Homeownership can offer families a lifetime of fun memories. The dream of owning a home, for many couples, becomes a reality through the support of a mortgage. The financial commitment of a mortgage can open the door to stability, security, and your “forever home”. While refinancing is a more familiar strategy, there’s never been a better time for hardworking homeowners to evaluate mortgage recasting. Read on to understand the benefits, drawbacks, and practical considerations of mortgage recasting.

Learning Points

Mortgage Recasting: Current Context

As a homeowner, you value making smart financial decisions that support your goals. As a long-term thinker, you want to understand how your decisions will look over a span of decades rather than months or years.

Your mortgage interest rate has a significant influence over your long-term planning. Your mortgage interest rate affects your family’s annual spending, tax planning, and long-term planning.

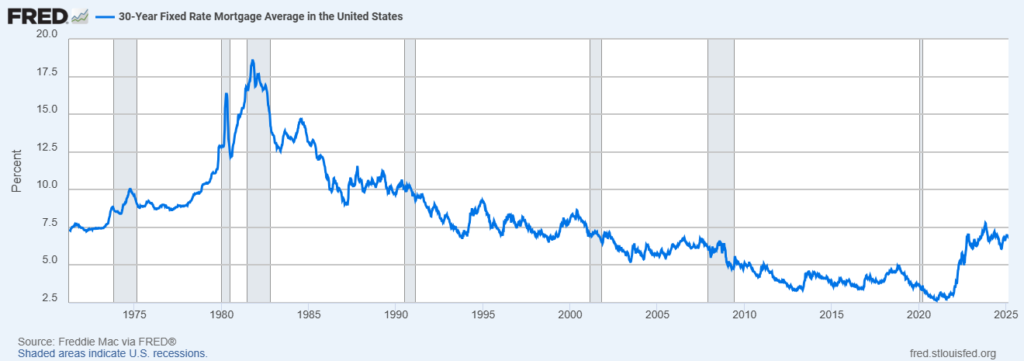

As of February 27, 2025, the average national mortgage interest rates were 5.94% [i] and 6.76% [ii] for 15- and 30-year mortgages in the United States, respectively.

Image Source: Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US, February 27, 2025.

Refinancing is a commonly discussed mortgage strategy when interest rates lower significantly. With mortgage interest rates originating between ~6.0% and ~7.2% since the beginning of 2024, refinancing might not currently be actionable for many homeowners.

There are multiple mortgage strategies that you can evaluate as your family’s needs change and interest rates adjust.

Given the current rate environment, what are some other mortgage strategies you can evaluate now without having to wait on interest rates?

Let’s explore one of the less familiar mortgage management strategies known as mortgage recasting.

Mortgage Recasting: An Overview

Mortgage recasting is the process where you make a one-time, lump-sum payment towards your mortgage’s principal balance.

During mortgage recasting, your mortgage lender keeps your original mortgage term and interest rate the same. Many mortgage lenders charge a fee for mortgage recasting. Once you pay your recast fee and follow the lender’s mortgage recasting application process, your mortgage lender then re-amortizes your loan.

Meaning, your mortgage lender recalculates a new monthly principal and interest payment based on the loan’s new, lower principal balance. Which means your monthly mortgage payments are now lower for the remainder of your mortgage.

The lower monthly payment due to re-amortization is a defining feature of mortgage recasting. Additionally, mortgage recasting could result in a lower amount of total interest you pay over the remaining life of your mortgage compared to your original mortgage.

Topics such as mortgage recasting, like so many others in financial planning, intersect with the world of tax. Make sure you coordinate with a qualified tax professional about your specific situation.

Now that you understand what mortgage recasting is, when might a homeowner like you want to evaluate mortgage recasting?

Mortgage Recasting: Illustrative Example

Mortgage recasting is an option to consider if you have a significant amount of extra cash and want to reduce your monthly mortgage expenses without the closing costs and paperwork of refinancing.

The following table shows how mortgage recasting lowers both the monthly payment as well as the total interest paid.

It also highlights that recasting does not change the term of your mortgage.

