For busy, working parents and professionals, saving for retirement using a Health Savings Account (HSA) might not feel like a top priority. Whether you already have an HSA or are considering opening one, spend a few minutes exploring the benefits, drawbacks, and practical considerations of an HSA. Read on to refresh your understanding of HSAs. Feel more confident in evaluating whether contributing to a Health Savings Account aligns with your financial goals.

Learning Points

Health Savings Accounts: Overview

Your Health Savings Account (HSA) is a personal savings account that you can use to pay for qualifying medical expenses. When you regularly contribute to your HSA, and align your HSA investments with your personal goals, your account earnings can potentially grow tax-free until you need to access these funds.

Your withdrawals of contributions and earnings are tax- and penalty-free when used for qualified health care expenses.

In short, you create the option to reimburse yourself for future medical expenses in a tax-advantaged way.

Health Savings Accounts are paired with high-deductible health plans (HDHPs). HDHPs generally have lower monthly premiums compared to traditional health insurance plans but require individuals to pay a higher deductible before their insurance coverage begins.

With that basic understanding, here are some beneficial features of health savings accounts to consider:

- Contributions to a Health Savings Account are tax-free: If you fund your HSA up to or below the annual contribution limits, those contributions are not taxed as income at the federal level.

- Earnings in a Health Savings Account are tax-free: Any earnings on the money in your HSA (e.g., interest or investment returns) are tax-free if the funds are used to pay for qualifying medical expenses.

- Withdrawals from an HSA for qualifying medical expenses are tax-free: If you use the money in your HSA to pay for qualifying medical expenses, the withdrawals are tax-free. This means that you won’t have to pay any taxes on the money you withdraw from your HSA to pay for medical expenses.

- No Required Withdrawals: There is no requirement that you spend down your HSA account balances starting at a certain age. Looking ahead, once you reach age 65, HSA withdrawal restrictions become relatively more permissive. Specifically, from age 65 and older, you can use your HSA funds for any purpose without any penalty tax. However, if you withdraw HSA funds to pay for non-medical expenses, you should plan to pay ordinary income taxes.

Evaluating a Health Savings Account (HSA) can inspire you to reflect on your own financial goals, and how a Health Savings Account does, or does not, support your goals.

Health Savings Accounts: Personalizing Your Finances

Framing your financial decisions around your family, lifestyle, or career goals can help you evaluate your options based upon what’s most important to you over the long term.

Your goals can inform whether you should take an action (or not). Understanding the tradeoffs of your set of decisions can help you evaluate how a decision takes you closer to your goals, or away from them.

When you can accurately understand the benefits and drawbacks of your investments and the type of account you plan to hold those investments in, you’ll be better prepared to make personalized decisions.

Read on to explore additional key facts and considerations about Health Savings Accounts.

Qualified Medical Expenses

Understanding what you can use your HSA funds for is critical for your planning and ongoing monitoring.

In the context of a health savings account, qualified medical expenses mean expenses paid by you (the HSA owner) for your medical care, or that of your spouse or dependent. Further, only those expenses that are not compensated for by insurance (or otherwise) apply.

While there are exceptions, insurance premiums are not generally considered qualified medical expenses in the context of your health savings account.

Nonqualified Expenses

If you use your health savings account funds to pay for nonqualified expenses, and you are not age 65 or older, then you should plan on paying an additional 20% penalty on the amount withdrawn. These types of withdrawals will also be treated as gross income.

The 20% penalty is waived in cases of disability or death and if you age 65 and older.

Let’s dive a little deeper so you can better understand how a health savings account can move you closer to your financial goal or distract you from what you’re really trying to achieve.

Your Eligibility Requirements Checklist for Opening and Funding a Health Savings Account

To open and fund a Health Savings Account (HSA), you need to meet several requirements[1]:

- Enroll in a High-Deductible Health Plan (HDHP): You must be covered under a qualifying HDHP, which meets the minimum deductible and maximum out-of-pocket threshold for the year.

