For married couples interested in saving for retirement, a Spousal IRA can help you keep making progress toward your goals. Read on to explore the defining aspects of the Spousal IRA in this quick read. Whether you’re just starting to save for retirement, or looking to increase your retirement savings, understanding the different retirement saving options available to you can bring clarity and balance to your long-term financial goals.

Learning Points

What is an Individual Retirement Account (IRA)

IRAs can sometimes feel familiar from afar – it’s all right there in the name “Individual Retirement Account” – and then, after a closer review, it can seem entirely foreign.

You’re likely familiar your 401(k) account. Like, how your paycheck is used to contribute to your 401(k) and your plan regularly send communications about your 401(k).

It can sometimes feel like there is more structure and educational resources built around your 401(k) experience than the average IRA.

An Individual Retirement Account (IRA) is a tax-advantaged personal savings account generally used for setting money aside for retirement.

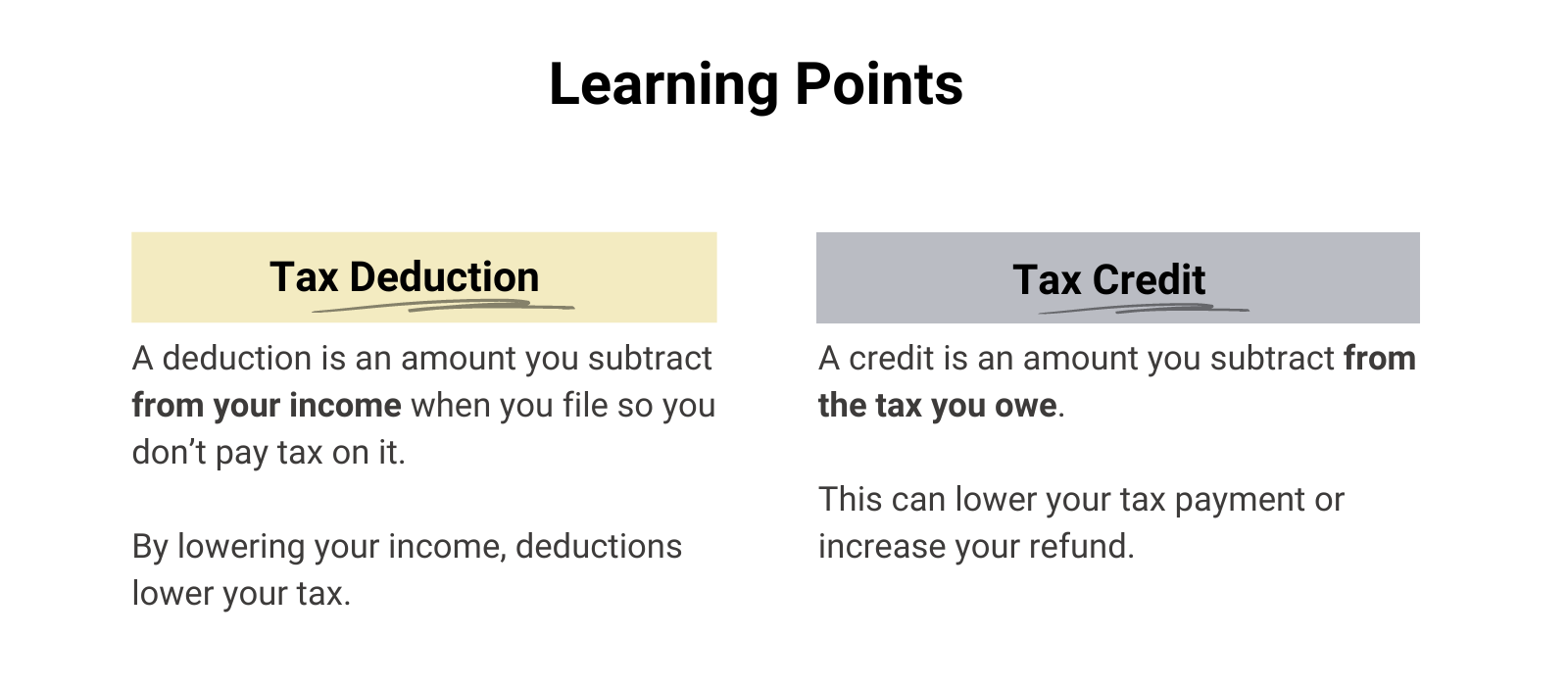

Depending on the type of IRA you select and your personal circumstances, these tax advantages can include tax-deductible contributions for traditional IRAs and tax-free withdrawals for Roth IRAs.

For most investors, IRAs generally complement, but do not fully replace employer-sponsored plans, like a 401(k) or a 403(b), for your retirement savings goals.

