You’ve built a life in your home filled with memories, milestones, and meaning. But when was the last time you checked if your homeowners insurance still fits your family’s reality? With rising costs and changing risks, this article helps you take a fresh, informed look at your coverage. Discover how small updates can make a big difference in protecting your home and your future.

Learning Points

Prioritizing Your Homeowners Insurance Review

When was the last time you truly reviewed your insurance coverage options? It’s easy to put off, and it probably wasn’t a priority when you were closing on the home your family is living in today.

For homeowners like you, it may feel like insurance costs continue to represent a larger portion of your family’s budget each year. While individual homeowners are likely to experience a variety of premium changes, broadly speaking it’s not just your imagination.

For some data driven context, S&P Global Mark Intelligence found that homeowners insurance rates have increased throughout the country between 2019 and 2024. In Missouri and Illinois, for example, homeowners insurance effective rates have cumulatively increased 43.7% and 59.7% between 2019 and 2024, respectively [i].

There are a variety of drivers for rising homeowners insurance premiums, increasing property values, inflation (driven by the rising costs of building materials and labor), as well as claims payouts.

So, let’s connect how these cost drivers for insurance premiums are relevant to you, as an individual homeowner.

If property values are increasing due to inflation from rising building costs, you want to know whether you need to update your dwelling limit on your homeowners insurance.

If inflation and/or tariffs are driving appliance cost increases, understand whether your personal property limit sufficiently covers all the contents of your home, especially expensive or hard-to-replace items.

Reviewing your homeowners insurance policy can help you build a strong foundation for your personal finances. It can keep you and your family protected from financial loss when tailored to your life.

The Role of Homeowners Insurance

Whether you’re in your starter home, forever home, or somewhere in between, and you have a mortgage, chances are you have a homeowners insurance policy.

Homeowners insurance protects your family from the loss of or damage to your home and personal property. It can provide relief from personal liability for injuries to others, or their property, while they are on your property.

Your homeowners insurance should cover your home, other structures on your property, and your personal property (belongings). Your homeowners coverage amounts should be informed by how much it would cost to rebuild your home in a total loss scenario.

For example, if your home was destroyed by a tornado or home fire, how much would a builder charge your to rebuild your home?

The amount of your coverage should not include the value of the land though.

As a homeowner, you’ve probably heard the same generic approach to purchasing homeowners insurance. It goes something like this, “Get several written quotes. Compare the annual cost and coverage limits. Evaluate premium amount depending on your deductible options.”

The above approach is a good starting point. However, it doesn’t provide you with much of a framework for what you’re comparing and what to consider in your evaluation.

Understand the choices you have available to adjust your homeowners insurance coverages to fit your current needs and lifestyle.

Align your premium and deductibles with your current savings goals and personal risks you could encounter over the next year. Read on to understand the different elements of your homeowners insurance policy, key terms, and questions to ask your insurance company.

With school back in session, there has never been a better time for reviewing your homeowners insurance policy with your spouse.

Take the time now to think critically about whether you have the right homeowner insurance coverages in place for you and your family. Sleep better knowing you understand the risks and costs.

Take the next step and explore this educational article on how you can review your homeowners insurance using actionable approaches.

Coverage Types

As a homeowner evaluating new and existing homeowners insurance policies, it’s helpful to start with the following framework:

- What you are insuring (e.g. your house, other structures, and their contents).

- What you are insuring against (e.g. fire).

- The total estimated dollar value of the real and personal property you are insuring.

- The amount of coverage each set of policies provides.

The following overview is intended to provide homeowners with an educational framework during their homeowners insurance policy review. Each insurance company will have its own set of policy forms, potentially with varying exclusions, terms and conditions.

HO-2: Broad Form

This covers the dwelling and personal property from only the specifically named perils listed in the policy.

