Life moves fast, and it’s easy for critical details to slip through the cracks. For busy parents and professionals, an outdated beneficiary designation could create unintended frictions. Learn why a proactive beneficiary review is time well-spent. Identify any potential gaps across all your accounts. Take the time now to avoid future complications and to ensure your wealth transfers smoothly and efficiently. A clear plan to take care of your loved ones if you’re not around is a critical element of your financial plan.

Learning Points

Why Your Beneficiary Review Matters

Beneficiary designations are essential elements of an estate plan. You can use beneficiary designations to guide your family, or estate, as to how you want your assets transferred after your death.

A beneficiary designation is a legally binding instruction provided to a financial institution specifying who will receive a particular asset upon the account holder’s death.

The beneficiary designation allows you to specify who receives your account’s assets after you are gone.

A beneficiary can be an individual or entity that is entitled to the beneficial enjoyment of property under a legal arrangement such as a contract, trust, or will. When you designate a beneficiary on an account, you enter into a direct agreement with the financial institution holding that account.

Prioritizing your beneficiary designations matters. When you choose someone, or your trust, to be your account’s beneficiary, in most cases, that designation overrides any language you have in your will about the matter.

Identifying Beneficiary Gaps

It might have been a while since you went through a complete account beneficiary review. Even the most organized among us can easily overlook, delay, or unknowingly skip this doublecheck.

Understand what beneficiary gaps exist across all your accounts and assets.

It can be challenging to keep track of all your designated beneficiaries. There is no national reporting mechanism. There is no centralized clearinghouse for you to aggregate all your accounts and designated beneficiaries. Your financial institution is unlikely to ask you to review and update your designated beneficiaries.

Like many busy parents, you might not have thought about reviewing your beneficiaries since you initially opened an account. It’s a helpful habit to conduct a beneficiary review as your finances, relationships or circumstances change (section link). You would not want an outdated family relationship or deceased loved one to remain the beneficiary of your account.

And so, if you haven’t reviewed all your account beneficiaries since the first Obama administration, let’s explore how you can identify any gaps in your beneficiary designations. Here’s one approach to getting organized.

Organizing Your Beneficiary Review

There’s never been a better time to review your beneficiary designations. Well, depending on when you’re reading this, the next rainy evening might be a better time to get organized.

Regardless, whether you have 3 or 30 accounts, a beneficiary review does take some time – at least initially.

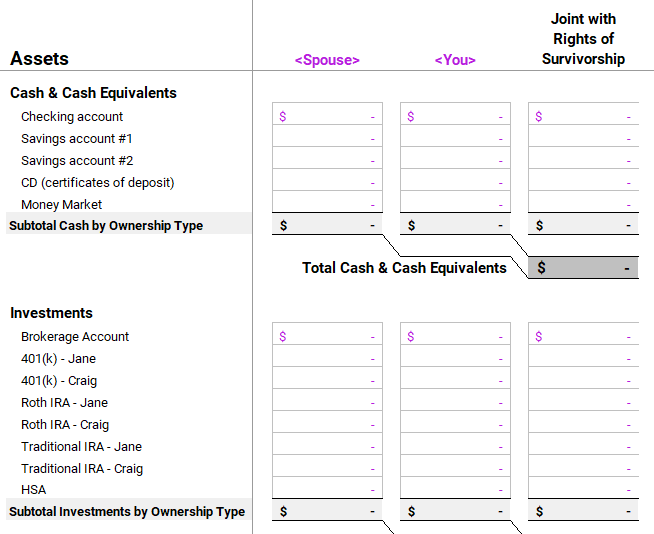

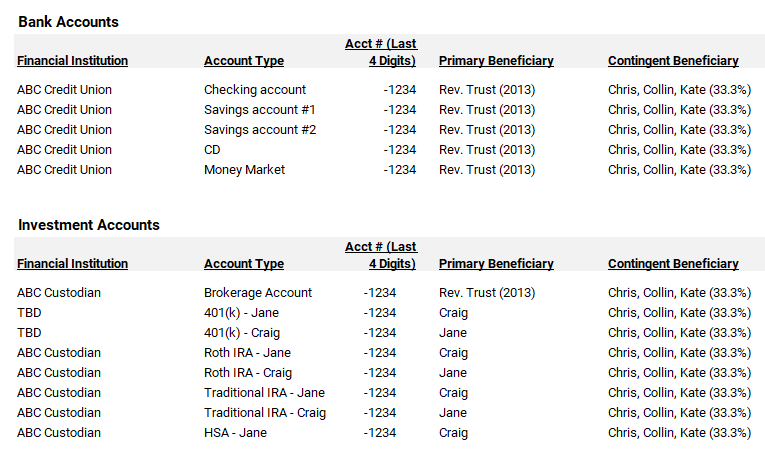

To start your beneficiary review, create an inventory of your accounts and their key details into a single document. Begin with all your accounts, insurance policies, and annuities listed on your personal net worth report.

If you don’t have a personal net worth statement, you can download your free, personal net worth and cash flow report template here.

During your beneficiary review, consider including details like those shown in the report template below. You might also consider including contact details such as their phone number, email address, mailing and address. Once you’ve consolidated these details, you can quickly reconcile and update your account inventory as your life changes.

For most long-term investors like you, the next beneficiary review becomes an easier to manage process after your initial review since you’re either adding/deleting accounts or updating beneficiaries.

And so, each time you update your estate planning documents, you’ll want to review a complete list of your accounts, policies, etc. where you should have a designated beneficiary.

This approach can help create clarity and understanding for you and your spouse the next time you walk through a beneficiary review.

Personal Cybersecurity Matters

After your beneficiary review, store your account inventory in a secure location. Strongly consider using multifactor protection and a unique password to protect this specific document. Consider storing the updated version as a physical copy alongside your estate documents. Securely dispose of the old physical copy. While you’re thinking about security, here’s a simple personal cybersecurity checklist:

The Next Step

If you died, how would your assets transfer to your loved ones?

A clear plan to take care of your loved ones after your death is a critical element of your financial plan. Your estate plan can specify how your assets, such as your home, investments, or life insurance, will be passed on to your loved ones after you are gone.

When you take the time to review and update essential estate planning elements, like account titling and beneficiary designations, you can make sure your loved ones are taken care of later.

If you do not have a trust, a will, or designated beneficiaries, then the laws of your state, also known as intestacy laws, will most likely govern the distribution of your estate.

Beyond the time requirement and knowing where to start, taking concrete action on your estate planning can be psychologically challenging.

Contemplating our own mortality, and what it means for those we love, can be a productive exercise when we know where to channel our energy and resources.

Your account inventory, or personal net worth report, can serve as a valuable reference point when you are considering updates to your estate plan or when your family relationships evolve. Your up-to-date account inventory can guide your spouse if you are no longer around.

So, review your personal net worth report and confirm whether each of your accounts has the proper beneficiary designation. If you come across an account and you’re unsure who the beneficiary should be, consider reviewing your instructions for funding and titling your trust.

Taking a Strategic View of Your Finances

We help busy parents and individual professionals like you explore tax-efficient gifting strategies and develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.