By: Jeff McGovern

Jeff is the lead financial planner at Haven Wealth Planning and has more than 16 years of experience in the wealth management industry. He has completed the Boston University Financial Planning Program and holds an MBA from Washington University in St. Louis. He received a Bachelor of Business Administration in finance and a Bachelor of Arts in markets and culture from Southern Methodist University in Dallas, Texas.

Many families want to help pay for their children’s education but aren’t sure where to begin. This 529 account guide explains the essentials in plain language with clear, actionable insights. It takes a grounded look at how families can contribute to, invest in, and use a 529 account to cover education expenses, while calling attention to state-specific details that quietly matter. This guide shows how a 529 account can thoughtfully fit alongside your other financial goals – before you commit long-term dollars.

529 Account Learning Points

Keeping 529 Accounts in Perspective

For many families in America, higher education aspirations are funded by a mix of parent and student loans, savings/investments, and current income. The dream of giving your child the gift of a great college education can be financially challenging without thoughtful planning.

If you’re evaluating ways to financially support your child’s education, you can analyze whether saving and investing in a 529 account when your children are young supports your education funding goal.

Currently, college is one of several ways families can effectively use their 529 account funds.

In 2025, Sallie Mae and Ipsos released their latest survey results titled ‘How America Pays for College’. This data-rich report details a variety of factors and approaches to how American families pay for their child’s higher education.

One notable statistic from this report was that families with $150,000+ in annual income reported that an average of 21%, or $7,726 out of $37,219, of their child’s college education expenses was covered by a “college savings fund, such as a 529 plan” for academic year 2024-2025 . While this data is from a relatively small snapshot of families across America, it illustrates a significant financial commitment for families, for each child, each year covering their entire undergraduate career.

With families deploying a mixture of student loans, scholarships, federal work-study, grants, current income and investment assets to pay for higher education, a 529 account is just one of the many tools that families have available to them.

Given the variety of additional funding resources available to families for undergraduate-related expenses, you’ll want to understand how you can use 529 assets before, during, and after your child’s undergraduate years.

529 Account Basics

What is a 529 plan?

A section 529 plan is a tax-advantaged investment program designed to help families save for education expenses. 529 plans are also known as a “qualified tuition plan”. 529 plans are sponsored by states, state agencies, and educational institutions. In 2025, there are two kinds of 529 plans:

- Education Savings Plans: most education savings plans are available to everyone. A few have residency requirements for the account holder and/or the beneficiary. This type of plan provides a broader use-case for families than a Prepaid Tuition Plan.

- Prepaid Tuition Plans: While these typically have residency requirements, one notable exception is a prepaid tuition plan sponsored by a group of private colleges and universities. This is a narrower use-case than an Education Savings Plan. It does provide clarity for families whose education funding goals align with this plan’s specific use.

529 Account Uses

529 accounts allow families a flexible, tax-advantaged way to save and invest in support of the following educational goals:

- Kindergarten through 12th grade (K-12)

- Trade Schools / Apprentice Programs

- Undergraduate studies

- Qualifying graduate schools

- Student loan repayment

529 Account Key Features

Depending on factors like what state you live in and what 529 plan you use, a 529 account can support your family’s education funding goals in the following ways:

529 Plan: Key Features

Depending on factors like what state you live in and what 529 plan you use, a 529 account can support your family’s education funding goals in the following ways:

| Feature | Details | |

|---|---|---|

| State Income Tax Deductibility for Contributions |

Depending on what state you live in and what 529 plan you contribute to, your 529 account contributions may be tax-deductible at the state level. There are currently no federal tax benefits for 529 account contributions. |

|

| Tax-Advantaged Growth |

The money invested in the account accumulates tax-deferred at the federal level, and in many cases, at the state level as well. |

|

| Tax-Free Withdrawals |

When the money is withdrawn to pay for qualified education expenses, those withdrawals are federal income tax-free and often state income tax-free as well. This can lead to significant savings over time compared to using taxable investment accounts. |

|

| Investment Flexibility |

529 accounts offer investors a variety of investment choices that align with each family’s ability, willingness, and capacity for risk. Ultimately, you’ll want to follow an investment strategy that allows you to sleep at night. |

|

Like so many topics in financial planning, coordinating with a qualified tax advisor can be an important step when planning and executing your education funding strategy.

If funding your child’s 529 account is a savings priority for you, read on, and read on to familiarize yourself with the essential details of these investment accounts.