Currently, HO-2 coverage usually names around sixteen specific perils that the policy DOES cover:

| Fire or lightning | Windstorm or hail | Explosion | Riot or civil commotion |

| Damage by aircraft | Damage by vehicles | Smoke | Vandalism or malicious mischief |

| Theft | Falling objects | Weight of ice, snow, or sleet | Volcanic eruption |

| Sudden and accidental tearing apart, cracking, burning, or bulging of built-in systems | Freezing of plumbing, heating, or AC systems | Sudden and accidental damage from artificially generated electrical current | Accidental discharge or overflow of water or steam |

HO-3: Special Form

This policy is different from the HO-2 policy in the way it approaches perils for your real property.

Specifically, the HO-3 policy provides open perils coverage for your dwelling. Meaning, unless the policy specifically excludes a peril, all other perils are covered.

In HO-3 policies, common exclusions include the following:

| Earth movement (e.g., earthquakes, landslides) | Flooding and water backup | Neglect or lack of maintenance | War or nuclear hazard |

| Intentional loss | Government action | Mold, fungus, or wet rot (unless caused by a covered peril) | Wear and tear |

| Mechanical breakdown | Smog, rust or corrosion | Pollutant discharge or seepage | Settling, shrinking, bulging, or expanding of structure |

| Damage from birds, vermin, rodents, or insects | Damage from animals owned by insured |

However, the HO-3 policy, like the HO-2, generally covers personal property from only those sixteen specifically named perils listed in the policy.

HO-5: Comprehensive Form

This policy provides open perils coverage for your dwelling and personal property. Meaning, unless the policy specifically excludes a peril – like those shown in the table above – all other perils are covered.

When you review your homeowners insurance policy, notice how it is structured. It isn’t a single policy.

It is a package of policy forms, each addressing different situations and amounts of coverage for your real property and personal property.

Coverages and Property

As you start to assess which policy form best fits your personal situation, you’ll want to organize the quantitative elements that best balance risk and cost.

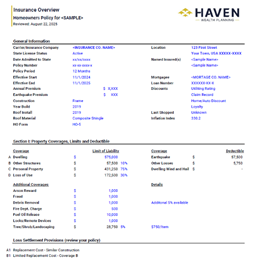

Let’s walk through the different elements of your declarations page.

You can use this framework to organize the costs and benefits of each set of policies. Like any contract, you need to understand the details and definitions used for each element noted on your declarations page.

Section I

This outlines the coverage limits – the amount you will be paid for a covered claim.

A: Dwelling: for the residence listed in the declarations page, and attached structures like a garage, deck, or fences.

B: Other Structures: for structures not attached to your dwelling, like your detached garage. If your structure is used for business purposes, there is generally no coverage under your homeowners insurance policy.

C: Personal Property: Your policy will limit certain types/classes of property. You’ll want to pay particular attention to these sublimits because they cover common high-value items regularly kept at home.

D: Loss of Use: provides benefits for you to live elsewhere while the portion of your home that you normally live in is repaired or rebuilt.

As you evaluate your policy, here are some Section I questions to consider with your insurance contact(s):

- Can you help me estimate what it would cost to repair or rebuild my home if it were damaged or destroyed?

- Will the coverage limits for my home or personal property automatically increase over time with inflation? If not, what do I need to do to make sure my home is insured for the right amount?

- What is NOT covered by this policy?

Deductibles

This is the portion of the insurance claim you are responsible for. Many homeowners insurance policies will have specific deductibles for specific types of losses. Increasingly these deductibles are quoted on a percentage basis relative to the total dwelling limit of liability.

For example, if your dwelling liability limit is $575,000, you might see an earthquake endorsement deductible of 10%, or $57,500.

Let’s connect this concept back to actionable information.

As you think about your own financial plan, if your home suffered a total loss from a high-deductible peril, would you have enough cash on hand to cover the deductible?

Your financial planner should be able to discuss how you can keep that portion of your emergency cash available, but also working against the effects of inflation, fees, and taxes.

Section II

This details the coverage limits for the following:

E: Personal Liability

F: Medical Payments to Others

Loss Settlement Provisions

Describe how an insurance company will reimburse you for personal property losses: actual cash value or replacement cost value. Here is an educational piece that highlights the importance of these critical provisions.

