Planning for retirement is more than numbers on a screen. You can align your saving, investing, and spending with what matters most to your family. Two simple tools, your 401(k) and IRAs, can move your closer to your retirement goals. Cost-of-living adjustments to 2026 401(k) and IRA contribution limits are now available. Understand how these limits fit into your long-term goals. Explore these changes for 2026 with clarity and purpose. Whether you’re saving for retirement, college, or future meaningful experiences.

401(k) Contribution and Catch-Up Limits (2026)

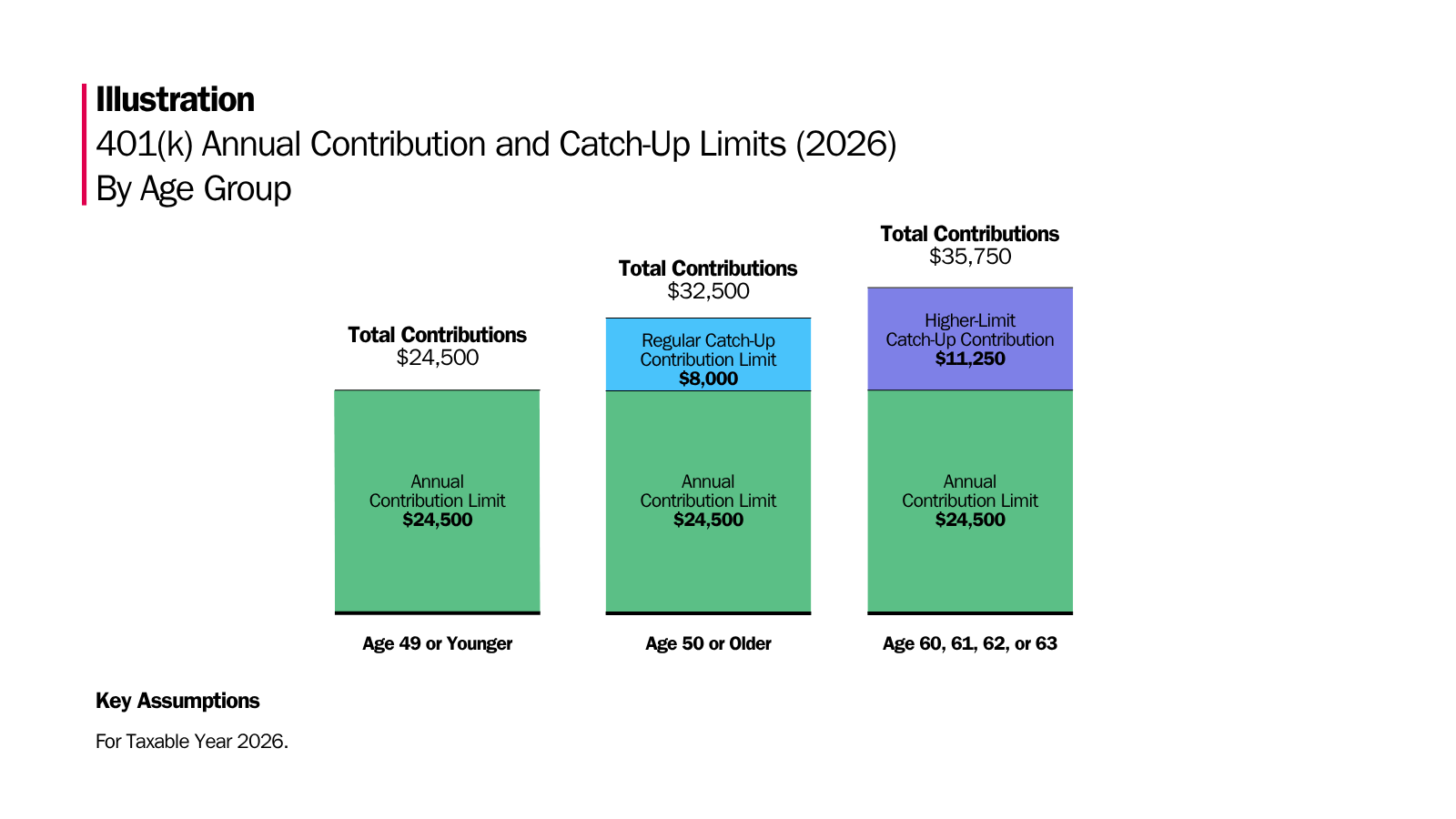

#1 Under Age 50: Maximum contribution limit is $24,500 in 2026. No catch-up contributions allowed.