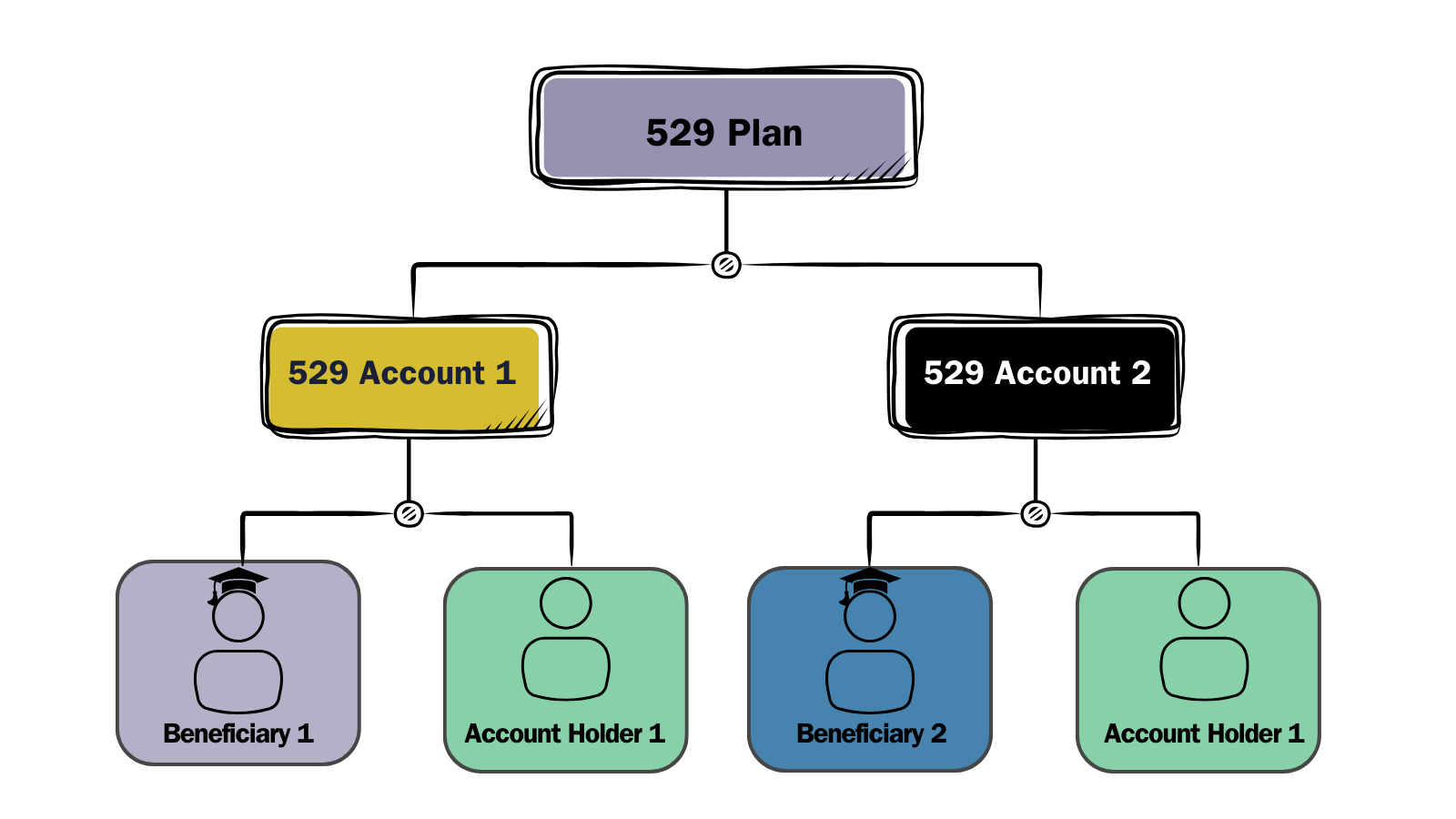

529 Account Roles

When you open a 529 account through either of these two plan types, your role is called the account holder, or the saver. The account holder opens the account for the beneficiary (e.g. your child). Technically, the account holder and the beneficiary can be the same person.

The chart below illustrates how these roles fit together for a family with two children.

An account holder can open multiple 529 accounts at the same 529 plan, and each account can be for a different beneficiary.

