Funding your children’s lifetime of education is a significant family priority. It often involves a mix of resources and thoughtful planning. Explore whether a 529 account aligns with your savings priorities. Understand potential trade-offs. Confidently transform your children’s educational dreams into achievable goals.

*This post has been updated to incorporate new and updated provisions introduced by H.R. 1, commonly referred to as the OBBBA or “One Big Beautiful Bill Act”. The OBBBA was signed into law on July 4, 2025.

Learning Points

The Importance of Planning How to Fund Your Child’s Education

For many families in America, higher education aspirations are funded by a mix of parent and student loans, savings, and current income.

The dream of giving your child the gift of a great college education can be financially challenging without thoughtful planning.

If you’re evaluating ways to financially support your child’s education, you can analyze whether saving and investing in a 529 account when your children are young supports your education funding goal.

Currently, college is one of several ways families can effectively use their 529 account funds.

In 2024, Sallie Mae and Ipsos released a study titled ‘How America Pays for College’. This data-rich report details a variety of factors and approaches to how American families pay for their child’s higher education. One notable statistic from this report was that families with $150,000+ in annual income reported that an average of 19%, or $5,147, of the Total Cost of Attendance was covered by a “college savings fund, such as a 529 plan” for academic year 2023-2024[i].

Taking A Long-Term View of Your Family’s Goals

An essential step of a robust financial plan is to understand the downsides and tradeoffs of using your family’s resources to fund one savings priority over another.

As a parent, it’s important to evaluate whether funding your own retirement is a higher priority than your child’s future education. For some families, that means you want to analyze the right balance of retirement and education funding contributions.

Long-term investors like you can evaluate multiple savings priorities. Understanding whether fully funding your 401(k), gifting the maximum annual exclusion amount to your child’s 529, increasing your emergency fund, or some combination of these and other savings priorities aligns with your goals and values.

When you’re comfortable that you’re minimizing your taxes, your living expenses are dialed in and aligned with your values, it becomes easier to save the right amounts toward your future goals/savings priorities.

Aligning Your Family’s Education Goals and 529 Account Use Cases

With families deploying a mixture of student loans, scholarships, federal work-study, grants, current income and investment assets to pay for higher education, a 529 account is just one of the many tools that families have available to them.

Given the variety of additional funding resources available to families for undergraduate-related expenses, you’ll want to understand how you can use 529 assets before, during, and after your child’s undergraduate years.

529 accounts allow families a flexible, tax-advantaged way to save and invest in support of the following educational goals:

- Kindergarten through 12th grade (K-12)

- Trade Schools / Apprentice Programs

- Undergraduate studies

- Qualifying graduate schools

- Student loan repayment

Depending on factors like where you live and what 529 plan you use, a 529 account can support your family’s education funding goals in the following ways:

- Tax-Advantaged Growth: Contributions to a 529 plan may be tax-deductible at the state level (depending on the state). More importantly, the money invested in the account grows tax-deferred at the federal level, and in many cases, at the state level as well. This means you won’t pay taxes on the earnings as long as the funds are used for qualified education expenses.

- Tax-Free Withdrawals: When the money is withdrawn to pay for qualified education expenses, those withdrawals are federal income tax-free and often state income tax-free as well. This can lead to significant savings over time compared to using taxable investment accounts.

- Investment Flexibility: 529 accounts offer investors a variety of investment choices that align with each family’s ability, willingness, and capacity for risk. Ultimately, you’ll want to follow an investment strategy that allows you to sleep at night.

Like so many topics in financial planning, coordinating with a qualified tax advisor can be an important step when planning your education funding strategy.

If funding your child’s 529 account is a savings priority for you, read on, and familiarize yourself with the essential details of these investment accounts.

529 Plan Types

A section 529 plan is a tax-advantaged investment program designed to help families save for education expenses. 529 plans are also known as a “qualified tuition plan”. 529 plans are sponsored by states, state agencies, and educational institutions. In 2025, there are two kinds of 529 plans:

- Education Savings Plans: most education savings plans are available to everyone. A few have residency requirements for the account holder and/or the beneficiary. This type of plan provides a broader use-case for families than a Prepaid Tuition Plan.

