You work hard to build a bright future for your family. Ensuring your loved ones are cared for, even after you are gone, is a cornerstone of a long-term financial plan. Discover how your beneficiary designations can provide clear control of your assets. Learn why beneficiary designations are an essential element of your estate plan. Understand how they can protect your family, and what steps you can take today to ensure your estate plan reflects your intentions.

Learning Points

What is a Beneficiary Designation?

A will or trust can instruct your family, or estate, about how your assets will be distributed, creating a foundational component of an estate plan. While a will and trust can lay a strong foundation for your future, there’s another essential element: your beneficiary designations. Beneficiary designations are essential elements of an estate plan. You can use beneficiary designations to guide your family, or estate, as to how you want your assets transferred after your death.

A beneficiary designation is a legally binding instruction provided to a financial institution specifying who will receive a particular asset upon the account holder’s death. The beneficiary designation allows you to specify who receives your account’s assets after you are gone. A beneficiary can be an individual or entity that is entitled to the beneficial enjoyment of property under a legal arrangement such as a contract, trust, or will. When you designate, or name, a beneficiary on an account, you enter into a direct agreement with the financial institution holding that account.

Prioritizing your beneficiary designations matters. When you choose someone, or your trust, to be your account’s beneficiary, in most cases, that designation overrides any language you have in your will about the matter.

Read on to gain, or refresh, your working knowledge of beneficiary designations. You can apply this knowledge to your own life. Understand what gaps your accounts, or estate plan, have currently. Reaffirm how you are using beneficiary designations in your own estate planning.

Where to Start

Now that you understand what a beneficiary designation is, you can determine where it should exist in your financial life.

As a starting point, you can review the following account types to confirm who you’ve designated as a beneficiary:

- Employer Sponsored Retirement Accounts: your 401(k), 403(b), 457s and other profit-sharing plan accounts.

- Employer Sponsored Retirement Accounts: your 401(k), 403(b), 457s and other profit-sharing plan accounts.

- Investment Accounts: non-retirement brokerage accounts

- Life Insurance Policies: your term life, whole life, or universal life policies.

- Annuity Products: if you have a fixed annuity or variable annuity, for example.

- Other Employer-Sponsored Plans: company stock options, restricted stock units, deferred compensation, and defined benefit plans.

Additionally, you’ll want to review your bank accounts. Specifically for your bank accounts, a payable on death (POD) designation means your bank account automatically transfers to the named beneficiary upon the death of all account owners and co-owners.

For your non-retirement investment accounts, often referred to as “brokerage accounts”, you can designate a beneficiary or beneficiaries which establishes a transfer on death (TOD) registration for each account.

Here are common assets and the term for its non-probate transfer mechanism used to bypass probate:

Table: List of Common Assets and Their Transfer Mechanism

| Asset Type | Transfer Mechanism |

|---|---|

| Retirement Accounts (IRAs, 401(k)s, 403(b)s, Pensions) | Beneficiary Designation |

| Life Insurance Policies | Beneficiary Designation |

| Annuities | Beneficiary Designation |

| Other Employer-Sponsored Plans | Beneficiary Designation |

| Personal Property with Title Documents (in some jurisdictions) | Beneficiary Designation (where applicable) |

| Bank Accounts (e.g. Savings, Checking, CDs) | Payable on Death (POD) |

| Brokerage Accounts | Transfer on Death (TOD) |

| Vehicles (varies/state dependent) | Transfer on Death (TOD) |

Because this topic, like so many others in financial planning, intersects with the world of estate planning and tax, make sure you coordinate your actions with a qualified estate planning attorney and tax advisor.