There is no “one-size fits all” 529 strategy. The way you approach selecting, opening, and managing a 529 account depends on your personal facts and circumstances.

Here’s a simple framework to follow:

- What state do you live in?

- When does your 529 beneficiary need to use the money?

- What kind of educational need, or needs, will the 529 fund?

Your 529 Account Starting Point: What State Do You Live In?

It’s helpful to center your 529 plan analysis around your state of residency.

This is primarily driven by each state’s specific approach to taxes on 529 plan contributions and distributions. Centering your analysis at the state level helps you create a base case which you can then compare against other 529 plans and education savings accounts.

For example, some states, like Missouri, offer residents a tax deduction for their 529 plan contributions. Other states, like Kentucky, assess an income tax but do provide a tax deduction or credit for 529 plan contributions. The amounts of these tax deductions vary from state to state.

If you live in a state that has no state income tax, like Texas or Tennessee, there is no state income tax deduction or credit to consider.

Similarly, when it comes to K-12 tuition, the states have a mixed view. Some states, like New York, currently take the position that paying for K-12 expenses with 529 funds is a non-qualified distribution.

If you live in a state that follows this approach, this could influence the timing of when you plan to distribute funds from your 529 account. Other states allow you to use 529 assets to pay for qualified education expenses.

The takeaway here is to familiarize yourself with your state’s specific 529 plan-related rules, tax benefits, and limits. It’s easy to skip over your 529 plan’s Program Description materials.

State Tax Reciprocity Arrangements

Some states that levy state income taxes, like Missouri, provide additional flexibility for residents to use 529 plans from other states.

This kind of reciprocity arrangement treats other state’s plans the same way as the in-state plan is treated. And so, you’ll want to be clear on the details of each state’s reciprocity arrangement before enrolling in a 529 plan sponsored by a different state. These state tax reciprocity arrangements can change.

You can check with the 529 plan’s administrator or your qualified tax professional for the latest information.

Contributions and Tax Considerations

Federal Tax Treatment

While contributions to a 529 account are not tax-deductible at the federal level, they are subject to the annual gift tax exclusion limit. In 2026, an individual’s annual gift tax exclusion limit is $19,000 per recipient.

State Tax Deductions and Credits

Many states offer a tax deduction, and a handful offer tax credits, for residents who contribute to a 529 plan. Families in St. Louis and throughout Missouri may elect to claim this benefit whether they invest in a Missouri 529 plan, or another state’s 529 plan.

For example, Missouri residents can contribute up to the following amounts in a 529 plan and reduce adjusted gross income:

- $8,000 (filing single)

- $16,000 (married filing jointly)

Given this approach, for example, if a Missouri resident grandparent contributes to their grandchild’s out-of-state 529 account, they could still pursue this tax benefit. The same holds true for a Missouri parent contributing to their child’s out-of-state 529 account.

Contribution Timing

Most states have a December 31 contribution deadline to qualify for state tax deductions or credits. A minority of states have contribution deadlines in April contribution. If you plan to contribute to a 529 account and claim a deduction, be sure to follow your state’s contribution deadline.

Superfunding / 5-Year Election

Since it’s tax filing season, it’s only fitting to reference one of the more concise explanations of 529 account superfunding:

“If in 2025, you contributed more than $19,000 to a qualified tuition plan (QTP) on behalf of any one person, you may elect to treat up to $95,000 of the contribution for that person as if you had made it ratably over a 5-year period. The election allows you to apply the annual exclusion to a portion of the contribution in each of the 5 years, beginning in 2025. You can make this election for as many separate people as you made QTP contributions.”

Source: Internal Revenue Service: Instructions for Form 709 – United States Gift (and Generation-Skipping Transfer) Tax Return, 2025.

Keep in mind that in 2026, the annual gift tax exclusion allows individual taxpayers to give each recipient up to $19,000 per year without incurring a gift tax.

If you embark on a 529 account superfunding strategy in 2026, you can contribute up to $95,000. That’s a lot of books. If you’re interested in learning the details on this approach, here’s a more in-depth discussion.

Earnings

529 plans can have a maximum account balance or maximum contribution limit.

For 529 accounts with a maximum account balance, the plan will accept contributions to your account(s) until the aggregate balances for the same beneficiary reach the predetermined maximum account balance limit.

If your plan has a maximum contribution limit then the accounts for the same beneficiary that have reached this limit may continue to accrue earnings but will not accept any additional contributions. With this provision, your 529 account(s) could exceed the stated limit, but only because of earnings/investment growth.