- Prepaid Tuition Plans: While these typically have residency requirements, one notable exception is a prepaid tuition plan sponsored by a group of private colleges and universities. This is a narrower use-case than an Education Savings Plan. It does provide clarity for families whose education funding goals align with this plan’s specific use.

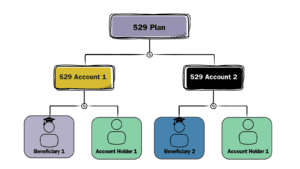

529 Account Roles

When you open a 529 account through either of these two plan types, your role is called the account holder, or the saver. The account holder opens the account for the beneficiary (e.g. your child). Technically, the account holder and the beneficiary can be the same person.

The chart below illustrates how these roles fit together for a family with two children.

An account holder can open multiple 529 accounts at the same 529 plan, and each account can be for a different beneficiary.

Key Considerations For 529 Accounts

There is no “one-size fits all” 529 strategy. The way you approach selecting, opening, and managing a 529 account depends on your personal facts and circumstances.

Here’s a simple framework to follow:

- What state do you live in?

- When does your 529 beneficiary need to use the money?

- What kind of educational need, or needs, will the 529 fund?

Your 529 Account Starting Point: What State Do You Live In?

It’s helpful to center your 529 plan analysis around your state of residency.

This is primarily driven by each state’s specific approach to taxes on 529 plan contributions and distributions. Centering your analysis at the state level helps you create a base case which you can then compare against other 529 plans and education savings accounts.

For example, some states, like Missouri, offer residents a tax deduction for their 529 plan contributions. Other states, like Kentucky, assess an income tax but do provide a tax deduction or credit for 529 plan contributions. The amounts of these tax deductions vary from state to state.

If you live in a state that has no state income tax, like Texas or Tennessee, there is no state income tax deduction or credit to consider.

Similarly, when it comes to K-12 tuition, the states have a mixed view. Some states, like New York, currently take the position that paying for K-12 expenses with 529 funds is a non-qualified distribution.

If you live in a state that follows this approach, this could influence the timing of when you plan to distribute funds from your 529 account. Other states allow you to use 529 assets to pay for qualified education expenses.

The takeaway here is to familiarize yourself with your state’s specific 529 plan-related rules, tax benefits, and limits.

Reciprocity Arrangements

Some states that levy state income taxes, like Missouri, provide additional flexibility for residents to use 529 plans from other states. This kind of reciprocity arrangement treats other state’s plans the same way as the in-state plan is treated.

And so, you’ll want to be clear on the details of each state’s reciprocity arrangement before enrolling in a 529 plan sponsored by a different state. These reciprocity arrangements can change.

Check with the plan’s administrator or your qualified tax professional for the latest information.

Contributions

While contributions to a 529 account are not tax-deductible at the federal level, they are subject to the annual gift tax exclusion limit. In 2025, an individual’s annual gift tax exclusion limit is $19,000 per recipient.

Many states offer a tax deduction, and a handful offer tax credits, for residents who contribute to a 529 plan.

Notably, Missouri residents may claim this benefit whether they invest in a Missouri 529 plan or another state’s 529 plan. For example, Missouri residents can contribute up to the following amounts in a 529 plan and reduce adjusted gross income[ii]:

- $8,000 (filing single)

- $16,000 (married filing jointly)

Given this approach, for example, if a Missouri resident grandparent contributes to their grandchild’s out-of-state 529 account, they would still receive this tax benefit. The same holds true for a Missouri parent contributing to their child’s out-of-state 529 account.

Qualified Rollovers

“What happens if my family moves, and therefore, changes our state of residence?”

“What if my current 529 plan no longer fits my family’s needs due to high fees or investment options that don’t align with our goals?”

Moving all or some of your money between 529 plans is a flexible way to manage your 529 assets. Specifically, you can transfer funds to a different 529 plan for the same beneficiary or a qualifying family member. Each plan will detail the specific requirements to follow.

