Giving back can be one of the most fulfilling parts of your financial journey. Donating to charity in 2026 can be straight forward, meaningful, and tax smart. This article highlights key changes to incorporate into your own charitable giving strategy. Let’s dive in and make your giving go further.

Summary: 2026 Charitable Giving Deductions

#1 For the Standard Deduction Crowd: If you take the standard deduction, you can also deduct your cash donations to charities up to the following amounts:

- $1,000 for single taxpayers

- $2,000 for married filing jointly taxpayers

#2 Itemizers: If you itemize your deductions, you can claim a charitable giving deduction only if your annual giving exceeds 0.5% of your adjusted gross income (AGI).

#3 Your deduction for charitable cash contributions cannot be more than 60% of your adjusted gross income (AGI).

Learning Points

Charitable Giving Deductions and the Feeling of Enough

Whether you donate your time and energy, or money to charity, it can be a powerful experience.

When you directly volunteer to support a charity’s mission, you can show your children to connect words and values to the real work of helping others. You lead by doing.

Donating hard-earned resources, in the form of cash, appreciated securities/capital gain property, or non-cash items, to a favorite charity can communicate a strong, underlying message that you have “enough”. Of abundance, fulfillment, and purpose.

For some investors, this can signal to yourself that you’re going to be O.K. financially when you donate to a charity. That you have enough.

You can embrace that feeling of enough and dial down the noise from the world around you. You can push back on the notion that you need more. More stuff. More money.

You can use the feeling of having “enough” as a calming force.

Because topics like charitable giving deductions, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with a qualified tax professional.

When you know the basics around charitable donations, and the potential tax planning opportunities available, you can feel better prepared to evaluate whether a certain approach works for your family’s specific situation. This piece is intended for a variety of readers to pick and choose the topic that’s most relevant to them, given their personal financial situation.

If you itemize your deductions, there are new rules you want to be aware of. But wait. If you take the standard deduction, there’s something for you, too.

Read on to explore how the One Big Beautiful Bill Act influences charitable giving deductions and your charitable donation plans for 2025, 2026, and beyond.

Combining the Standard Deduction and Cash Donation Deduction in 2026

H.R. 1, commonly referred to as the OBBBA or “One Big Beautiful Bill Act”, introduced a raft of tax changes to evaluate in 2025 and beyond.

For example, effective for tax years after December 31, 2025, Section 70424 of the OBBBA allows taxpayers who elect to take the standard deduction, to additional charitable giving deductions for certain cash donations they make the qualified organizations.

Starting in 2026, cash donations to qualified organizations have a maximum deduction cap of:

- $1,000 for single taxpayers

- $2,000 for married filing jointly taxpayers[i]

Cash contributions currently include donations made in the form of cash, check, electronic funds transfer, online payment service, debit card, credit card, payroll deduction, or a transfer of a gift card redeemable for cash.

If you plan to take the standard deduction in 2026, these increased cash contribution deduction limits allow non-itemizers to provide even more meaningful support of charitable organizations. In addition to these elevated limits, the IRS Revenue Procedure 2025-32 updated the Standard Deduction tables in 2026.

The following table shows these two different deduction limits side-by-side[ii]:

| Deduction Tables | ||

| Filing Status | Standard Deduction | Cash Contribution Deduction |

| Single/Unmarried Individuals | $ 16,100 | $ 1,000 |

| Married Filing Separate | $ 16,100 | $ 1,000 |

| Married Filing Jointly / Surviving Spouse | $ 32,200 | $ 2,000 |

| Head of Households | $ 24,150 | $ 1,000 |

Keep in mind that this limit does not allow you to deduct contributions to donor advised funds, supporting organizations, or private foundations.