For 529 plans with maximum limits, it represents an estimated maximum cost of some combination of undergraduate and graduate school. The maximum on a 529 plan may adjust each year to reflect the rising cost of higher education.

Currently there is not a federal limit on the total (lifetime) amount that can be contributed to a 529 plan. The limits are determined at the state level.

Qualified Expenses

Qualified Higher Education Expenses

Tuition, fees, and the costs of books, supplies, and equipment required by the Eligible Educational Institution. Some room and board costs are qualified when your child is attending at least half-time. Be sure to consult with your school to determine what counts as half-time attendance.

Qualified K-12 Education Expenses

Many states allow 529 account distributions of up to $20,000 per year, per beneficiary, for qualified education expenses in connection with enrollment or attendance at a K-12 school.

These include elementary or secondary public, private, or religious schools.

H.R. 1, commonly referred to as the OBBBA or “One Big Beautiful Bill Act”, expanded the use of 529 funds. Specifically, effective after July 4, 2025, Section 70413 of the OBBBA widened the scope of “qualifying higher education expenses” to include materials, standardized testing, tutoring, and therapies for K-12 education .

Here is the current, expanded list of qualifying higher education expenses available to many American families for K-12 education:

Qualified K–12 Education Expenses

Qualifying higher education expenses available to American families for K–12 education:

| Expense | Details | |

|---|---|---|

| Tuition | Tuition for K–12 education. |

|

| Curriculum and Materials | Curriculum and curricular materials, books or other instructional materials, and online educational materials. |

|

| Tutoring and Educational Classes |

Tuition for tutoring or educational classes outside of the home, including at a tutoring facility, but only if the tutor or instructor is not related to the student and meets one of the following:

|

|

| Standardized Tests and Exams | Fees for a nationally standardized norm-referenced achievement test, an advanced placement examination, or any examinations related to college or university admission. |

|

| Dual Enrollment | Fees for dual enrollment in an institution of higher education. |

|

| Educational Therapies for Students with Disabilities | Educational therapies for students with disabilities provided by a licensed or accredited practitioner or provider, including occupational, behavioral, physical, and speech-language therapies. |

|

This expanded definition empowers families to better support their child’s educational needs and goals. Tutoring and therapy can represent significant educational expenses for American families.

Trade Schools and Apprenticeship Programs

Your 529 account can pay for the fees, books, and equipment required by qualifying trade school/apprenticeship programs. Parents will want to consult with the specific institution to verify whether it is a certified apprenticeship institution.

Student Loan Repayment

You can disburse 529 account assets to pay principal and/or interest on your designated beneficiary’s or their sibling’s qualified student loan. In 2026, this option is currently limited to a lifetime maximum of $10,000 per beneficiary when used to repay qualified student loans for the beneficiary, or the beneficiary’s sibling.

Keep in mind that if you use your 529 account to repay your eligible student loan, you can’t include any interest from that portion of the loan repayment in your federal income tax deduction.

Postsecondary Credentialing Expenses

Interestingly, Section 70414 of the OBBBA expanded Americans’ ability to use their 529 funds toward certain ‘postsecondary credentialing expenses’, such as the following:

Postsecondary Credentialing Expenses

Qualifying postsecondary employment credentials and related expenses:

| Expense | Details | |

|---|---|---|

| Industry-Recognized Credentials |

Any postsecondary employment credential that is industry recognized and is issued by a program that is:

|

|

| Registered Apprenticeship Certificate | Any certificate of completion of an apprenticeship that is registered and certified under the National Apprenticeship Act. |

|

| Occupational or Professional License | Any occupational or professional license issued or recognized by a State or the Federal Government (and any certification that satisfies a condition for obtaining such a license). |

|

| Recognized Postsecondary Credential | Any recognized postsecondary credential as defined in section 3(52) of the Workforce Innovation and Opportunity Act. |

|

Withdrawals

Qualified and Non-Qualified Withdrawals

When withdraw/distribute money from your 529 account to pay for qualified education expenses, those distributions are not taxable. These withdrawals are comprised of contributions and earnings. With just a handful of exceptions, a non-qualified withdrawal happens if you withdraw money from your 529 account and use it to pay for anything other than qualified education expenses.

529 Timing Rule

The timing of your 529 account withdrawals should match the same tax year you paid the qualified educational expenses. If your total distributions exceed the beneficiary’s qualified education expenses, the excess portion of the earnings is taxable.