A qualified rollover for a 529 account has no federal income tax consequences as long as you complete the move within 60 days and you haven’t done a similar rollover for that person in the 12 months.

This empowers you to choose the best 529 plan for your family’s evolving needs.

Earnings

529 account earnings grow tax-free while invested in the plan and are not treated as income for either the account holder or the beneficiary.

Maximums

Some 529 plans will often state the maximum account balance or maximum contribution limit.

Until you hit the maximum account balance, the plan will accept contributions to your account(s) until the aggregate balances for the same beneficiary reach the predetermined limit.

Or, if your plan has a maximum contribution limit then the accounts for the same beneficiary that have reached this limit may continue to accrue earnings but will not accept any additional contributions. With this provision, your 529 account(s) could exceed the stated limit, but only as a result of earnings/investment growth.

For 529 plans with maximum limits, it represents an estimated maximum cost of some combination of undergraduate and graduate school. The maximum on a 529 plan may adjust each year to reflect the rising cost of higher education.

Currently there is not a federal limit on the total amount that can be contributed to a 529 plan. The limits are determined at the state level.

Withdrawals

When you use 529 account withdrawals, comprised of contributions and earnings, to pay for qualified education expenses, those distributions are not taxable.

However, the earnings on non-qualified withdrawals may be subject to federal income tax and a 10% federal penalty tax, state and local income taxes and recapture of state tax deductions.

The timing of your 529 account withdrawals should match the same tax year you paid the qualified educational expenses. If your total distributions exceed the beneficiary’s qualified education expenses, the excess portion of the earnings is taxable.

In the example of a Missouri resident, qualified 529 withdrawals are not taxable whether the Missouri resident has a Missouri 529 account or an out-of-state 529 account.

Qualified Higher Education Expenses

For families considering a 529 account, the following summary of expenses are currently included as Qualified Higher Education Expenses:

Tuition, fees, and the costs of books, supplies, and equipment required by the Eligible Educational Institution.

Some room and board costs are qualified when your child is attending at least half-time. Be sure to consult with your school to determine what counts as half-time.

Apprenticeship Program

The fees, books, and equipment required by qualifying programs. Parents will want to consult with the specific institution to verify whether it is a certified apprenticeship institution.

Qualified K-12 Education: OBBBA Expanded Edition

Many, but not all, 529 plans allow distributions of up to $10,000 per year, per beneficiary, for qualified higher education expenses in connection with enrollment or attendance at a K-12 school.

These include elementary or secondary public, private, or religious schools.

H.R. 1, commonly referred to as the OBBBA or “One Big Beautiful Bill Act”, expanded the use of 529 funds.

Effective after July 4, 2025, Section 70413 of the OBBBA widened the scope of “qualifying higher education expenses” to include materials, standardized testing, tutoring, and therapies for K-12 education.

Here is the new, expanded list of qualifying higher education expenses available to American families for K-12 education [iii]:

- Tuition

- Curriculum and curricular materials.

- Books or other instructional materials.

- Online educational materials.

- Tuition for tutoring or educational classes outside of the home, including at a tutoring facility, but only if the tutor or instructor is not related to the student and

- is licensed as a teacher in any State,

- has taught at an eligible educational institution, or

- is a subject matter expert in the relevant subject.

- Fees for a nationally standardized norm-referenced achievement test, an advanced placement examination, or any examinations related to college or university admission.

- Fees for dual enrollment in an institution of higher education.

- Educational therapies for students with disabilities provided by a licensed or accredited practitioner or provider, including occupational, behavioral, physical, and speech-language therapies.

Again, the updated/expanded language only applies to 529 distributions made after the date of the enactment – July 4, 2025 – of the OBBBA.

This expanded definition empowers families to better support their child’s educational needs and goals. Tutoring and therapy representing significant expenses educational expenses for some American families.

Looking ahead to 2026, families will be able to use up to $20,000 of 529 funds, per beneficiary, to pay for K-12 qualified higher education expenses.