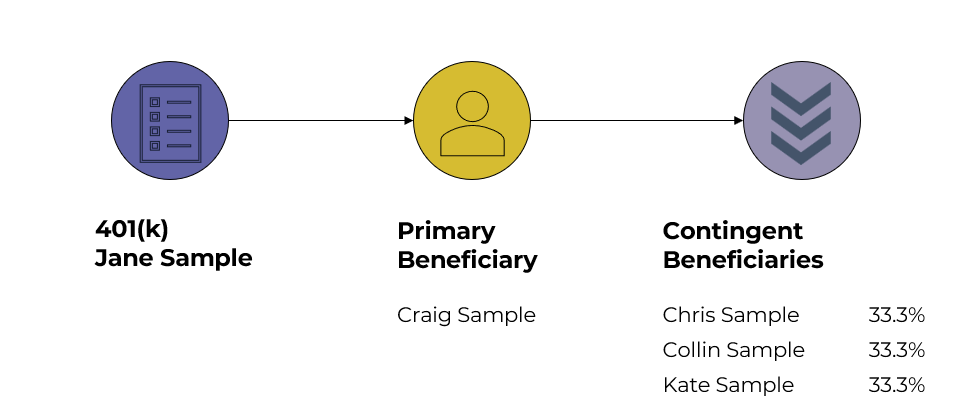

Primary Beneficiary and Contingent Beneficiary Designations

For each account you or your spouse own, a fundamental best practice is to designate both primary and contingent beneficiaries. In the context of a single account, the diagram below shows the relationship between a 401(k) account for ‘Jane Sample’, her husband ‘Craig Sample’ as the primary beneficiary and their three children as contingent beneficiaries.

Primary Beneficiary

Primary in this context means first. For a single asset, such as a 401(k) account, this role represents the first choice to receive the asset.

Your primary beneficiary is the person or entity you name in your last will and testament, account, or in your trust. Your primary beneficiary receives distributions from your trust first.

Contingent Beneficiary

Contingent in this context means all primary beneficiaries predecease the account holder, are unable to accept the inheritance, or decline it. This safeguard group prevents assets from going through probate if the primary beneficiary is unavailable. This role serves as an essential backup to the primary beneficiary.

In the context of an estate plan that includes a trust, the contingent beneficiary designation is:

The person, or entity, that you want to receive the trust (or estate) distribution, but only if the primary beneficiary, or primary beneficiaries, has passed away, is unable, or unwilling to accept the distribution.

A contingent beneficiary role is sometimes referred to in the following terms:

- remainder

- remainderman

- secondary

While you’re evaluating who you want to name as the beneficiary of a trust, or a single account, you are not limited to just a single beneficiary. You can have multiple primary beneficiaries and/or multiple contingent beneficiaries.

With few exceptions, if your account does not have a designated beneficiary, and you pass away, that portion of your estate will likely go through probate court.

Beneficiary Planning for Parents with Children and Grandchildren

As parents, you want to coordinate and align your beneficiary designations with your estate plan, including any trust(s).

If you have young children, especially kids under the age of majority in your home state, you should consider speaking with an estate planning attorney about whether a trust would help you achieve your estate planning goals.

Your trust can help you detail who controls your assets, how and when you want your money distributed to your children, as well as other provisions.

An estate planning attorney can help you and your spouse evaluate and memorialize how best to protect and thoughtfully distribute your assets according to your wishes.

If you had estate plan documents drafted before children, are the people you named originally, still the right ones now that you have children?

Too many people assume “Oh, yeah, I have those documents”. Yes, but if they are old and outdated the cost of getting current documents may prove far less of a cost and hassle than the problems created by outdated or inadequate documents.