#2 Age 50 and Over: Eligible for catch-up contributions up to $8,000.

#3 Age 60 to 63: Higher catch-up contribution up to $11,250.

IRA Contribution and Catch-Up Limits (2026)

- Traditional and Roth IRA Contribution Limits: $7,500.

- IRA catch-up contribution limit: $1,100. This limit generally applies to account owners age 50 and over.

Learning Points

Putting Your 401(k) and IRA Contribution Limits into Perspective

If one of your goals is to save for retirement, knowing how much you can contribute each year is essential.

Starting with what matters to you and your family is a vital first step when you think about your financial priorities. Too often, specific solutions – invest in this or don’t spend money on that – lead the conversation. In our view, that order is upside down.

Instead, your goals and values should guide you in how you save and invest for the future. Money and time are important tools for patient, long-term investors.

With that in mind, once you’re clear about what important things you are saving for, it’s worth your time to consider these annual adjustments to 401(k) contribution limits.

Are you on track for your short-term goals, like making memories with your family by going on vacations together? How confidently are you approaching saving and investing for your long-term aspirations, like retiring?

When retirement investors like you can ignore the day-to-day market fluctuations, and stick to your long-term investment strategy and goals, you are well-positioned to capture market returns and manage the related risks over the course of your lifetime.

However, that doesn’t mean you want to ignore changes to your personal situation. For example, are you getting married, do you plan to have another child in 2026, or earn a significant compensation adjustment for 2026?

Your life events can influence your savings priorities and personal tax situation.

Do the increased 401(k) and IRA contribution limits in 2026 help move you closer to your savings priorities? Does it mean you need to make some tradeoffs? If so, what are the right mix of solutions for you or your family?

When you’re comfortable that you’re minimizing your taxes, your living expenses are dialed in and aligned with your values, it becomes easier to save the right amounts toward your future goals and financial priorities.

With this as your backdrop, let’s review the cost-of-living adjustments for 401(k) contribution limits for 2026. Be sure to understand whether the 401(k) catch-up contribution limits and Roth catch-up requirement apply to your personal financial life.

401(k) Contribution Limit for 2026

The IRS released Notice 2025-67 on November 13, 2025, detailing the cost-of-living adjustments relating to retirement plans and IRAs.[i]

In 2026, the total employee contribution limit for your 401(k) is $24,500.

This limit also applies to retirement savers contributing to a 403(b), governmental 457 plans, or the federal government’s Thrift Savings Plan. This limit applies to both traditional 401(k) and Roth 401(k) accounts.

401(k) Catch-Up Contribution Limit for 2026

“Catch-up contributions” allow retirement savers who are age 50 or older to contribute additional amounts into a 401(k). In 2026, the catch-up contribution is $8,000.

This special provision is driven, at least in part, to make it even more appealing for retirement savers to increase retirement account contributions during “peak” earning years.

And so, applying these two limits together in practice, a catch-up eligible retirement saver in can contribute up to $32,500 ($24,500 + $8,000) in 2026.

401(k) Higher Catch-Up Contribution Limit for 2026

“But wait, there’s more…”

On Sept. 16, 2025 the IRS and the Department of the Treasury published final regulations for higher catch-ups. In 2026, the higher catch-up contribution limit is $11,250 for 401(k) accounts.

Meaning, eligible retirement savers in most 401(k)s can contribute up to $35,750 ($24,500 + $11,250) in 2026.

To be eligible for these enhanced catch-up contributions, you need to “attain age 60, 61 ,62, or 63 during the taxable year”.[ii]

Roth 401(k) Catch-Up Contribution Requirement

So, what’s the catch with these catch-up contributions?

If you’re considering eligible catch-up contributions, you’ll want to pay specific attention to how much you made the year before.

Specifically, if you are a catch-up eligible participant AND your FICA wages for the preceding calendar year from the employer sponsoring the plan exceed $150,000, your catch-up contributions must be designated Roth contributions in 2026.

This is commonly referred to as the Roth catch-up requirement.

