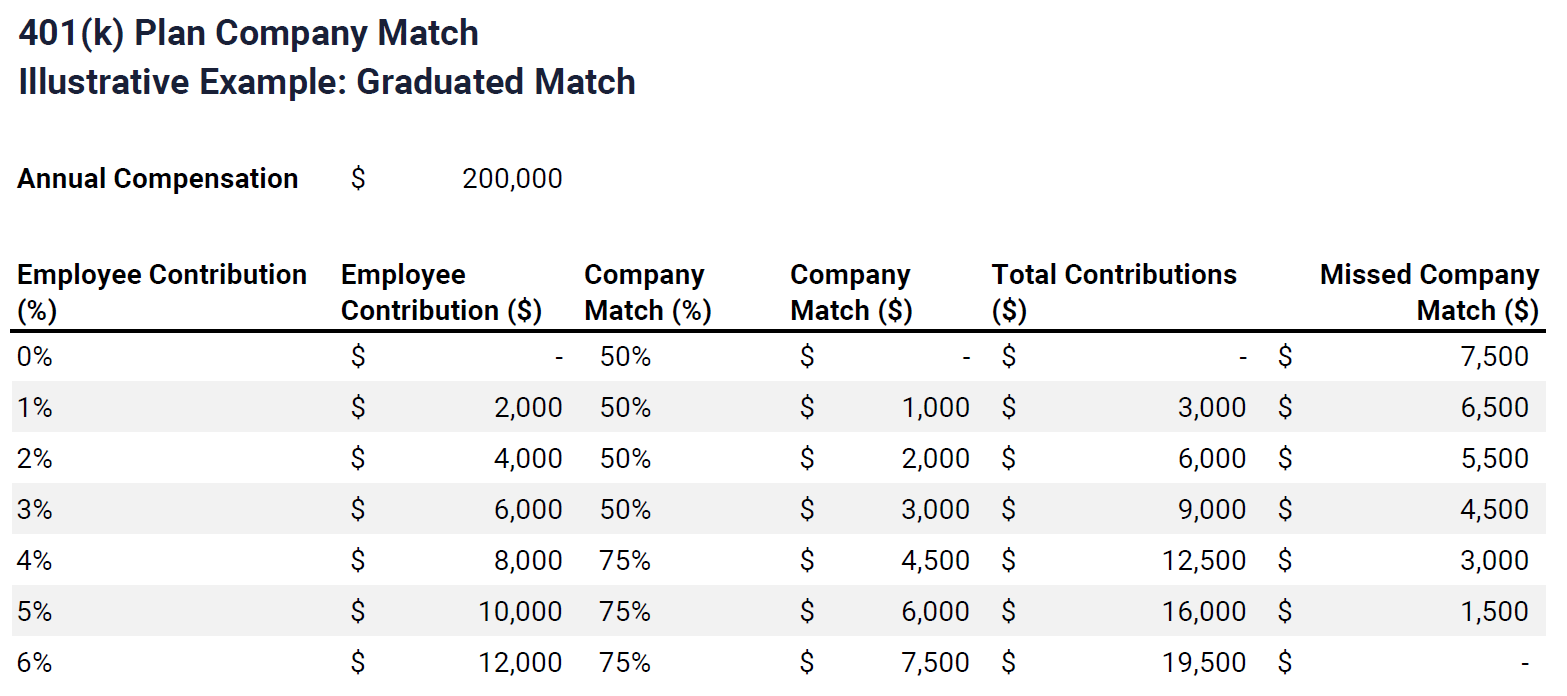

- Graduated matching contribution: Under this design, the employer’s match increases as the employee’s contribution level increases. For example, the employer might offer a 50% match on the first 3% of an employee’s salary, and a 75% match on the next 3%.

The following two illustrative examples highlight how each of these matching contribution methods works using some basic assumptions like hypothetical annual compensation.

By contributing enough to receive the full company match amount offered each year, you’re maximizing this employee benefit.

If your savings priorities don’t include maximizing your 401(k) contribution, evaluate whether you can contribute an amount that allows you to receive the full company match.

Think you’ve got this one covered?

Let’s review some other savings priorities so you can evaluate your own progress as you approach the end of 2024.

Evaluate Contributing to a Health Savings Account (HSA)

If you have a Health Savings Account (HSA), you can use your HSA as a personal savings account to pay for qualifying medical expenses.

Your HSA is paired with high-deductible health plans (HDHPs), which generally have lower monthly premiums compared to traditional health insurance plans but require individuals to pay a higher deductible before their insurance coverage begins.

HSA contributions, earnings, and qualifying distributions are tax-advantaged.

In 2024, the contribution limit for an individual with self-only HDHP coverage is $4,150, and the limit for an individual with family HDHP coverage is $8,300. Practically, this means you and your spouse can contribute a maximum aggregate amount of $8,300 to all your HSAs in 2024 if you have a family HDHP.