Non-Qualified Withdrawal Consequences

The earnings on a non-qualified withdrawal may be subject to federal income tax, a 10% federal penalty tax, state and local income taxes and the potential recapture of state tax deductions.

Exceptions to the 10% Penalty

In certain cases, a 529 account owner can take a non-qualified withdrawal that is not subject to the 10% federal tax penalty on earnings. These special cases include the following:

529 Plan: Penalty Exceptions

Situations in which the 10% early withdrawal penalty may be waived:

| Exception | Details | |

|---|---|---|

| Death or Disability | The beneficiary died or became disabled. |

|

| Scholarship | The beneficiary received a scholarship. The amount of the withdrawal up to the amount of the scholarship is exempt. |

|

| U.S. Service Academy Attendance | The beneficiary is attending a U.S. service academy (for example, the United States Air Force Academy near Colorado Springs, Colorado or United States Naval Academy around Annapolis, Maryland). |

|

| Federal Education Tax Credits | Funds from the withdrawal used to claim certain federal education credits such as the American Opportunity and Lifetime Learning credits. |

|

IRS Form 1099-Q

Your 529 Plan will issue you a Form 1099-Q for the taxable year that you withdraw funds for any reason. Work with your qualified tax professional to understand what else is required in your personal situation.

What If My Child Doesn’t Go to College?

529 Account: Options If Funds Are Not Used

Alternatives to consider when 529 funds are not needed for the original beneficiary:

| Option | Details | |

|---|---|---|

| Change the Beneficiary | You can update the account beneficiary to another “member of the family” of the original beneficiary. For example, if your son or daughter has a sibling or a cousin, a same-generation family member is a clean approach. |

|

| Hold the Account | There’s no deadline to use the funds. You can simply wait – your child might go back to school, pursue a trade program, or you can change the beneficiary later. |

|

| Non-Qualified Withdrawal | See the Non-Qualified Withdrawal Consequences above. |

|

| 529 Roll Over to a Roth IRA | See the next section below. |

|

529 to Roth IRA Rollover

529 account holders can transfer up to a lifetime maximum of $35,000 from a 529 plan to a Roth IRA for a beneficiary. This approach allows Roth IRA owners a chance to avoid triggering non-qualified withdrawal penalties for an overfunded 529. It’s intended to address concerns from families who do not want to overfund their 529 account(s) and face significant tax penalties on non-qualified withdrawals.

Key eligibility criteria for this approach include:

- The 529 account must be more than 15 years old to qualify for this rollover. Starting early, even with a nominal amount is one approach to get the clock started.

- Only amounts contributed to the 529 account more than five years ago can be rolled over.

- The in-force Roth IRA contribution limits still apply. Your Roth IRA contributions consist of after-tax dollars – money you’ve already paid income tax on. In 2026, you can contribute up to the following amounts into a Roth IRA:

- $7,500 per person.

- Up to $8,600 per person if you are age 50 or older.

Note that this applies specifically to Roth IRAs, not traditional IRAs.

Investing in Your 529 Account

Investment Options

529 plans traditionally offer investment options like mutual funds, exchange-traded funds (ETFs), CDs, and an FDIC insured or cash equivalent type of account.

Risk Continuum by Time Horizon

You can choose investment options in your 529 account that align with your personal risk tolerance and time horizon.

For example, if you need your high school freshman’s 529 account to cover college costs in a few years, you’re probably less risk tolerant about your 529 investments than when your child was a toddler. This shift is driven, in part, by the fact there is less time to recover from a significant decline in stock markets. There is also less time to contribute to your child’s 529 account. Practically, this means adjusting from stock/equity investments to bond and savings-type investments.

The chart below illustrates this concept:

For parents planning to use your 529 account to pay for near-term, K-12 educational expenses, you may feel more comfortable with a savings-type investment.

What about those families looking to save money for both a long- /intermediate-term goal (e.g. college) and a short-term goal (K-12) for the same child? How could they invest for each of these two separate goals? One simple approach is to open two 529 accounts and invest each differently according to the time-horizon of the goal.

Age-Based and Target Enrollment Year Portfolios

529 plans with age-based and target-enrollment year portfolios decrease your expected investment risk as your child approaches their first tuition bill. Some plans use a glide path to automate this transition. They shift investments from growth-oriented equities to capital-preserving bonds and cash.