- No Other Health Coverage: You cannot be covered by any other health plan, such as a spouse’s plan, Medicare, or TRICARE.

- No Disqualifying Alternative Medical Savings Accounts: You cannot have a flexible spending account (FSA) or Health Reimbursement Account (HRA) that disqualifies you from contributing to an HSA. Of note, you can have a limited-purpose FSA or post-deductible FSA.[2]

Once you meet these requirements, you can open an HSA through your employer (if they offer one) or directly with an HSA provider like a bank or financial institution.

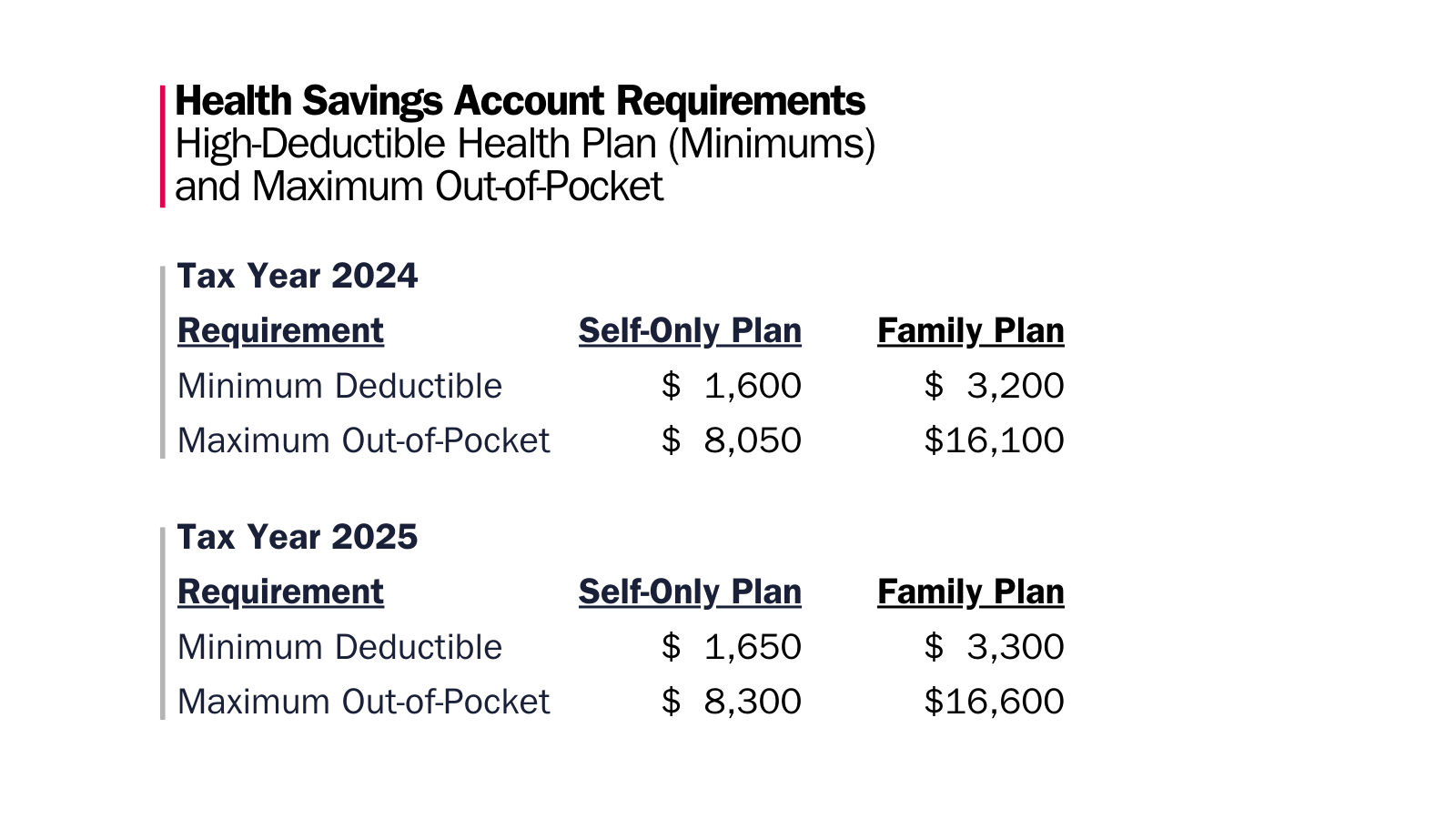

High Deductible Health Plan and Out of Pocket Maximums

To be HSA qualified, a health plan’s annual deductible for self-only coverage must be at least $1,600 in 2024 and $1,650 in 2025.

For family plan coverage, the minimum deductible is $3,200 in 2024 and $3,300 in 2025.

In 2024, the out-of-pocket maximums are $8,050 and $16,100 for self-only and family plans, respectively.

Those out-of-pocket figures tick up slightly for 2025 to $8,300 and $16,600 for self-only and family plans, respectively.

When considering a Health Savings Account, one practical adjustment you’ll want to evaluate is increasing your emergency fund.

Specifically, you’ll want to consider having enough emergency fund savings to be able to pay the full deductible on your HSA-eligible, high-deductible health plan.

Contributions and Contribution Limits

You can fund your HSA through direct deposits, payroll deductions (if offered by your employer), or by making contributions directly to the HSA provider.

Contributions to an HSA made by an individual are tax-deductible. This means that the money you contribute to your HSA can be deducted from your taxable income, which can lower your tax bill.

