Taking control of your finances can feel incredibly empowering. If you’re a homeowner looking to keep more of your money working for you throughout the year, here’s one small adjustment to consider. Evaluate whether you can remove the escrow account requirement on your mortgage. Explore the potential benefits and drawbacks, as well as the practical approaches.

Learning Points

Overview: Removing Mortgage Escrow Account

If you’re a homeowner, property taxes and homeowners insurance are likely two significant annual expenses. Like many hardworking homeowners with a mortgage, you might be required to contribute a portion of these expenses in addition to your monthly mortgage payment.

Often, your mortgage company will hold your funds in an escrow account until the specific insurance and tax payments are due.

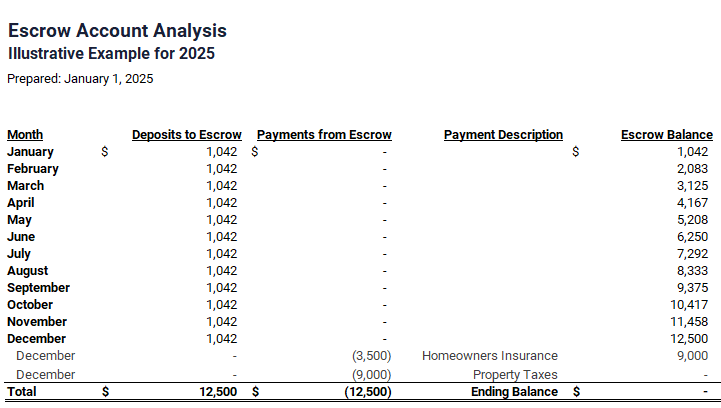

If this fits your situation, let’s briefly explore an illustrative example of how mortgage escrow account payments function currently. We’ll then look at how things change if you remove your mortgage escrow account.

For this illustrative example, we’ll use the following assumptions:

- Homeowners Insurance Payment: $3,500

- Homeowners Insurance Payment Due Date: 12/31/2025

- Property Tax Payment: $9,000

- Property Tax Payment Due Date: 12/31/2025

- Total Monthly Escrow Payment: $1,041.67

These dates and figures are intended to illustrate the timing of your escrow account cashflow.

While your specific due dates and expense amounts will likely vary from this illustrative example, hopefully this helps outline what the annual cycle looks like.

Next, let’s explore how this situation could look if the homeowner successfully removed their mortgage escrow account requirement.

Benefits of Removing Your Mortgage Escrow Account

Opportunity to Earn Interest on Planned Savings

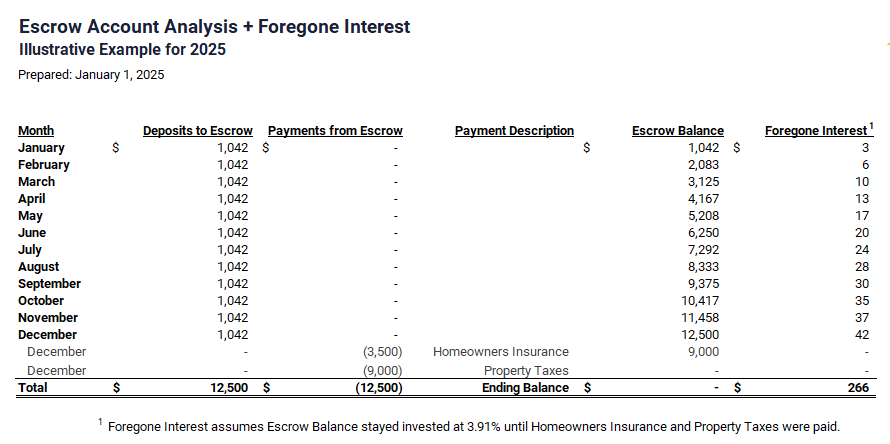

If you’re not earning interest in your mortgage escrow account, it’s worth exploring whether your loan is eligible to remove the mortgage escrow account.

By continuing to maintain your mortgage escrow account, and your is eligible to remove the requirement, you are missing the opportunity to earn interest on that money throughout the year.

Interest rates, and consequently, yields on fixed income, will adjust throughout the year. For this illustrative example, we use the same assumptions as before. Now, let’s also assume for simplicity that your cash could earn 3.91% interest throughout 2025. This is shown in the Foregone Interest column on the right of the original illustrative example.

Flexibility

If you’re not earning interest in your mortgage escrow account, it’s worth exploring whether your loan is eligible to remove the mortgage escrow account.

By continuing to maintain your mortgage escrow account, and your is eligible to remove the requirement, you are missing the opportunity to earn interest on that money throughout the year.

Thinking and Planning in Decades

If you’re in your 30’s or 40’s, your property taxes and homeowners insurance payments could continue for decades. Further, if/when you fully pay off your mortgage, you’ll likely continue to carry homeowners insurance and need to pay property taxes.

Removing your mortgage escrow account sooner rather than later creates the opportunity for you to earn interest for a longer time.