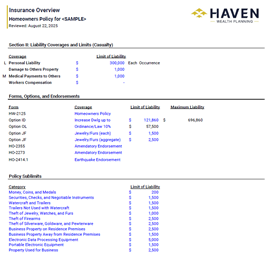

Forms, Options, and Endorsements

These modify Section I and Section II. Not every homeowners insurance policy includes each of these coverages. They can be added, at additional cost to you, the insured. Your policy will provide details about all the available forms, options and endorsements available to you.

Back-Up of Sewer or Drain

As you’re evaluating your home insurance coverage, consider an easily overlooked scenario.

You’re on family vacation when a storm with damaging winds and heavy rain knocks out power at your house. The ground is saturated, and your sump pump fails due to the lack of power.

How much will it cost you to repair, restore, or replace all the water damaged personal property and building materials in your finished basement?

If paying for a fully damaged basement due to a sump pump failure doesn’t let you sleep well at night, you could consider installing a battery-powered sump pump and/or adding a backup sewer endorsement to your homeowner’s policy. Depending on your insurance policy, this endorsement could provide protection in the event of a water backup in the basement through the storm drain or sump pump.

Under some policies, this endorsement covers the costs of restoration, construction repairs and replacement.

Earthquake Coverage

Another common endorsement for Missouri homeowners is earthquake insurance. According to the Missouri Department of Insurance, “Missouri is the third largest market for earthquake insurance…exceeded only by California and Washington.” [ii]

When you start reviewing insurance policies, one key consideration for evaluating your earthquake endorsement options is the deductible. Depending on your policy, you could need to plan on a deductible ranging between 10% – 20% of the coverage limit.

For example, if your dwelling coverage limit is $600,000 and you have a 20% deductible, your deductible amount would be $120,000.

The details of this coverage are critical. Not every earthquake endorsement covers brick veneer or solid masonry construction. Understanding how your own home is constructed can guide you to the right insurance solutions.

Ordinance or Law

This option pays the extra cost to rebuild your home to meet new or updated building codes or ordinances that did not exist when your home was first built. It is also called building code upgrade coverage. You’ll want to understand this specific option’s deductible.

Umbrella Liability Insurance

The primary benefit of an umbrella policy is increased liability coverage. An umbrella policy can provide additional liability coverage beyond what your regular insurance policies, such as your auto or homeowners insurance, already provide.

Key Terms

Actual Cash Value (ACV). The value of your home or personal property considering its age and wear and tear and resulting depreciation. This method will generally be a lower amount compared to the cost of a brand-new item. This method does not consider qualitative factors such as how little used or well-kept your personal property was prior to the loss. This replacement cost method pays for your loss but often does not pay enough to fully replace or repair the damage.

Replacement Cost (RC). The cost to rebuild your home or repair damages using materials of a like kind and quality. This refers to how much it costs to repair or replace the lost personal property with an exact or functionally similar, but new, item. This is different from your home’s market value, which includes the price of land and depends on the real estate market.

Premium: The amount you pay your insurance company for the insurance coverage.

Deductible. The amount of money you are required to pay out-of-pocket on a claim before the policy pays the loss. Deductibles can be a dollar amount, or a percentage. Your declarations page may identify the deductibles on your policy.

Depreciation. The decrease in home or property value due to its age, wear, and tear.

Exclusion. These eliminate coverage for certain losses or personal property. For example, common exclusions include damage from floods and earthquakes. These are potentially covered by a separate Flood, or Earthquake policy

Limits. The maximum amount an insurance company will pay if/when an insured event occurs.

Peril. The cause of a loss such as wind, fire, and theft.

Personal Liability Protection. This covers you, and all your family members living with you, from financial loss if someone makes a claim, or files a lawsuit against you, and you are legally responsible for bodily injuries or damage to someone else’s property for which you are negligent.

If you come across an insurance term that you don’t have a solid grasp of, you can reference the National Association of Insurance Commissioners’ glossary of commonly used terms and definitions. This resource can help orient you to the term’s general meaning. Your specific homeowners insurance policy will also have defined terms that you should understand.

