You can align your financial plan to directly support causes that matter to you and your family. Thoughtfully combine your charitable goals with multi-year tax planning. Read on to learn how you can evaluate charitable donation bunching. The feeling of “enough” can be a calming force, especially in the context of your financial plan. Think about how you can make progress in your financial life, so that you can continue to focus on the people and experiences that matter.

Learning Points

Giving Your Money Meaning

Whether you donate your time and energy, or money to charity, it can be a powerful experience.

There is a reciprocal nature to intentional philanthropy. One that goes beyond the immediate benefits your volunteerism or charitable donation provides to an organization.

At its core, there is an underlying message that you’re communicating to yourself and your family. That message of enough. Of abundance and fulfillment.

When you make the time to directly volunteer for a charity to support its mission, you can show your children how they can connect words and values to the real work of helping others. You lead by doing.

When you donate money or other assets to a charity, you signal to yourself that you’re going to be O.K. financially. That you have enough. It can dial down the noise from the world around you. It can push back on the notion that you need more. More stuff. More money.

The feeling of “enough” can be a calming force, especially in the context of your financial plan. Think about how you can make progress in your financial life, so that you can continue to focus on the people and experiences that matter.

You can align your financial plan with directly supporting causes and organizations that matter to you and your family. When you take a strategic view of your charitable goals and efforts, and combine it with thoughtful tax planning, you can efficiently share your resources with deserving charities.

Because topics like charitable giving, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with a qualified tax professional.

Read on to explore how charitable donation bunching works and the potential tax planning opportunity it creates. Understand how different types of charitable donations compare to one another on an after-tax basis. Check whether this technique could work for your family’s specific situation.

Tax Planning for Charitable Contributions

If you’re considering donating money to charity and want to understand how it might influence your tax situation, evaluate whether you plan to itemize or take the standard deduction in a given tax year.

For taxpayers who itemize their deductions, charitable contributions, state and local taxes, and home mortgage interest are relatively common. This is especially true for taxpayers in high marginal tax brackets. If the sum of these itemized deductions is greater than your standard deduction, work with your qualified tax professional to determine the right deduction strategy for you and your family.

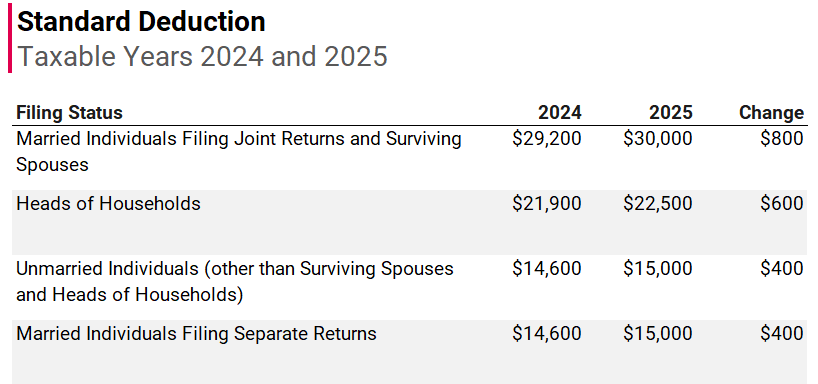

In general, for taxable years beginning in 2024 and 2025, the standard deduction amounts are as follows [i]:

Charitable Donation Bunching

If you regularly give set amounts of money to charity, but don’t have enough qualifying itemized deductions in a given tax year, evaluate whether a charitable donation bunching strategy aligns with your long-term goals and values.

Charitable donation bunching occurs when you aggregate your charitable contributions for multiple years into a single year so that you can itemize your tax deductions in that year. In subsequent years you could then re-evaluate whether the standard or itemized deduction decision is right for you.

If you are on the threshold between taking the standard deduction or itemizing to maximize your tax benefits, charitable donation bunching is worth evaluating in detail.

Adjusted Gross Income (AGI) Limits on Deductions

For purposes of charitable donation bunching, your deduction for charitable contributions generally can’t be more than 60% of your AGI.

In some cases, 20%, 30%, or 50% limits may apply. In the context of charitable donation bunching, two of the more relevant and applicable deduction limits to consider are the following [ii]:

- If you donate cash, via a check, wire transfer or credit card to specific types of qualified organizations, you’re generally eligible for an income tax deduction up to 60% of your AGI.

- If you donate long-term appreciated assets directly to charity or to a donor advised fund, you generally won’t have to pay capital gains. As such, you generally can take an income tax deduction in the amount of the full fair-market value, up to 30% of your AGI.