Resource: Tax Exempt Organization Search

To look up the tax status of a particular organization, you can use the IRS search tool: https://www.irs.gov/charities-non-profits/tax-exempt-organization-search

The site provides users with two key ‘Publication 78’ data points and states that site users may rely on “in determining the deductibility of their contributions”:

- On Publication 78 Data List: e.g. Yes / No

- Deductibility Code: e.g. PC / PF

| Table: Deductibility Code | ||

| Deductibility Code | Type of organization and use of contribution | Deductibility Limitation |

| PC | A public charity. | 50% (60% for cash contributions) |

| POF | A private operating foundation. | 50% (60% for cash contributions) |

| PF | A private foundation. | 30% (generally) |

| GROUP | Generally, a central organization holding a group exemption letter, whose subordinate units covered by the group exemption are also eligible to receive tax-deductible contributions, even though they are not separately listed. | Depends on various factors |

| LODGE | A domestic fraternal society, operating under the lodge system, but only if the contribution is to be used exclusively for charitable purposes. | 30% |

| UNKWN | A charitable organization whose public charity status has not been determined. | Depends on various factors |

| EO | An organization described in section 170(c) of the Internal Revenue Code other than a public charity or private foundation. | Depends on various factors |

| FORGN | A foreign-addressed organization. These are generally organizations formed in the United States that conduct activities in foreign countries. Certain foreign organizations that receive charitable contributions deductible pursuant to treaty are also included, as are organizations created in U.S. possessions. | Depends on various factors |

| SO | A Type I, Type II, or functionally integrated Type III supporting organization. | 50% (60% for cash contributions) |

| SONFI | A non-functionally integrated Type III supporting organization. | 50% (60% for cash contributions) |

| SOUNK | A supporting organization, unspecified type. | 50% (60% for cash contributions) |

| Source: Internal Revenue Service, Deductibility Codes, https://apps.irs.gov/app/eos/details/ | ||