Mortgage Recasting

Illustrative Example

This table illustrates the hypothetical Original and Recast mortgage metrics after recasting a $50,000 principal payment.

| Original Loan | After Recast | Variance | |

|---|---|---|---|

| Principal Balance | $434,881 | $384,881 | ▼($50,000) |

| Monthly Payment | $2,626 | $2,324 | ▼($302) |

| Total Principal Paid 2 | $434,881 | $434,881 | – |

| Total Interest Paid | $431,724 | $382,086 | ▼($49,637) |

| Total Mortgage Payments | $866,604 | $816,967 | ▼($49,637) |

| Years Left in Mortgage | 27.5 | 27.5 | – |

| Payoff Date | Aug 2052 | Aug 2052 | – |

1 The original mortgage’s hypothetical first payment occurred on September 1, 2022. The hypothetical mortgage recasting occurs on March 1, 2025.

2 Assumes mortgage recast fee is paid in cash, and not added to mortgage principal balance.

For homeowners considering a recast, the extra principal payment could come from an inheritance, profitable investments, bonuses or life insurance proceeds.

There is also another situation where mortgage recasting could create a smoother landing on a new home purchase.

Recast Scenario: When You Want to Buy a House and Sell Your Existing Home

The dream of living in your “forever home”, for many couples, often becomes a reality through the support of a mortgage. Your home serves as the backdrop for a lifetime of memories. It can be a gathering place for your family to recharge while pursuing their dreams. Mortgage recasting can lower monthly payments and reduce total interest payments. It can also provide flexibility to secure your “forever home” in a tight housing market.

If you’re a homeowner facing the following scenario, it’s worth evaluating mortgage recasting:

If you are buying a house, and need to sell your current home, and feel comfortable not including a home sale contingency on your offer.

If you are successful with your home purchase offer, and your existing house doesn’t sell quickly, you might need a lower down payment for the new home.

In this scenario, you’ve closed on the house you want, but your mortgage payment is higher than what you are comfortable with long term.

Therefore, you’d look to further pay down principal once your existing home sells. In this situation, you could evaluate recasting your mortgage to lower your monthly payment that feels more comfortable to you. The money you save via a new, lower monthly mortgage payment could be saved or reinvested to support your other goals.

Mortgage Recasting Risks/Drawbacks

Total Interest Payments: After mortgage recasting, you will have a lower monthly mortgage payment relative to your original mortgage. You will also pay less in interest over the remainder of your home loan after mortgage recasting than if you did nothing to your original mortgage.

If you are sensitive to how much total interest you will pay over the life of your mortgage, a single, lump-sum principal payment there is another option to consider.

A single, lump-sum principal payment, ceteris paribus, results in less total interest paid over the remaining mortgage term than mortgage recasting.

Emergency Fund/Liquidity Considerations: Using a large sum of your money for mortgage recasting reduces your ability to cover immediate or short-term expenses.

Some homeowners will want to avoid depleting their emergency fund to execute this strategy.

Your home is a relatively more illiquid asset compared to the cash you have in a bank account.

If you have enough extra cash and you have a long-term goal of reducing the total interest you pay over the life of your loan, mortgage recasting and a lump-sum principal payment are worth evaluating.

Opportunity Cost: The money used for recasting could potentially be saved or invested in other ways that support your financial goals. This can feel more pronounced when a homeowner’s mortgage interest rate is far lower than current rates.

Long-term economic conditions, interest rate changes, and capital market outcomes are difficult to consistently and accurately forecast.

Evaluate Alternatives: There are other alternatives like mortgage refinancing and lump-sum principal payments are worth considering as tools in your mortgage management toolkit.

Not Always Available: Some lenders do not offer recasting, and certain loan types are ineligible.

A Note on Mortgage Recasting Fees

Mortgage recasting requires you to pay a fee. As of the time of this writing, mortgage recast fees ranged between $250 – $500.

Relative to current mortgage refinance costs, a recast fee is likely to be lower as of the time of this writing.