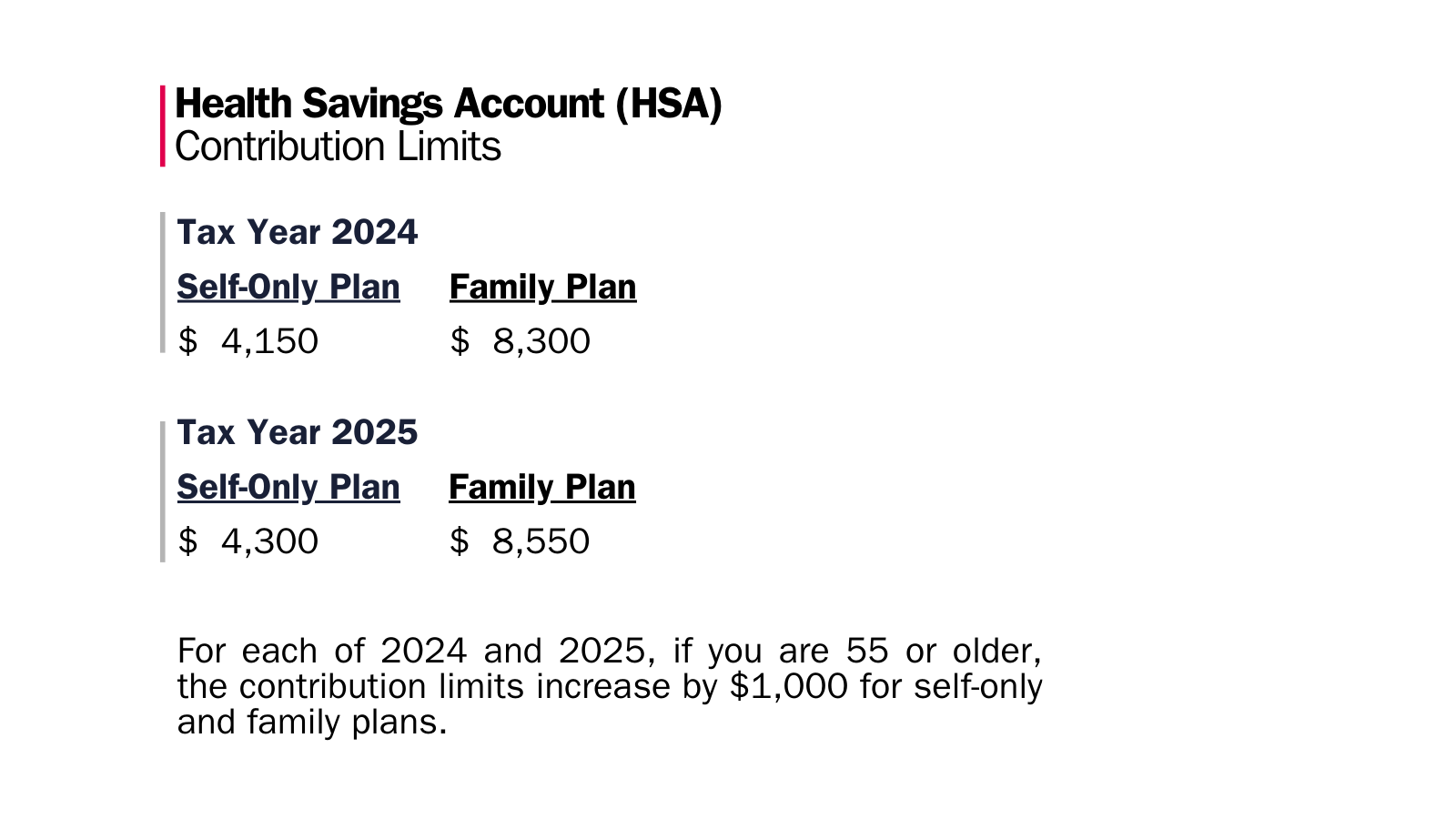

In 2024, the HSA maximum contribution limits are $4,150 for individual/self-only coverage and $8,300 for family coverage. For 2025, individual/self-only coverage contribution limit is $4,300 and $8,550 for a family plan.

Further, if you are age 55 or older, those 2024 and 2025 limits increase by an additional $1,000.

The contribution limits for a health savings account are generally higher than those for other types of tax-advantaged accounts, such as flexible spending accounts (FSAs).

Be aware from a tax planning perspective, if you contribute more than the annual limit to your HSA, the excess contributions will be taxed as ordinary income and incur a excise/penalty tax of 6%.

Looking at the calendar, you can make your HSA contributions at any time during a calendar year and until the federal income tax return filing date (without extensions), normally April 15 of the following year. And so, you have over 15 months to make your HSA contributions for a particular tax year.

This can be helpful to factor into your planning if you receive a substantial year-end or quarterly bonus in the early few months of any given year.

Understanding Contribution Limits and Uses for Married Couples

Health savings accounts are individual accounts.

And so, for married couples who combine their finances, there is not currently a joint HSA.

Your spouse may use either their own or your health savings account for reimbursement of their qualified medical expenses.

If you and your spouse are both HSA-eligible, and at least one of you is covered by a family coverage HSA-qualified HDHP, then the maximum amount you can collectively contribute to your HSA(s) is the family coverage annual limit for that year.

Employer Contribution Matching

Your employer might encourage you to save in your Health Savings Account by using an HSA matching contribution feature. This could function similarly to your 401(k) plan with employer match feature.

For example, your employer might match 50% of your HSA contributions up to a certain percentage of your compensation. Or your employer might match your HSA contributions up to a pre-determined dollar amount.

And so, if you have a goal to fund your HSA, and your employer has an HSA contribution matching feature, you’ll want to know how much you can contribute so that you achieve your funding goal and maximum employer contribution.

At a practical level, your employer’s HSA contributions count toward your annual contribution limit, are not tax deductible, and do not count as taxable income to you.

Investment Considerations

An HSA can have both a cash-like savings component, such a money market fund, and an investment component. HSA funds may hold investments “approved for IRAs (e.g., bank accounts, annuities, certificates of deposit, stocks, mutual funds, or bonds).