Evaluate whether you’ve contributed the right amount to your HSA this year based on your personal situation.

What adjustments, if any, do you anticipate making in 2025?

Does your high-deductible health plan still fit your family’s needs?

Keep in mind that you can pay for qualified medical expenses now, save the related receipt(s), and reimburse yourself years or decades later. That creates the opportunity for your HSA to stay invested over a longer time period.

Refresh your understanding of your HSA details with this brief overview.

Estate Planning Essentials

If you died, how would your assets transfer to your loved ones? Account titling is a key element of your estate plan. Account titling determines who can manage the specific asset during your lifetime. It also helps determine how your assets are distributed upon your death.

Proper account titling and beneficiary designations can help determine how your assets will transfer.

Your approach to asset or account titling determines how you want to manage your assets during your lifetime. It also helps determine how your assets are distributed upon your death according to your will based on state law, agreement, or beneficiary designation.

Have you reviewed your accounts and verified that you’ve properly titled each account and designated the correct beneficiaries?

Assessing Your Insurance Coverages

Reviewing insurance policies can help you build a strong foundation for your personal finances. Think about how you can make progress in your financial life, so that you can continue to focus on the people and experience that matter.

- When reviewing insurance, like your auto policy, it can be helpful to consider how you’re protected against a “worst-case” scenario.

- What additional endorsements provide more complete coverage for your homeowners insurance? In Missouri, you’re likely to need an earthquake endorsement if you have a mortgage. Or, if you have a finished basement, have your evaluated ways to

- If you coach youth sports, have young/inexperienced drivers, or have significant property or assets, is your umbrella insurance policy adequately covering your family?

What’s the right balance of deductibles and policy coverages that let you sleep well at night?

Here are a few additional savings priorities to evaluate. Consider how you can make progress in your financial life beyond 2024, so that you can continue to focus on the people and experiences that matter.

Education Funding

If contributing to a 529 account is one of your savings priorities, keep in mind that here is no “one-size fits all” 529 strategy.

Here are some questions to consider as you re-assess your progress and education funding needs.

- When does your 529 beneficiary need to use the money?

- What kind of educational need, or needs, will the 529 fund?

- How much more do you need to contribute in 2024 to stay on track with your education funding goals?

How are you adjusting your investments as you get closer to paying for your child’s education?

IRAs: Traditional and Roth Considerations

An individual retirement account (IRA) is a tax-advantaged personal savings account generally used for setting money aside for retirement.

Depending on the type of IRA and your personal circumstances, these tax advantages can include tax-deductible contributions for traditional IRAs and tax-free withdrawals for Roth IRAs.

For most investors, IRAs generally complement, but do not fully replace employer-sponsored plans, like a 401(k) or a 403(b), for your retirement savings goals.

- If contributing to an IRA is one of your savings priorities, have you fully funded an IRA that’s right for your personal situation?

- If your spouse isn’t currently working have you evaluated funding a Spousal IRA?

How are your IRAs supporting your personal goals?

Charitable Giving Strategies: Charitable Bunching and Donor Advised Funds

When you make the time to directly volunteer for a charity to support its mission, you can show your children how they can connect your words and values to the real work of helping others. You lead by doing.

When you donate money or other assets to a charity, you signal to yourself, and family, that you’re going to be O.K. financially. That you have enough. It can dial down the noise from the outside world.

The feeling of “enough” can be a calming force, especially in the context of your financial plan.

You can align your financial plan with your savings priorities that directly support causes and organizations that matter to you and your family. When you take a strategic view of your philanthropy and combine it with thoughtful tax planning, you can efficiently share your resources with deserving public charities.

Charitable bunching occurs when you aggregate your charitable contributions for multiple years into a single year so that you can itemize your tax deductions in that year. In subsequent years you could then re-evaluate whether the standard or itemized deduction decision is right for you.

A donor advised fund is a tax-advantaged account – like a 401(k) is for retirement savings – with a specific, intended purpose.

Tax-advantaged means the tax code provides a benefit to the investment or account holder by making the investment or account exempt from taxation, deferred from taxation, or bear a reduced tax to the taxpayer.

A donor advised fund, or DAF, is a charitable investment account you can establish to support public qualified charitable organization(s). A DAF also allows you to take an immediate charitable deduction in the year of your contribution.

The Next Step: Taking a Strategic View of Your Finances

If you can take a more comprehensive view of your finances, you are better positioned to understand how you can work towards your savings priorities. A more complete view of all the elements of your financial life can help you evaluate the tradeoffs of funding specific savings priorities relative to others.

Are you on track for your short-term goals, like making memories with your family by going on vacations together? How confidently are you approaching saving and investing for your long-term aspirations, like retiring or pursuing a meaningful second career?

We help busy parents and professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s start a conversation.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.