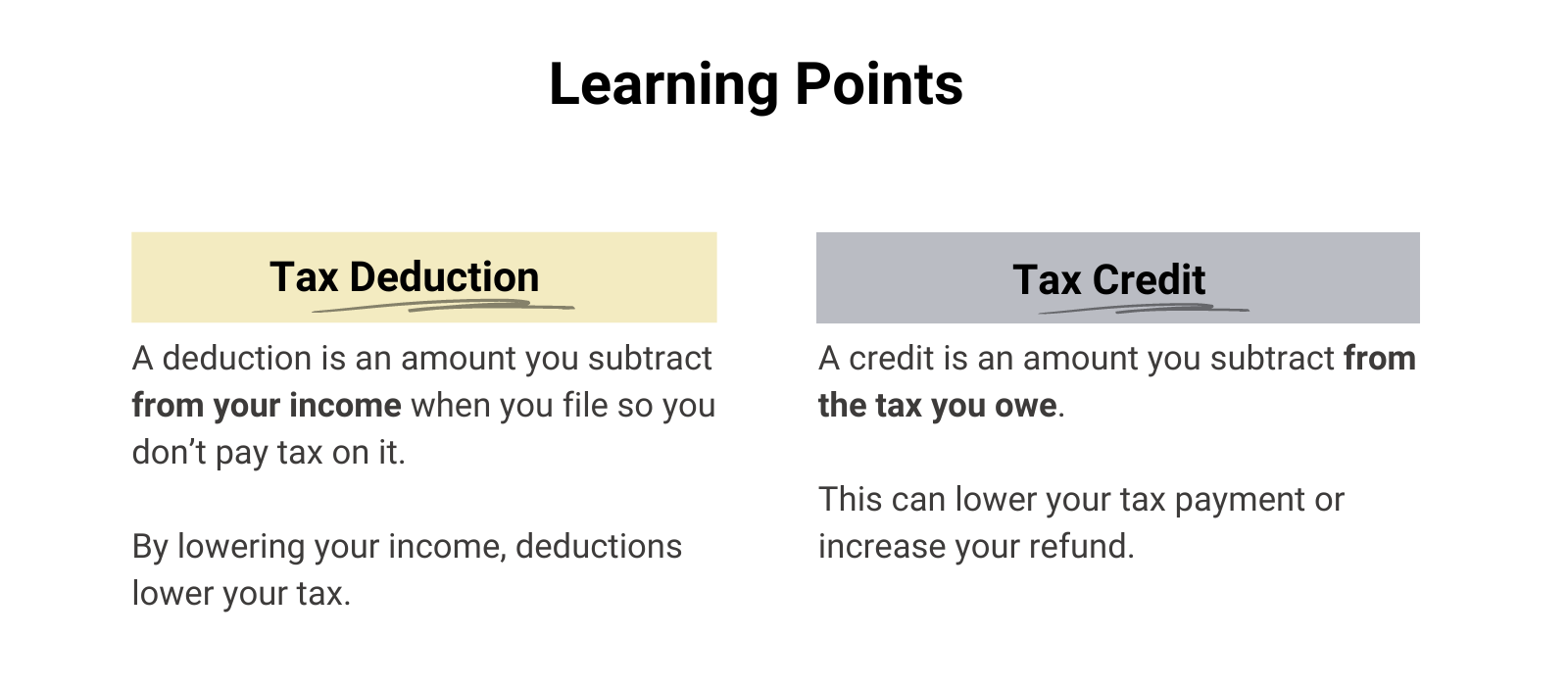

What is the Difference Between a Tax Deduction and a Tax Credit

When you’re evaluating charitable giving deductions, it’s worth recalling the distinction between tax deductions and tax credits.

- Tax Deduction: The amount you save with a tax deduction depends on your tax bracket. For example, if you’re in the 37% tax bracket, a $1,000 tax deduction could potentially save you $370 off your tax bill.

- Tax Credit: A tax credit reduces the tax you owe. For example, a $1,000 tax credit could potentially save you $1,000 off your tax bill.

Charitable Giving Deduction Essentials: Documentation

So far, we’ve covered the following two elements:

- How cash contributions to qualified charities are deductible, and

- How tax deductions adjust your tax bill

It can be easy to skip ahead and overlook the right documentation for a given contribution type. However, after you write that check or click donate, be sure to get the right documentation from any charity you donate to, even if it’s only for your tax records.

For each charitable contribution, there are specific documentation rules you’ll need to follow depending on:

- how much you contribute, and

- what you contribute (e.g. cash, noncash, and capital gain property)

Next, we’ll highlight the documentation requirements of two common charitable giving deduction scenarios involving cash contributions. These are just a couple of the many possible scenarios that charitably inclined professionals and families might consider each year.

Keep in mind that there are special rules for specific situations, like when you contribute any of the following:

- Clothing or household items

- A car, boat, or airplane

- Taxidermy property

- Property subject to a debt

- A partial interest in property

- A fractional interest in tangible personal property

- A qualified conservation contribution

- A future interest in tangible personal property

- Inventory from your business

- A patent or other intellectual property

The fact that taxidermy property is carved out on this list is currently a favorite for me. There’s a Tax Court case on this topic is an interesting read.

Cash Contributions Less than $250

Currently, if you make a cash contribution of less than $250, and want to deduct it, you will need one of the following pieces of documentation:

- Bank record showing the name of the qualified organization, date of contribution, and amount of contribution, including a(n):

- canceled check

- bank or credit union statement

- credit card statement

- electronic fund transfer receipt

- a scan of both sides of a canceled check from a bank or credit union website

– or –

- A receipt, letter, or other written communication (e.g. email) showing the name of the qualified organization, date of contribution, and amount of contribution.

There are similar requirements if you want to deduct cash contributions to charities made via a payroll deduction.

It’s notable that you don’t combine separate transactions into an aggregated annual amount when applying this documentation requirement. Each payment is its own separate contribution.

For example, you make a recurring $100 cash contribution to a qualified charity each month. Each unique monthly cash contribution would need documentation that follows the above approach for a charitable giving deduction.

Cash Contributions of $250 or More: Contemporaneous Written Documentation (CWA)

If you want to claim a deduction for your qualified charity cash contribution of $250 or more, you’ll need contemporaneous written acknowledgement, sometimes referred to as CWA. That’s right. C-W-A. Some acronyms just make sense.

A contemporaneous written acknowledgment needs to meet the following timing requirements: [iii]

- received on or before the earlier of the date you file a tax return for the tax year in which the contribution was made, or

- the due date (including extensions) of the return.

The written acknowledgment should include the following information:

- name of the organization,

- amount of cash contribution,

- description (but not value) of non-cash contribution

- whether the qualified organization provided you any goods or services,

- description and good faith estimate of the value of goods or services, if any, that organization provided in return for the contribution; and

- statement that goods or services, if any, that the organization provided in return for the contribution consisted entirely of intangible religious benefits, if that was the case.

You need to receive a written acknowledgement of your contribution from the charitable organization before filing your return.