HSAs may not invest in life insurance contracts, or in collectibles (e.g., any work of art, antique, metal, gem, stamp, coin, alcoholic beverage, or other tangible personal property specified in IRS guidance.” [3]

One way to approach investing your HSA funds is to hold, at a minimum, the amount equal to your annual deductible in more liquid investment choices, like cash or a money market fund. Consider this part of your overall emergency fund, even if it’s spread across multiple accounts.

If you have an HSA balance greater than your annual deductible, you could evaluate what the right mix of longer-term investments align with your retirement needs. HSAs can provide you with the ability to invest for the long-term using low-cost ETFs and/or mutual funds.

Currently, HSAs are offering relatively low annual yields on cash holdings. The Consumer Financial Protections Bureau (CFPB) published a report in May of 2024 looking at recent trends for Health Savings Accounts.[4]

The CFPB report cited yields of less than 1% from a variety of leading HSA providers. The report footnotes that the research was conducted in 2023.

A recent scan in December 2024 of nearly a dozen HSA providers showed that many required a variety of minimum balances – ranging from $10,000 to $50,000 – to earn that provider’s highest interest rate – which ranged from 0.01% to 0.40% – on cash deposits. These figures are a snapshot in time and will change as benchmark interest rates adjust over time.

With any investment, make the time to understand the rules and restrictions that will apply over the lifecycle of the investment. As a long-term investor, it’s not enough to only research how to “get into” an investment.

As you evaluate Health Savings Account providers, consider working with providers that do not charge high fees, that do offer low-cost investments, and do have investment options that align with your HSA savings goals.

Your goals should guide your decisions. An investment or account type should align with and support your goals. Not the other way around.

Provider Fees and Expenses

The aforementioned CFPB report surfaced several practical elements you can factor into your HSA planning.

Monthly account maintenance and paper statement fees are two common types of fees to review in your HSA. The CFPB report cited figures that, when annualized, totaled around $48 per year. Over time, these fees reduce your investment returns if you are the one paying them.

If your HSA charges fees, does your employer pay it? Or is the fee reducing your account balance each month?

If you change employers and keep your former employer’s HSA, you might start being charged those maintenance fees your former employer previously paid.

The CFPB report also noted transfer fees and account closure fees, a common practice for many investment accounts. $25 was a commonly cited figure in the report.

The takeaway here is to understand the all-in cost of investing in an HSA when you’re evaluating your HSA provider options. Evaluating providers in this way is worthwhile even if your employer requires you to use a specific HSA provider for your payroll deductions or employer contributions.

Portability and Rollovers

Health Savings Accounts (HSA) are portable. Unlike employer-sponsored health insurance plans, which are tied to your job, an HSA belongs to you and stays with you even if you change jobs or retire.

This means that you can continue to use your HSA to pay for qualifying medical expenses even if you leave your current job.

Health Savings Account rollovers are allowed. Whether you are looking to simplify your finances and consolidate accounts, benefit from lower HSA costs, or a better set of investment choices, you are allowed to roll your HSA funds into a new account at a different provider. An HSA rollover contribution is not included in your income, is not deductible, and does not reduce your contribution limit.

HSA account holders can make one rollover from one HSA to another HSA during a one-year period.

Keep in mind that not every HSA provider will allow you to transfer your HSA investments to in-kind.

Health Savings Account funds don’t have an expiration date. Any money left in your HSA at the end of the year rolls over to the next year, so you don’t have to worry about losing it.

Situations Where a Health Savings Account Might Not Be a Good Fit

- You Plan to Need the Funds for Nonqualified Expenses before age 65: If you are earmarking your HSA to fund anything other than qualified medical expenses before you are 65 or older, an HSA might not be the right fit for your goals. Specifically, if you use HSA funds for anything other than qualified medical expenses, those withdrawals will be taxed as ordinary income and incur any additional 20% penalty tax.

- You don’t have an HDHP: In order to be eligible to contribute to a Health Savings Account, you must be enrolled in an HDHP. If you have a traditional health insurance plan with a low deductible, you won’t be able to contribute to an HSA.