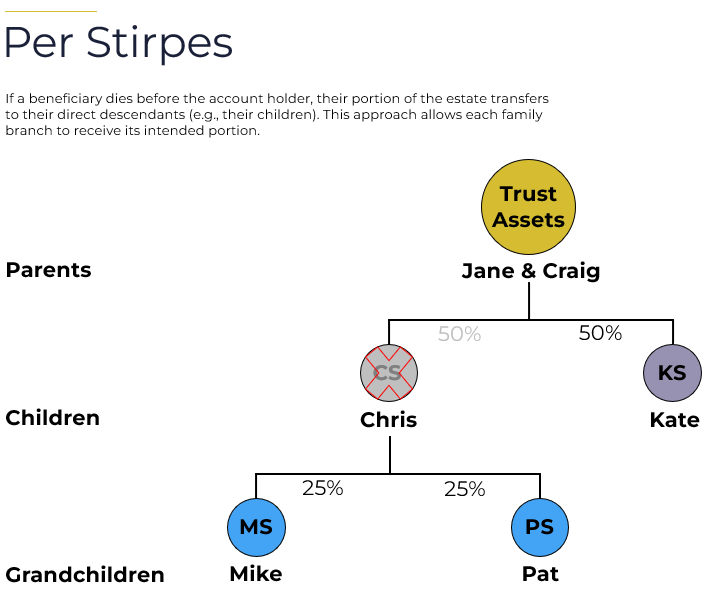

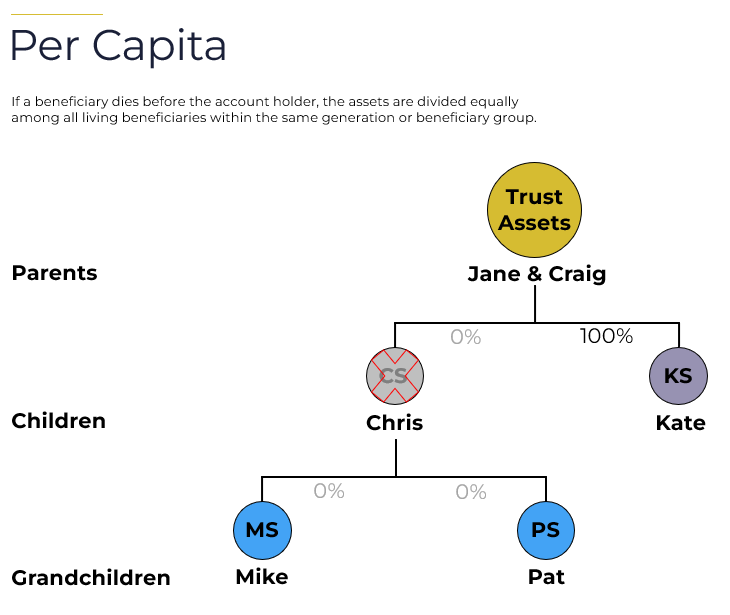

For multi-generational planning, understanding the distinction between “Per Stirpes” and “Per Capita” is essential. These two terms dictate how assets are distributed if a named beneficiary predeceases the holder. They are particularly useful when considering how children and grandchildren are, or are not, included in the transfer of an asset.

Let’s review what each of these terms mean.

Per Stirpes

Contingent in this context means all primary beneficiaries predecease the account holder, are unable to accept the inheritance, or decline it. This safeguard group prevents assets from going through probate if the primary beneficiary is unavailable. This role serves as an essential backup to the primary beneficiary.

Per Capita

If a beneficiary dies before the account holder, the assets are divided equally among all living beneficiaries within the same generation or beneficiary group. If a beneficiary dies, their portion of the assets is redistributed among the remaining beneficiaries, rather than being passed down to their descendants. This allows an inheritance to be redistributed among the remaining beneficiaries, rather than passing through to the beneficiary’s heirs.

If you select ‘per capita’ without a clear understanding of its application, you could set up a scenario where you disinherit a deceased child’s lineage. If this is an unintended outcome, it could potentially cause significant family discord and undermine the true spirit of your family legacy.

Common Misconceptions about Beneficiary Designations

While you’re considering beneficiary designations, knowing what a beneficiary is not allowed to do can also help guide your thinking.

Specifically, designating someone as a beneficiary does not give them any legal ownership rights, access, or control of your account while you are alive.

For instance, if you name your daughter as the beneficiary of your bank account, your daughter will not have access to that account simply because she is named as a beneficiary. You daughter would not have control of your bank account to withdraw money from the account. Nor would your daughter, as the designated beneficiary, be allowed to change the beneficiary designation(s) on that account.

In the context of your estate plan, if you named someone as the beneficiary, you are not obligated to share your full trust or will with them while you are living.

Life Moments: Reasons to Revisit/Update Estate Documents

As your life changes, your needs and wishes might change in ways that cause you to update your beneficiary designations or other parts of your estate plan. Here are some common reasons to review and/or update beneficiary designations, and other elements of your estate plan:

- Outdated estate plan. The documents drafted before children, or that you last reviewed ~5-7 years ago.

- Marriage or divorce.

- New child. Your account beneficiaries might not reflect all your children. Your estate plan might not adequately address a new child.

- Move to a new state. The plan that fits your family in your old state might not line up well in your new primary state of residence. Working with a qualified estate attorney in your new state to help review, revise or start anew could help reduce unintended issues later.

- Vacation homes or other assets held outside your primary state of residence.

Taking a Strategic View of Your Finances

We help busy parents and individual professionals like you explore tax-efficient gifting strategies and develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.