Each mortgage lender is going to have its own recasting process and requirements. We explore these generally below.

Create Your Mortgage Recasting Eligibility Checklist

If you’re considering recasting your mortgage, it’s a good idea to contact your lender to confirm your loan’s eligibility and understand any specific requirements they might have.

- Loan Eligibility: Generally, conventional loans – those not backed by the federal government – with terms of 15- to 30- years are eligible. Confirm with your mortgage lender that your loan is eligible. Loans backed by the federal government, such as Federal Housing Administration (FHA), VA loans, or USDA loans – backed by the United States Department of Agriculture – are typically not eligible for recasting.

- Minimum Principal Payment/Reduction Amount: Does your lender have a minimum principal amount they require you to pay in order to be eligible for mortgage recasting?

- Fees: Understand your mortgage lender’s recast process and fees. For example, the recasting process can take up to a certain number of days. Know their process and plan accordingly.

- Payment History: Your lender might also require you to have a loan in “good standing”. Validate payment history requirements. These could range from 12 to 24 months of on-time payments.

- Confirm what future restrictions your lender could apply to your loan after you recast. For example, does your lender allow you to recast your mortgage multiple times over the course of the loan?

Hypothetical Mortgage Recasting Timeline/Process

If you’re considering recasting your mortgage, and eligible for a recast, understand your mortgage lender’s timeline and process so you can prepare accordingly.

- Review and submit a completed recast request form and pay the recast fee.

- Make the related principal payment.

- Sign and return the recast agreement. This document should define all the details of your new re-amortized loan, including the effective date of your lower monthly mortgage payment.

- Your lender will re-amortize your mortgage loan according to your recast agreement.

- As of the effective date of your recast agreement, you will see your new monthly payment amount reflected.

Tax Planning

For homeowners who regularly claim the standard deduction on their taxes, a recast can improve your cash flow without sacrificing tax benefits

If you itemize your deductions, it’s a little less clear cut.

One approach is to calculate the marginal benefit. Meaning, how much of the itemized tax benefit will you miss via the lower annual mortgage interest? You could then compare that to lower mortgage payments.

Behavioral Finance Considerations: Cognitive Biases Affect Decision-Making

Loss Aversion: As a homeowner, it’s important to recognize that you could be overvaluing payment reduction (perceived as an immediate gain) versus potential portfolio growth (a relatively abstract and uncertain future gain).

Behavioral finance research shows that people tend to prefer avoiding losses over acquiring equivalent gains. The idea of parting with a large sum of money for mortgage recasting can be daunting, even if it leads to real future savings and aligns with your goals.

Depending on the specifics of your situation, you might prioritize mortgage interest reductions over the potential of higher-return investments over the long term.

Anchoring Effect: If you feel like you just missed out on the earlier, low-interest rate environment, you might be tempted to wait until those historically low interest rates return.

Mental Accounting: People often mentally separate their finances into different “accounts” (e.g., savings, mortgage payments). This can lead to a reluctance to use a lump sum for recasting, as it feels like a significant reduction in liquid assets. Understanding this bias can help homeowners make more rational decisions by focusing on the overall financial benefits.

The Next Step

Hopefully you found this overview of mortgage recasting helpful and educational.

Do any of these mortgage strategies move you closer to your savings priorities? Does it mean you need to make some tradeoffs? If so, what’s the right mix of solutions for you or your family?

You can review your household cashflow, mortgage debt, and evaluate potential alternatives that support your goals. It’s important to review and adjust to changes in your personal situation and the world around you.

Are you on track for your short-term goals, like making memories with your family by going on vacations together? How confidently are you approaching saving and investing for your long-term aspirations, like retiring or pursuing a meaningful second career?

We help busy parents and individual professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

[i] Freddie Mac, 15-Year Fixed Rate Mortgage Average in the United States [MORTGAGE15US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE15US, February 27, 2025.

[ii] Freddie Mac, 30-Year Fixed Rate Mortgage Average in the United States [MORTGAGE30US], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/MORTGAGE30US, February 27, 2025.