- You have high medical expenses: If you have high medical expenses, an HDHP with a Health Savings Account may not be the best option for you. With an HDHP, you could potentially end up having to pay a higher deductible before your insurance coverage begins. If this happens, you’ll have to pay more out of pocket before your insurance starts covering your medical expenses.

- You don’t have the funds to contribute to a Health Savings Account: If you don’t have the extra funds to contribute to an HSA, it may not make sense to enroll in an HDHP. While HDHPs generally have lower monthly premiums compared to traditional health insurance plans, you’ll still need to be able to pay for your medical expenses until your deductible is met.

- You have other savings priorities: Whether you’re saving for a down payment for your dream home, contributing the maximum to your 401(k), or bolstering your emergency fund, for most of us, we only have a finite number of resources. Prioritizing what matters the most to you is what matters.

A Peculiar Planning Opportunity: The HSA Last Month Rule

If you are an HSA-eligible individual on the first day of the last month of your tax year, you are considered an HSA-eligible individual for the entire year. That’s December 1 for most folks. This holds true, even if you changed coverage during the year.

If you contribute to your HSA based on being an eligible individual for the entire year under the last-month rule, you must remain an eligible individual during the testing period.

Meaning, instead of spreading out your HSA contributions throughout the entire year, you condensed all your HSA contributions into the “last month” (up to the maximum contribution limit).

What is the Last-Month Rule Testing Period?

It begins with the last month of your tax year and ends on the last day of the 12th month following that month. As an example, such a time period could run from December 1, 2024 through December 31, 2025.

If you fail to maintain your HSA eligibility during this period, then you will owe a 10% penalty on your HSA contributions for the months that you were not covered by an HSA-qualified high-deductible health plan. Those contributions would also be included in your gross income.

Taking a Strategic View of Your Finances

Hopefully you found this overview of Health Savings Accounts helpful and educational.

Does funding your Health Savings Account in 2025 move you closer to your savings priorities? Does it mean you need to make some tradeoffs? If so, what’s the right mix of solutions for you or your family?

For example, if you fully fund your health savings account in 2025, are you able to continue to contribute the maximum amount to your 401(k) plan? Or does it mean you need to adjust your contributions so you can continue to receive a full employer matching contribution to your 401(k)?

If you have an HSA currently, here are some questions to consider throughout the next year:

- Have you verified that your contributions are accumulating in your HSA?

- How are you investing your HSA contributions to support your savings priorities?

- Are your investments low-cost, low-turnover funds, or are there other options you need to consider?

Reviewing your benefits, benefits usage, and aligning your benefits to support your goals should be a year-round process.

When you can take a more comprehensive view of your finances, you are better positioned to understand how you can work towards your savings priorities. It can also help you evaluate the tradeoffs of funding specific savings priorities relative to others.

The Next Step

Are you on track for your short-term goals, like making memories with your family by going on vacations together? How confidently are you approaching saving and investing for your long-term aspirations, like retiring or pursuing a meaningful second career?

We help busy parents and professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

[1] 26 U.S. Code I.R.C. § 223 – Health Savings accounts. Retrieved from https://uscode.house.gov/view.xhtml?req=granuleid:USC-prelim-title26-section223&num=0&edition=prelim. Accessed: December 3, 2024.

[2] Internal Revenue Service. (2004). Section 223 – Health Savings Accounts—Interaction with Other Health Arrangements. Retrieved from https://www.irs.gov/pub/irs-drop/rr-04-45.pdf. Accessed December 4, 2024.

[3] Internal Revenue Service. (2004). Health Savings Accounts—Additional Qs&As. Retrieved from https://www.irs.gov/irb/2004-33_IRB#NOT-2004-50. Accessed December 4, 2024.

[4] Consumer Financial Protection Bureau. Issue Spotlight: Health Savings Accounts (May 1, 2024). https://files.consumerfinance.gov/f/documents/cfpb_health-savings-account-issue-spotlight_2024-04.pdf. Accessed December 4, 2024.