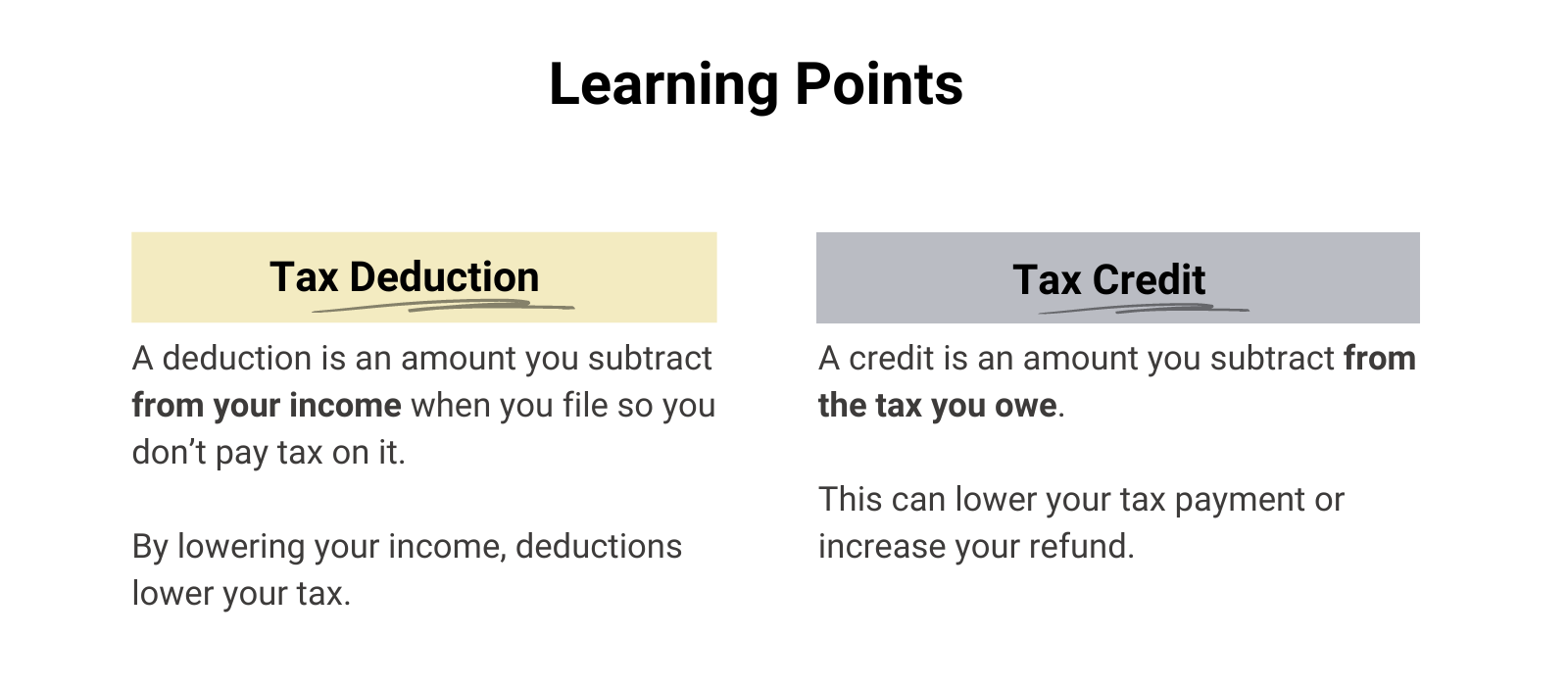

Understanding the Difference Between a Tax Deduction and a Tax Credit

As a quick refresher, remember the distinction between tax deductions and tax credits.

The amount you save with a deduction depends on your tax bracket. For example, if you’re in the 37% tax bracket, a $1,000 tax deduction could potentially save you $370 off your tax bill.

A tax credit reduces the tax you owe. For example, a $1,000 tax credit could potentially save you $1,000 off your tax bill.