Postsecondary Credentialing Expenses

Interestingly, Section 70414 of the OBBBA expanded Americans’ ability to use their 529 funds toward certain ‘postsecondary credentialing expenses’.

To quickly orient you, here are the three key terms to track:

- recognized postsecondary credential program

- recognized postsecondary credential

- qualified higher education expenses

Let’s walk through each of these terms in a little more detail. A “recognized postsecondary credential program’ is any program used to obtain a recognized postsecondary credential that it is:

- included on a State list prepared under Section 122(d) of the Workforce Innovation and Opportunity Act (WIOA)[iv],

- listed in the public directory of the Web Enabled Approval Management System (WEAMS) of the Veterans Benefits Administration, or successor directory such program,

- an examination (developed or administered by an organization widely recognized as providing reputable credentials in the occupation) is required to obtain or maintain such credential and such organization recognizes such program as providing training or education which prepares individuals to take such examination, or

- such program is identified by the Secretary, after consultation with the Secretary of Labor, as being a reputable program for obtaining a recognized postsecondary credential for purposes of this subparagraph.

The term ‘recognized postsecondary credential’ is defined as:

- any postsecondary employment credential that is industry recognized and is:

- issued by a program that is accredited by the Institute for Credentialing Excellence, the National Commission on Certifying Agencies, or the American National Standards Institute,

- included in the Credentialing Opportunities On-Line (COOL) directory of credentialing programs (or successor directory) maintained by the Department of Defense or by any branch of the Armed Forces, or

- identified for purposes of this clause by the Secretary, after consultation with the Secretary of Labor, as being industry recognized.

- any certificate of completion of an apprenticeship that is registered and certified under National Apprenticeship Act,

- any occupational or professional license issued or recognized by a State or the Federal Government (and any certification that satisfies a condition for obtaining such a license), and

- any recognized postsecondary credential as defined in section 3(52) of the Workforce Innovation and Opportunity Act.

The term ‘qualified higher education expenses’ includes the following qualified postsecondary credentialing expenses:

- tuition, fees, books, supplies, and equipment required for the enrollment or attendance of a designated beneficiary in a recognized postsecondary credential program, or any other expense incurred in connection with enrollment in or attendance at a recognized postsecondary credential program if such expense would, if incurred in connection with enrollment or attendance at an eligible educational institution, be covered under subsection (e)(3)(A),

- fees for testing if such testing is required to obtain or maintain a recognized postsecondary credential, and

- fees for continuing education if such education is required to maintain a recognized postsecondary credential.

The details matter here, and hopefully this updated educational post helps you better navigate your specific situation.

Student Loan Repayment

You can disburse 529 account assets to pay principal and/or interest on your designated beneficiary’s or their sibling’s qualified student loan. In 2025, this option is limited to a lifetime maximum of $10,000 per beneficiary when used to repay qualified student loans for the beneficiary, or the beneficiary’s sibling.

Keep in mind that if you use your 529 account to repay your eligible student loan, you would not be able to include any interest from that portion of the loan repayment in your federal income tax deduction.

Taking a Strategic View of Your Finances

We help busy parents and individual professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts – what are our options to give even more meaningful support?

As your financial planner in Saint Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step together, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.

[i] Sallie Mae and Ipsos. (2024). How America Pays for College. How America Pays for College | Sallie Mae. https://www.salliemae.com/content/dam/slm/writtencontent/Research/HAP_2024.pdf

[ii] MO Rev Stat § 166.435 (2021) https://revisor.mo.gov/main/OneSection.aspx?section=166.435

[iii] “H.R.1 – 119th Congress (2025-2026): One Big Beautiful Bill Act.” Congress.gov, Library of Congress, 4 July 2025, https://www.congress.gov/bill/119th-congress/house-bill/1

[iv] “H.R.803 – 113th Congress (2013-2014): Workforce Innovation and Opportunity Act.” Congress.gov, Library of Congress, 22 July 2014, https://www.congress.gov/bill/113th-congress/house-bill/803