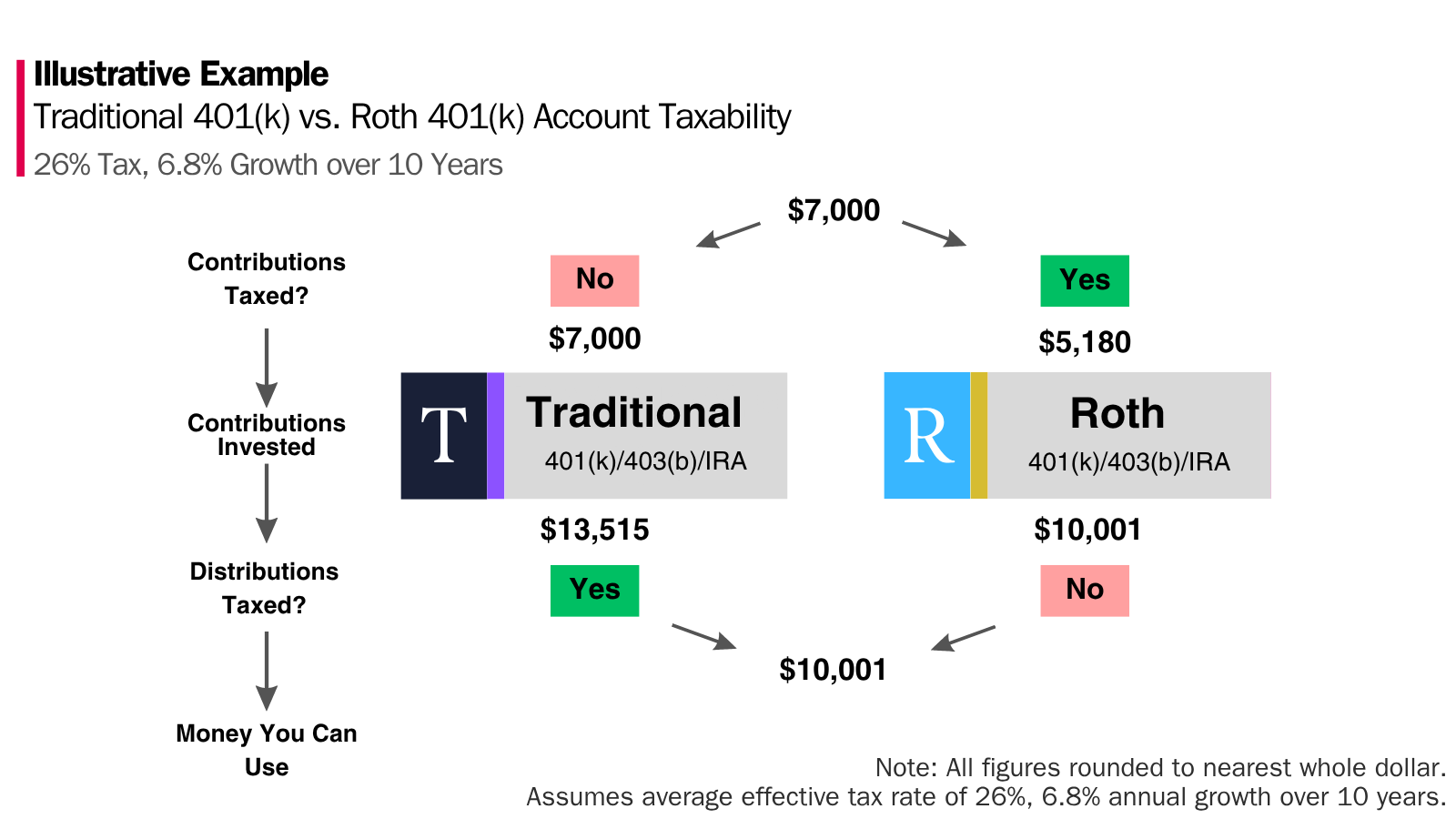

As a reminder, your Roth 401(k) contributions consist of after-tax dollars – money you’ve already paid income tax on.

This allows your contributions to grow tax-free. It also means when you spend the assets in these accounts during your retirement, the contributions and growth can be tax-exempt.

And so, retirement savers will want to re-evaluate how these updated 401(k) and IRA contribution limits align with their goals in 2026.