Both Roth and Traditional IRAs offer unique benefits and considerations for investors like you.

Next, let’s explore the key elements of the Spousal IRA

Key Details for Spousal IRAs in 2025

If you or your spouse are planning a career pivot, to take time out of the workforce to care for a growing family, go to school, or to look after an aging family member, the Spousal IRA rules can help you keep you saving for your future retirement.

Specifically, the Spousal IRA rules allow one working spouse to contribute to the other spouse’s IRA. The IRA can be either a traditional IRA and/or a Roth IRA. Each type of IRA has specific rules governing contribution amounts, income limits, taxability of contributions and distributions, as well as estate planning considerations.

At a practical level, there is not a “Spousal IRA” type of account.

You can plan make eligible Spousal IRA account contributions to a new or existing Traditional IRA and/or Roth IRA.

Contribution Limits

A spousal IRA is a special provision that allows a working spouse to contribute to the other spouse’s individual retirement account (IRA).

After all, you’re a team, right?

For 2025, if you file a joint return and your taxable compensation is less than that of your spouse, the most that can be contributed for the year to your IRA is the smaller of the following two amounts:

- $7,000 ($8,000 if you are age 50 or older).

- The total compensation includible in the gross income of both you and your spouse for the year, reduced by the following two amounts.

- Your spouse’s IRA contribution for the year to a traditional IRA.

- Any contributions for the year to a Roth IRA on behalf of your spouse.

Source: Publication 590-A (2024), Contributions to Individual Retirement Arrangements (IRAs), https://www.irs.gov/publications/p590a#en_US_2024_publink1000230412

Keep in mind, IRA contribution limits are per taxpayer (not per account). If you have both a Roth IRA and a traditional IRA, you aggregate your contributions across all your IRA accounts up to the applicable limit.

Annual Cashflow Planning: IRA Contributions for Both Spouses

If saving for retirement is one of your priorities in 2025, you and your spouse could contribute the following total maximum amounts to your IRAs, including a Spousal IRA:

- $14,000 if you are both under age 50. This assumes you each contribute a maximum allowable amount of $7,000 to your IRAs in 2025.

- $15,000 if only one of you is age 50, or older. Specifically, this assumes one spouse, who is age 50 or older, contributes a maximum allowable amount of $8,000 to their IRAs. The other spouse, who is age 49 or younger, contribute a maximum allowable amount of $7,000 to their IRAs.

- $16,000 if both of you are age 50 or older. This scenario assumes you each contribute a maximum allowable amount of $8,000 to your IRAs.

Tax Deductibility: Spousal IRA

Generally, your deduction for Spousal IRA contributions to a traditional IRA (for the spouse with less compensation) is limited to the lesser of:

- $7,000 ($8,000 if the spouse with the lower compensation is age 50 or older), or

- The total compensation includible in the gross income of both spouses for the year reduced by the following three amounts.

- The IRA deduction for the year of the spouse with the greater compensation.

- Any designated nondeductible contribution for the year made on behalf of the spouse with the greater compensation.

- Any contributions for the year to a Roth IRA on behalf of the spouse with the greater compensation.

Because topics like Spousal IRAs, like so many others in financial planning, intersect with the world of tax, make sure you coordinate with your qualified tax professional.

Tax Deductibility Limitations

- Specialized Employee Pension Benefit Plan: The deductibility limit above is reduced by any contributions to a section 501(c)(18) plan on behalf of the spouse with the lesser compensation.

- Divorced or Separated: If you were divorced or legally separated (and didn’t remarry) before the end of the year, you can’t deduct any contributions to your spouse’s IRA. After a divorce or legal separation, you can deduct only the contributions to your own IRA. Your deductions are subject to the rules for single individuals.

- Covered by Employer Plan: If you, or your spouse, was covered by an employer retirement plan at any time during the year for which contributions were made, your deduction may be further limited.

Age Limitations

There are no age limits on making contributions to traditional IRAs or Roth IRAs.

IRA Contribution Deadline: Tax Year 2025

The 2025 IRA contribution deadline is April 15, 2026. You have until that date to make contributions for the 2025 tax year.

Taking a Strategic View of Your Finances

Hopefully you found this overview of the Spousal IRA helpful and educational for your own planning in 2025.

When evaluating what type(s) of IRAs best align with your goals, you’ll want to fully incorporate all the moving parts of your financial life into your decision.

Are you on track for your short-term goals, like making memories with your family by going on vacations together? How confidently are you approaching saving and investing for your long-term aspirations, like retiring or pursuing a meaningful second career?

We help busy parents and individual professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.