Some target enrollment year portfolios feature two-year portfolios that reallocate quarterly. This is intended to create an incremental transition rather than a sudden shift.

Others offer tiered tracks based on your risk tolerance; conservative, moderate, or aggressive. This allows you to choose a glide path that matches your personal risk tolerance and while still participating in the automatic, age-driven reduction in expected risk of the investments in your portfolio. Mechanically, some portfolios use a stepped approach while others attempt a progressive approach to asset allocation.

For example, one plan I recently reviewed utilizes nine age-based portfolios. The plan adjusts as your child gets older, shifting the account’s investments from 100% equity for newborns to 20% equity for those 19 and older. Other plans adjust your investments between static portfolios based on your child’s age bracket (i.e. a stepped approach). Target enrollment year portfolios adjust the underlying mix within a single portfolio (i.e. a progressive approach).

The distinction between stepped and progressive approaches is especially critical during periods of elevated stock market volatility. Progressive models seek to decrease the “market timing” risk of moving large sums of money on a single day (e.g. your child’s birthday). Instead, as your child’s college enrollment nears, a progressive portfolio steadily decreases it’s expected risk by increasing the amount of investments that support preserving your existing 529 assets.

Four Evergreen Principles

529 Account: Investment Principles

Key principles to keep in mind when managing your 529 investment strategy:

| Principle | Details | |

|---|---|---|

| Avoid Market Timing | Market timing over your investment horizon is unlikely to deliver consistent, excess returns. Many 529 plans limit your ability to adjust your investments to only twice a year. |

|

| Expenses and Taxes Matter | Frictions such as high costs and unnecessary taxes can erode returns over time. This can cause high performing investments to not look as stellar after you factor in expenses and taxes. |

|

| Don’t Play the Losers Game | There is no evidence about the persistence of past performance as an indicator when selecting investments. |

|

| Manage Your Emotions and Biases | Emotions, biases, and other psychological factors can cause the average investor, generally, to be wired to be poor investors of their own money. Be aware that these factors exist and take time to fully reevaluate your plan if you find yourself reacting, and not responding, to a particular situation. |

|

Fee Evaluation

529 Account: Common Fees to Understand

Types of fees you may encounter when evaluating and maintaining a 529 plan:

| Fee Type | Details | |

|---|---|---|

| Enrollment & Application Fees | Today, it’s more rare than common for 529 plans to charge a fee to open an account online in 2026. Some may charge a nominal fee (e.g., $50) if you insist on submitting a physical paper application. |

|

| Account Maintenance Fees | This is a “keep the account” open cost. Many 529 plans have eliminated annual maintenance fees to encourage long-term saving. Some state 529 plans charge a nominal fee (e.g. $25/account/year). Some state plans waive this fee for their own residents or if you maintain an account that meets a predetermined minimum balance. |

|

| Program Management Fees | This is what you pay the state and its professional partners to run the 529 plan. |

|

| Underlying Investment Expense Ratios | These are the costs of the mutual funds or ETFs within your portfolio. |

|

Carefully review the fees of any plan you’re considering. High fees can erode your investment returns.

Keep in mind, too, that you do not need to work directly with a broker to open and fund a 529 account. Often, a direct-sold 529 plan, one that you can open and fund on your own, has lower fees and expenses.

Practical Planning Considerations

It’s important to know how your child’s 529 account affects your family’s college funding options. If your child is getting close to attending college, you can review your 529 decisions through two distinct lenses:

- Free Application for Federal Student Aid (FAFSA)

- College Scholarship Service (CSS Profile)

Don’t let these models take priority over making progress on all your most important goals. Understand the long-term tradeoffs before making any dramatic changes in your financial life just for the sake of gaining a short-term edge or favorable outcome on the FAFSA or CSS Profile.

“Grandparent”-owned 529 accounts and FAFSA impact

Under the current FAFSA methodology, if a parent is the 529 account holder, then the assets in those accounts will be reported as parent assets. This potentially reduces your child’s need-based aid by as much as 5.64% of the 529 account’s value.

However, if a grandparent, relative, or even close family friend is the owner of the 529 account, then neither the assets nor the withdrawal of those assets negatively affects the FAFSA calculation.

Keep in mind that many private colleges also use the CSS Profile (or their own aid application form), and “grandparent”-owned 529s may still affect a study’s aid calculation under non-FAFSA methodologies.