When used in combination with pre-tax retirement sources, after-tax accounts can help lower your taxable income. Your thoughtful investment tax planning should consider your personal situation and your details like marginal tax rate, retirement goals, and sources of income.

The illustration below helps highlight the difference between traditional 401(k) and Roth 401(k) taxability of contributions, growth, and distributions.

Total Contribution Limits for Your 401(k) in 2026

The total of all employee plus employer contributions, per employer, ticks up to $72,000 in 2026. This is an update to section 415(c)(1)(A) of the code for 2026.

Importantly, catch-up contributions (age 50+) and higher catch-up contributions (age 60-63) increase the total figure to $80,000 and $83,250, respectively.

Employer contributions could be in the form of matching, safe harbor, profit sharing, and/or non-elective contributions.

Traditional IRA and Roth IRA Contribution Limits for 2026

The IRS also updated the maximum IRA contribution limits for tax year 2026 in the same release.

In 2026, the annual limit on Traditional IRA and Roth IRA contributions is $7,500. This represents a cost-of-living increase of $500 from 2025.

For those of you reading who are really into the minutiae of this, here is minor, yet interesting point to highlight.

The term IRA is technically the abbreviation for Individual Retirement Arrangements. In practice, it is often referred to as an Individual Retirement Account.

Roth IRA Income Limitations

In 2026, there are modified adjusted gross income (MAGI) phase-out ranges for taxpayers making contributions to a Roth IRA. Those phase-out ranges are as follows:

- For single and head of household taxpayers, the income phase out is between $153,000 and $168,000.

- For married couples filing jointly, the income phase-out range is between $242,000 and $252,000.

IRA contributions can only be made with earned income. If only you or your spouse earned income in a particular tax year, you might still be able to contribute to your IRA. Be sure to read the Spousal IRA piece for additional details.

Traditional IRA Contribution Tax Deductibility

Notice 2025-67 also provides additional retirement planning details beyond 401(k) and IRA contribution limits. It also details the criteria for making tax deductible traditional IRA contributions.

If you meet specific eligibility criteria, you can deduct your contributions from your taxable income, which can lower your tax bill.

If you are covered by a workplace retirement plan, like a 401(k), your modified adjusted gross income (MAGI) affects the amount of your deduction.

Specifically, the deductibility of your traditional IRA contributions is limited by the following income phase-outs in 2025:

- For single and head of household taxpayers, the modified AGI phase out is between $81,000 and $91,000.

- For married couples filing jointly, the modified AGI phase-out range is between $129,000 and $149,000.

If you are not covered by a workplace retirement plan, like a 401(k), but your spouse is, the deductibility of your traditional IRA contributions is limited by the following income phase-out in 2025:

- For married couples filing jointly, the modified AGI phase-out range is between $242,000 and $252,000.

IRA Catch-Up Contribution Limit for 2026

The IRA catch-up contribution limit for 2026 is $1,100. This limit generally applies to account owners age 50 and over and represents an increase of $100 from the 2025 IRA catch-up limit.

Like so many topics in financial planning, coordinating with a qualified tax advisor can be an important step toward understanding your catch-up contribution eligibility.

A Long-Term Approach to Your Family’s Goals

Hopefully you found this quick update on 401(k) and IRA contribution limits helpful and educational as you think about your savings priorities in the year ahead.

Long-term investors like you can evaluate multiple financial priorities.

In addition to evaluating how much to contribute to retirement accounts like your 401(k) and IRA, we help professional and families like you understand gifting the maximum annual exclusion amount to fund your child’s 529, contributing to your dependent care FSA, reviewing your homeowners insurance, or increasing your emergency fund for example. We help you balance and align your savings priorities with your goals and values.

Taking a Strategic View of Your Finances

We help busy parents and professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

[i] IRS Notice 2025-67, Internal Revenue Service (November 13, 2025). 2026 Amounts Relating to Retirement Plans and IRAs, as Adjusted for Changes in Cost-of-Living. https://www.irs.gov/pub/irs-drop/n-25-67.pdf

[ii] 90 FR 44527 Department of Treasury and Internal Revenue Service. (2025, September 16). Catch-Up Contributions. Federal Register. https://www.federalregister.gov/documents/2025/09/16/2025-17865/catch-up-contributions