For perspective, this charitable giving deduction requirement has been in place since the Pension Protection Act of 2006.

Updates for Itemizers Donating to Charities in 2026

0.5% Floor on Deduction of Contributions by Individuals

H.R. 1, commonly referred to as the OBBBA or “One Big Beautiful Bill Act”, made the following requirement effective for tax years after December 31, 2025.

Section 70425 of the OBBBA allows itemizing taxpayers to claim a charitable giving deduction only if their annual giving exceeds 0.5% of their adjusted gross income (AGI). Currently, both cash and non-cash donations qualify toward the 0.5% AGI hurdle. [i]

Once the 0.5% floor is cleared, only those amounts that exceed 0.5% of AGI count as allowable deductions and deductibility limits continue to apply.

5-Year Carryforward

Section 70425 also addresses what happens if you itemize and some, or all, your charitable contributions don’t exceed the 0.5% AGI floor requirement.

Taxpayers may carry forward those unused amounts for five years. The 5-year carryforward clock runs out “following the fifth taxable year after the taxable year in which the charitable contribution was first taken into account.” You can use these carryforward contributions when your charitable contributions exceed the 0.5% floor requirement in a future taxable year. These contributions are made on a first-in, first-out basis (FIFO).

It’s important to highlight that you can only apply these unused carryforward amounts in a year you itemize your charitable giving deductions.

In these situations, taxpayers can evaluate several charitable giving strategies. For example, charitable donation bunching would allow you to provide significant financial support to a charity and clear the 0.5% AGI hurdle.

Planning ahead, you could try to time your bunching strategy to occur during a relatively lower income year. Just know that if you routinely take this approach, you’ll leave some amount of money in the 0.5% of AGI in the carryforward bucket.

Limitation for Cash Contributions to Charities

Section 70425 of the OBBBA also made “permanent” that your deduction for charitable cash contributions cannot be more than 60% of your adjusted gross income (AGI).

This functions as a cap on your charitable donation bunching strategy and in coordination with other limitations.

Publication 526, Charitable Contributions, which provides a walk through and Worksheet 2 detailing how to determine your deductions when different limits apply. [iv]

Limitation on Tax Benefit of Itemized Deductions

Section 70111 of the OBBBA also implemented what amounts to a 35% AGI cap on itemized deductions, including the charitable contribution deduction for taxpayers in the 37% bracket. This limit is applied in coordination with other limitations after

This means that high earners in the 37% tax bracket will no longer receive a dollar-for-dollar value in their charitable giving deduction.

This new cap works in combination with the 0.5% AGI floor discussed earlier.

A Long-Term Approach to Your Family’s Goals

Hopefully this educational update on charitable giving deductions allows you to be more informed, prepared to evaluate, and support your own charitable goals.

Think about how you can make progress in your financial life, so that you can continue to focus on the people and experiences that matter.

You can align your financial plan with directly supporting causes and organizations that matter to you and your family. When you take a strategic view of your charitable goals and efforts, and combine it with thoughtful tax planning, you can efficiently share your resources with deserving charities.

In addition to evaluating your charitable giving options, we help professional and families like you understand how to fund your child’s 529, contribute to your dependent care FSA, review your homeowners insurance, or increase your emergency fund. We help you balance and align your savings priorities with your goals and values.

Taking a Strategic View of Your Finances

We help busy parents and professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

[i] “H.R.1 – 119th Congress (2025-2026): One Big Beautiful Bill Act.” Congress.gov, Library of Congress, 4 July 2025, https://www.congress.gov/bill/119th-congress/house-bill/1

[ii] IRS Revenue Procedure 2025-32, “Administrative, Procedural, and Miscellaneous”, IRS.gov, Internal Revenue Service, 9 October 2025, https://www.irs.gov/pub/irs-drop/rp-25-32.pdf

[iii] “Charitable Contributions – Substantiation and Disclosure Requirements”, IRS.gov, Internal Revenue Service, 24 November 2024 https://www.irs.gov/charities-non-profits/charitable-organizations/charitable-contributions-written-acknowledgments

[iv] “Publication 526, Charitable Contributions.”, IRS.gov, Internal Revenue Service, 26 February 2025, https://www.irs.gov/pub/irs-pdf/p526.pdf