Rollovers Between 529 Plans

If you are considering transferring your 529 account assets from one state’s plan to another, you’ll want to understand the federal and state tax implications.

At the federal level, you can complete a rollover once every 12 months for the same beneficiary. Importantly, you’ll want to complete your rollover within 60 days of the distribution.

At the state level, not all states follow the federal approach detailed above. If you roll over your 529 account from one state to another, then you could potentially face state tax recapture

In 2026, some states are particularly clear about “recapture”; they require you to pay back any state tax benefits (e.g. deductions or credits) on the related contributions or assets.

Open Your Child’s 529 Early to Start the 15-Year Clock

If you’ve identified that a 529 account fits into your family’s education funding plan, consider opening and funding it as soon as you can do so. In addition to giving your investments more time to work for you, to benefit from tax-free earnings growth, it also starts the 15-year, 529 to Roth IRA rollover clock.

529 Account: Frequently Asked Questions

How much can I contribute to a 529 in 2026?

Individual contributions to a 529 account are subject to the annual gift tax exclusion limit. In 2026, an individual’s annual gift tax exclusion limit is $19,000 per recipient. A married couple could therefore contribute up to $38,000 per year per beneficiary.

If you decide to superfund your child’s 529 account in 2026 – a funding technique that far exceeds these figures – working with your qualified tax professional can help you stay on the right path.

Is a 529 contribution tax-deductible?

While a 529 account contribution is not deductible at the federal level, some states provide tax deductions or credits. For example, Missouri residents can contribute up to the following amounts in a 529 plan and reduce adjusted gross income:

+ $8,000 (filing single)

+ $16,000 (married filing jointly)

Can I use a 529 for K-12 private school tuition?

Many states, but not all, allow 529 account distributions of up to $20,000 per year, per beneficiary, for qualified higher education expenses in connection with enrollment or attendance at a K-12 school.

These include elementary or secondary public, private, or religious schools.

What qualifies as a qualified education expense for 529 accounts in 2026?

+ Qualified Higher Education Expenses: Tuition, fees, and the costs of books, supplies, and equipment required by the Eligible Educational Institution. Some room and board costs are qualified when your child is attending at least half-time (this status can vary by institution).

+ Qualified K-12 Education Expenses: Many states allow 529 account distributions of up to $20,000 per year, per beneficiary, for qualified education expenses in connection with enrollment or attendance at a K-12 school. These include elementary or secondary public, private, or religious schools.

Qualified expenses include the following; tuition, curriculum and curricular materials, books or other instructional materials, online educational materials, tuition for tutoring or educational classes (with specific caveats noted above), fees for a nationally standardized norm-referenced achievement test, an advanced placement examination, or any examinations related to college or university admission, fees for dual enrollment in an institution of higher education, educational therapies for students with disabilities provided by a licensed or accredited practitioner or provider, including occupational, behavioral, physical, and speech-language therapies.

+ Trade Schools and Apprenticeship Programs: fees, books, and equipment required by qualifying trade school/apprenticeship programs.

+ Student Loan Repayment: pay principal and/or interest on your designated beneficiary’s or their sibling’s qualified student loan. In 2026, this option is currently limited to a lifetime maximum of $10,000 per beneficiary when used to repay qualified student loans for the beneficiary, or the beneficiary’s sibling.

+ Postsecondary Credentialing Expenses: certain postsecondary employment credential that is industry recognized, certificate of completion of an apprenticeship, and occupational or professional license issued or recognized by a State or the Federal Government.

What happens to my child’s 529 account if they get a scholarship?

A 529 account owner can take a non-qualified withdrawal that is not subject to the 10% federal tax penalty on earnings if the beneficiary receives a scholarship. The exempt withdrawal can be up to the amount of the scholarship.

What happens to the 529 account funds if my child doesn’t go to college?

If your child has a 529 account and does not go to college, here are some common approaches to address the unused 529 assets. You can change the 529 account beneficiary. You can also continue to maintain the account if it’s unclear whether your child might go back to school later in life, pursue a trade program, or start a 529 account to Roth IRA rollover strategy.

You can also take non-qualified withdrawal.

When should I open a 529 account for my child?

A 529 account is a flexible, tax-advantaged way to save and invest toward your child’s educational future. From K-12 tuition to trade schools, undergraduate studies, qualifying graduate programs, and even student loan repayment. While a specific opening timeline isn’t prescribed, the earlier you begin, the more time your contributions have to compound. Explore whether the plan you choose aligns with your state’s tax benefits and your savings priorities.