Using the figures from the illustrative example above, earning and re-investing $266 each year for over a decade can add up. It might even add up to a year’s worth of homeowners insurance.

Drawbacks of Removing Your Mortgage Escrow Account

Hassle Factor

There is a hassle factor associated with requesting your mortgage escrow account to be removed.

You’ll need to spend time establishing a new automatic savings approach.

There’s also the tracking and follow up relating to the removal request process. While these are not ongoing, or even annual events, they will require some amounts of your time. The current process’ inertia can be a powerful factor to stay the current course. To do nothing.

You’ll also spend time verifying that your new approach is working as intended.

Plan on spending time each year monitoring and adjusting your automated savings amount as your homeowners insurance and property tax bills change each year.

Late Payment Fee

If you miss a payment for your homeowners insurance or property taxes, you might also additional late payment fees.

Practical Perspectives and Timing

For homeowners looking for more direct management of their property taxes and insurance, exploring the removal of a mortgage escrow account could be a smart move.

Depending on your type of mortgage (e.g. conventional, VA, FHA, etc.), your lender has a process and team responsible for reviewing your mortgage escrow account requirements.

Start by contacting your mortgage’s customer service team for their specific process.

From a time and action perspective, this process could take between 1 to 3 mortgage payment cycles.

If your mortgage escrow account is successfully removed, verify the escrow account refunding process with your mortgage company.

You can automate saving for these expenses each month in your own interest earning account(s). If you’re looking for inspiration on how to automate this new slice of planned savings, here’s a quick read.

Create a plan now for how you’ll earmark your escrow account refund so don’t miss a beat after you automate saving for these future expenses.

As you consider this approach, it can help to understand how your mortgage lender evaluates whether your loan is eligible to remove the mortgage escrow account requirement.

Potential Escrow Account Removal Requirements

The following are potential requirements you must satisfy before a mortgage escrow account can be removed:

- Your loan has not been modified through a modification program where an escrow account is required.

- Payments are current and no payments have been 30 or more days past due in the last 12 months.

- You (the borrower) have not experienced a 60+ day delinquency in the 24 months immediately preceding the request to remove the escrow account.

- The Loan-To-Value ratio (LTV) is 80% or less. The LTV can be calculated by the formula (Unpaid Principal Balance/Original Appraised Value) x 100 = LTV).

- Flood insurance cannot be removed from the account if the loan originated with flood insurance or was modified with flood insurance on or after January 1, 2016, AND is held by a bank or federal savings association.

- If your loan is a Higher Priced Mortgage Loan (HPML) and originated between April 1, 2010, and May 31, 2013, the loan must be a minimum of 12 months old. Or, if your loan originated after June 1, 2013, the loan must be five or more years old.

- Your mortgage company has current evidence of your hazard insurance policy. As a reminder, hazard insurance is a subsection of your homeowner’s insurance.

- The escrow account must have a positive balance with no cash advances at the time of cancellation/removal.

- The existing escrow account for insurance cannot be based upon a previous event of non-payment and/or lapse in coverage.

- The existing escrow for taxes cannot be based upon a previous event of non-payment.

Hopefully the above list provides some context. Use this as a way of previewing what might influence the outcome of your request now and in the future. Your specific facts and circumstances will determine your loan’s eligibility.

The Background Story

Often, educational pieces like this one are the result of helping other folks research potential alternatives to their current situation. The origin story for this piece can be pinpointed to when I was reviewing an escrow account analysis statement that stated the following:

“Escrow is kind of like a savings account…we use that money to make your taxes and insurance payments…”

Dear Reader, this…this is the type of shenanigans that fuels the thoughtful, detailed work of financial planners for clients. It becomes a matter of principle.

While those squishy words are accurate – “kind of like” is doing some heavy lifting – they miss the mark in informing and educating the reader.

Specifically, this narrative fails to inform its audience that this “kind of like a savings account” pays no interest whatsoever.

Another way to frame this topic is as follows: removing your mortgage escrow account can allow you to stop indirectly giving your mortgage lender a substantial interest-free loan each year.

The Next Step

Hopefully you found this overview the mortgage escrow account helpful and educational.

Create your planned savings system that allows you to easily make these annual payments. For these known, short-term expenses, consider prioritizing holding these savings in liquid, low-volatility accounts or investments.

Depending on your specific situation and the yield curve, exploring certificates of deposit, money market mutual funds, or high-yield savings accounts are worth considering.

Consider adding “To Do” items on your calendar to pay for each of these expenses and for adjusting your savings amount for when these expenses change.

There are multiple mortgage strategies you can evaluate as your family’s needs change and interest rates adjust.

You can review your household cashflow, mortgage debt, and evaluate potential alternatives that support your goals. It’s important to review and adjust to changes in your personal situation and the world around you.

Taking A Strategic View of Your Finances

Are you on track for your short-term goals, like making memories with your family by going on vacations together? How confidently are you approaching saving and investing for your long-term aspirations, like retiring or pursuing a meaningful second career?

We help busy parents and individual professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner in Saint Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.