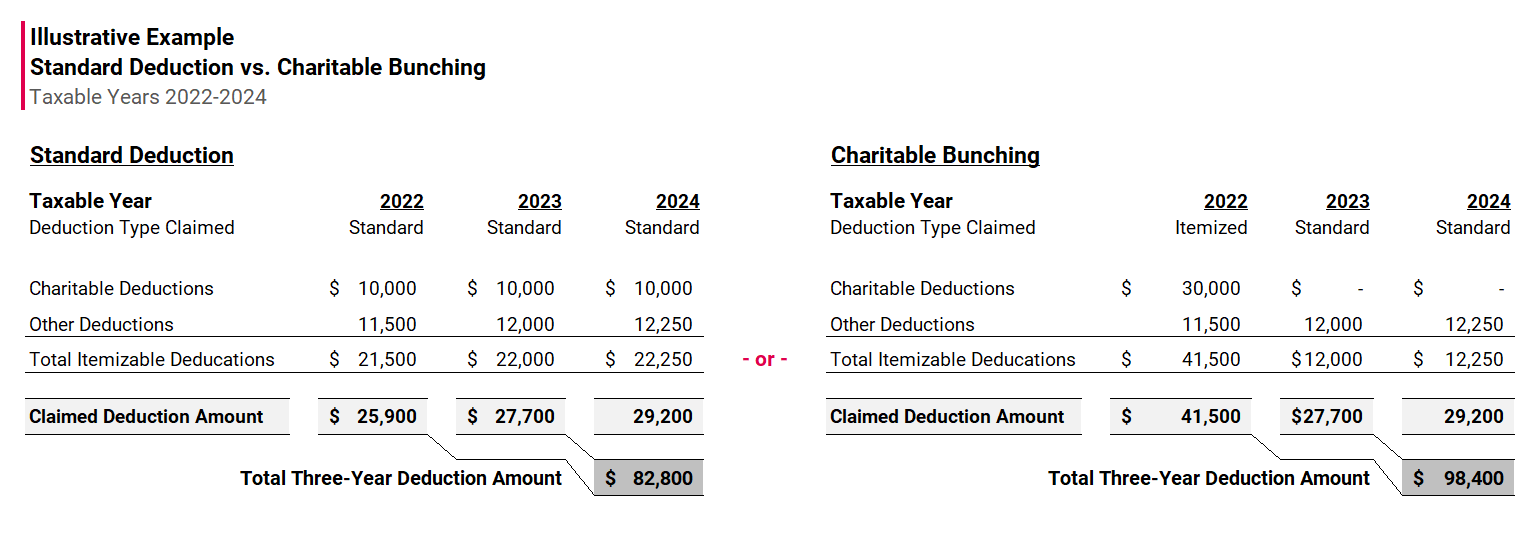

Illustrative Example: Standard Deduction vs. Charitable Bunching

To show how choosing the standard deduction compares to charitable bunching, consider the following illustrative example.

In the Standard Deduction hypothetical scenario, a couple who are married filing jointly contribute a fixed amount to charity in taxable years 2022, 2023, and 2024. They would claim the standard deduction in each of those taxable years. As such, they would have $82,800 in total, claimed deductions.

In the Charitable Bunching hypothetical scenario, a couple who are married filing jointly contribute three years-worth of charitable donations in taxable year 2022. They would not claim any charitable deduction in taxable years 2023 and 2024. They itemize their deductions in taxable year 2022, then claim the standard deduction in 2023 and 2024.

As such, they would have $98,400 in total, claimed deductions.

The difference in these two charitable giving approaches creates a difference of $15,600 in total claimed deductions over the same hypothetical three-year period.

If you are on the threshold between taking the standard deduction or itemizing to maximize your tax benefits, charitable bunching is worth evaluating in detail.

Note to Illustrative Example: This hypothetical example is only for illustrative purposes. Haven Wealth Planning does not provide tax or legal advice. Please consult your qualified legal or tax professional about your specific facts and circumstances.

In Practice: Charitable Donation Bunching Can Potentially Reduce Tax Burden in a Windfall Year

Depending on your specific facts and circumstances, charitable donation bunching could potentially reduce your tax burden after you experience a financial windfall.

Windfalls from infrequent or one-time events such as receiving an inheritance, selling a business, or experiencing uncharacteristically strong market returns.

A windfall could allow you to achieve years of planned giving with just a single donation using charitable donation bunching.

If you choose to pursue a charitable donation bunching strategy, consider communicating your intentions directly with the charity you are supporting. It can help the charity budget more accurately and fundraise more effectively.

The Feeling of Enough

As a thoughtful steward of your family’s resources, you can maximize the positive impact of your charitable efforts with long-term planning. When you set philanthropic goals, automate your saving for them, and create a plan designed for your specific situation you’ll be more likely to achieve your goals.

Your philanthropy can foster a deeper connection with your family and loved ones. You can instill and reinforce your family’s virtues with your charitable planning and actions.

The feeling of “enough” can be a calming force, especially in the context of your financial plan.

When you align your wealth with your thoughtful, generous spirit, you can give your money meaning.

Hopefully this educational overview of charitable donation bunching allows you to be more informed and prepared to evaluate and support your own charitable goals. Charitable donation bunching, like so many other topics in financial planning, intersects with the world of tax, please make sure you coordinate with a qualified tax professional.

The Next Step

Frequent, proactive, and open collaboration with your tax and estate planning professionals can help you work towards your financial planning goals.

Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

As your financial planner in Saint Louis, we can help you get organized and assess your family’s charitable giving options, like charitable donation bunching. Start feeling more confident that you are making progress toward your savings priorities.

Who is providing you with the right kind of accountability and collaboration in your personal financial life?

When you know who and what are truly important, we can help you create incredible clarity about your spending and saving. Clarity to confidently plan for the future and enjoy the present moment.

If you’re ready to take your next step, let’s talk.

[i] Source: Internal Revenue Service, Rev. Proc. 2024-40. https://www.irs.gov/pub/irs-drop/rp-24-40.pdf. Accessed: November 25, 2024.

[ii] Source: Internal Revenue Service, Publication 526, Charitable Contributions. https://www.irs.gov/pub/irs-pdf/p526.pdf. Accessed: November 25, 2024.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.