Can I roll a 529 account into a Roth IRA?

529 account holders can transfer up to a lifetime limit of $35,000 from a 529 plan to a Roth IRA for a beneficiary. This approach allows Roth IRA owners to avoid triggering non-qualified withdrawal penalties for an overfunded 529.

Can grandparents contribute to a 529?

Yes; anyone can contribute to your child’s 529 account. Contributors do not have to be a family member of the beneficiary to contribute to their 529 plan.

What is the difference between a 529 account and a Roth IRA for education savings?

One of the primary differences between these two account types surrounds the way you can contribute to each; a Roth IRA requires earned income, whereas a 529 account does not.

A Roth IRA has an annual contribution limit, and a 529 account has no annual contribution limit. A 529 account can be used for qualified educational expenses, student loan repayment, etc. as noted above.

A Roth IRA has age restrictions on withdrawals since it is primarily intended to support retirement saving and investing. Depending on who owns the Roth IRA, it will either count as the parent or student asset on the FAFSA.

Specifically, student assets are weighted at a 20% contribution rate whereas parent assets carry a maximum 5.64% contribution rate on the FAFSA. If your goal is to primarily fund your child’s education, a 529 account generally offers more compelling features than a Roth IRA.

Do I Open Three Separate 529 Accounts for Each of My Three Kids?

If you have three kids, it’s helpful to fund a unique 529 account for each of them. Depending on your personal situation and educational goals, this can provide you with flexibility later in life to:

+ Customize your funding and withdrawal strategies to their educational needs.

+ Name each child as a beneficiary to their own 529 account.

+ Submit claims for state tax deductions, especially deductions are allowable per beneficiary.

+ Only count the correct child’s 529 assets in your parental assets for FAFSA.

+ Take advantage of the 529 to Roth IRA rollover, if needed.

What are the types of “recognized postsecondary credential”?

Any postsecondary employment credential that is industry recognized and is:

+ issued by a program that is accredited by the Institute for Credentialing Excellence, the National Commission on Certifying Agencies, or the American National Standards Institute,

+ included in the Credentialing Opportunities On-Line (COOL) directory of credentialing programs (or successor directory) maintained by the Department of Defense or by any branch of the Armed Forces, or

+ identified for purposes of this clause by the Secretary, after consultation with the Secretary of Labor, as being industry recognized.

—

+ any certificate of completion of an apprenticeship that is registered and certified under National Apprenticeship Act,

+ any occupational or professional license issued or recognized by a State or the Federal Government (and any certification that satisfies a condition for obtaining such a license), and

+ any recognized postsecondary credential as defined in section 3(52) of the Workforce Innovation and Opportunity Act.

What are ‘qualified higher education expenses’ for postsecondary credentialing?

+ tuition, fees, books, supplies, and equipment required for the enrollment or attendance of a designated beneficiary in a recognized postsecondary credential program, or any other expense incurred in connection with enrollment in or attendance at a recognized postsecondary credential program if such expense would, if incurred in connection with enrollment or attendance at an eligible educational institution, be covered under subsection (e)(3)(A),

+ fees for testing if such testing is required to obtain or maintain a recognized postsecondary credential, and

+ fees for continuing education if such education is required to maintain a recognized postsecondary credential.

The Next Step

We help busy parents and professionals like you develop financial plans to address questions like:

- How can we save for a fulfilling retirement beyond our 401(k) plans?

- What does it take to save for the kids’ education and make a lifetime of memories along the way?

- These causes are close to our hearts. What are our options to give even more meaningful support?

As your financial planner in St. Louis, we can help you get organized and start feeling more confident that you are making progress towards your savings priorities.

Working with your financial planner in St. Louis can provide you with the right mix of accountability, collaboration, and long-term thinking.

When you know who and what are truly important, we can help you create incredible clarity about your spending and savings priorities. Clarity to confidently save for and spend on what matters.

If you’re ready to take the next step and work with a financial planner in St. Louis, let’s talk.

Disclosure

This commentary is provided for educational and informational purposes only and should not be construed as investment, tax, or legal advice. The information contained herein has been obtained from sources deemed reliable but is not guaranteed and may become outdated or otherwise superseded without notice. Investors are advised to consult with their investment professional about their specific financial needs and goals before making any investment decision.