Practical Considerations

Preparing to Get Quotes

If you plan to get multiple quotes from other insurance companies, you can prepare to share specific details about who and what you want to insure.

It’s common for an insurance company to request details about your current insurance on the property, as well as any primary or secondary mortgages.

The insurance company will also need to know specific finishes/materials of each room as well as age and quantities of systems (e.g. HVAC, plumbing, electrical, etc.) information about your home.

For example, how old is your stove? What is the approximate age of your current roof?

Insurance companies also evaluate safety factors, like how close you live to the nearest fire department and fire hydrant(s). Plan to share details about protective systems/devices installed on the property. Details like the type of security system, how old your dual carbon monoxide/smoke alarm is, or how many dead bolt locks are installed.

You’ll also need to provide approximate (or appraised) values of your personal property.

For example, if you have firearms, jewelry, artwork, collectibles, or antiques, you’ll want their values accurately reflected in your policy quote’s respective sublimit.

You can save some time by keeping a master list of these details somewhere handy and then copy/pasting the information into each insurance company’s specific form or portal.

Have you completed any renovations or additions? Have you purchased any items like jewelry, firearms, or antiques that exceed your personal property sublimits? When you are contemplating significant changes to your living space or personal property, make sure understand the downstream insurance costs associated with protecting your new space or stuff.

Discounts

Explore whether your insurance company has discounts available for:

- Bundling multiple vehicles

- Bundling multiple lines of insurance (e.g. home, auto, and umbrella).

- Operating vehicles with safety features like air bags, anti-lock brakes, and lane departure systems.

- Accident-free driving

Understanding Which Insurance Companies Offer Homeowners Insurance Near You

If you’re curious which insurance companies offer policies in your home state, one place to start is to review your state’s insurance commission website.

For example, the Missouri Department of Insurance offers a variety of consumer-oriented resources you can use to better understand your insurance options for homeowners insurance policies.

Homeowners Insurance Quotes and Credit Scores

In those states that allow insurance companies to use credit-based insurance scores when determining insurance rates, the soft inquiry doesn’t affect your credit score.

In the state of Missouri, an insurer may use a credit report or insurance credit score as a factor in underwriting your policy.[iii]

Declarations Page: Summarizing Your Homeowners Insurance Policy

You can recreate your own declarations page to help you quantitatively evaluate your current policy. Use it to compare against policy adjustments (i.e. increased deductible or additional endorsements).

Or use it compare against homeowners insurance quotes from other insurance companies.

As a starting point, here is one approach to organizing your policy details:

If you’re interested in the underlying Excel template, please feel free to reach out to us at info (at sign) havenwp (dot) com.

A Long-Term Approach to Your Family’s Goals

Hopefully you found this overview of homeowners insurance helpful and educational.

In addition to homeowners insurance, we help professionals and families like you understand whether fully funding your 401(k), gifting the maximum annual exclusion amount to your child’s 529, contributing to your dependent care FSA, increasing your emergency fund, or some combination of these and other savings priorities aligns with your goals and values.

When you’re comfortable that you’re minimizing your taxes, your living expenses are dialed in and aligned with your values, it becomes easier to save the right amounts toward your future goals/savings priorities.

Taking a Strategic View of Your Finances

If you’d rather not dedicate your few, precious free evenings to reviewing your insurance policy coverage, you could instead partner with a financial planner.

We help busy parents and professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

[i] Woleben, Jason. “US Homeowners Rates Rise by Double Digits for 2nd Straight Year in 2024.” S&P Global Market Intelligence, January 21, 2025. https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/1/us-homeowners-rates-rise-by-double-digits-for-2nd-straight-year-in-2024-87061085 Accessed August 21, 2025.

[ii] “Earthquake Insurance | Missouri Department of Insurance.” Insurance.mo.gov. https://insurance.mo.gov/earthquake-insurance Accessed August 22, 2025.

[iii] Missouri Revised Statutes, Mo. Rev. Stat. § 375.918 (2025). https://www.revisor.mo.gov/main/OneSection.aspx?section=375.918 Accessed August 22, 2025.